Advisors frequently ask: “My plan sponsors are asking me why they should choose stable value investments over money market funds. How can I convince them to stay the course with stable value?”

Given recent actions by the Federal Reserve and market expectations of additional interest rate cuts on the horizon, it’s a good time to discuss this topic.

Stable value investments have generally outperformed money markets year after year in retirement plans. However, consecutive federal funds rate hikes beginning in March 2022 flipped the script, temporarily positioning money market funds ahead of stable value.

But based on recent Fed comments, as well as the September 2025 rate cut and outlook, here are a few key things to keep in mind:

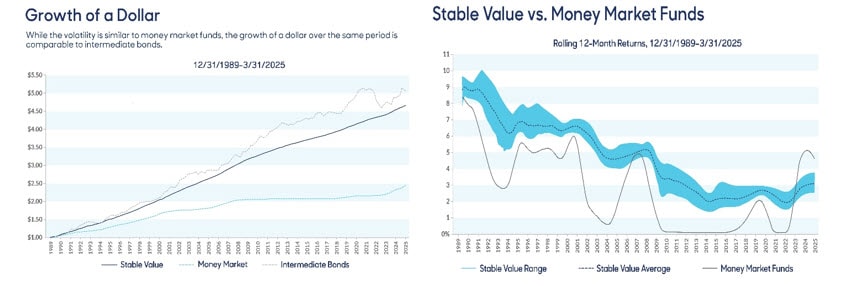

1. Long-term returns matter. Over the long term, the return of a dollar invested in stable value far outweighs average returns earned in a money market fund (Chart 1). As seen below, a dollar invested in stable value in 1988 would more than double in value relative to the same investment held in money market funds. This is because, over long periods, earned rates on stable value are typically above money market rates by nearly 200 basis points. And even though money market rates have been higher in recent years, the trend is already starting to reverse with recent Fed rate cuts (Chart 2).

2. Retirement investing is not a sprint. It’s a marathon spanning decades where slow and deliberate matters. Money markets are short-term debt instruments, aka “cash,” and often used to meet anticipated near-term liquidity needs. With durations typically of six months and shorter, they are generally less suited to the long-term investment horizon of retirement plans as a core portfolio holding.

3. So why are stable value returns higher over time? This is for the same reason that bond funds provide higher returns than money market funds in a normal yield market where it costs more to borrow longer. Stable value steps in as a hybrid of both — combining low volatility and stable NAV (net asset value) similar to cash, but with the help of insurance wraps, able to invest longer to earn bond-like returns. And, if rates continue to rise, typically stable value will eventually catch up with the lag.

Source: Based on Stable Value Investment Association Composited Data files as of March 31, 2025. Returns illustrated are gross before any fees.

4. Yield curve inversions are anomalies. Reviewing the history — only six inversions have occurred over the last 45 years and all reverted back. While each plan sponsor’s situation is unique and should be evaluated on its merits, staying the course is likely the solution in many cases.

5. It’s risky to make a choice based on short-term Fed actions. As seen in Chart 2, money market funds rates shadow federal fund rate moves almost identically — as rapid as the rise so could be the fall. And tied so closely to Fed actions, money market rates are more volatile. Let’s also not forget recent history of prolonged zero percent interest Fed policy with money market rates languishing for nearly seven years.

Of course, no one can predict when stable value and money market returns will revert to historical norms, nor should anyone try. Money market yields have begun to decline following a series of Fed rate cuts totaling 100 basis points over the past two years. Stable value crediting rates, while slower to adjust, remain competitive and outperform in the long run and continue to be a viable option for plan sponsors seeking consistency and stability.

Discover more from MassMutual…

Stable value market value adjustments and other solutions

Stable value in today’s markets

________________________________________

This article was originally published in November 2023. It has been updated.