Businesses of all sizes and shapes were impacted by economic volatility during the past year, with some even closing their doors permanently. But the federal government’s nearly two trillion-dollar response to the pandemic, coupled with the “reopening” of the economy, is paving the way to brighter days ahead.

The Federal Reserve reported an economic growth rate of 6.4 percent in the first quarter of 2021 and in a survey released this May, the National Association of Business Economists (NABE) projected an annual expansion rate of 6.5 percent1. Such robust growth rates have not been seen in nearly 40 years.

The economic resurgence is intensifying the competition for skilled workers, especially for experienced managers who can lead businesses to profitability and growth. Meanwhile, many employees, after working from home for the past year, are reluctant to return to a group office setting. They treasure their newfound work-life balance, relative safety from health risks, elimination of stress from commuting and the freedom to manage their daily household affairs. Further complicating things, many who exited the workforce in 2020 seem yet pressured to return.

It’s a predicament that businesses have rarely, if ever, faced. The challenge is prompting companies to create incentives of all kinds to attract sought after talent.

Typically, cash and accommodative incentives enhance a company’s total rewards package to lure targeted workers away from competitors. Where those enticements are insufficient, companies can further enrich total rewards packages with nonqualified and executive benefits. A package for highly compensated and leadership roles often includes nonqualified deferred compensation (NQDC). When properly structured, NQDC can be an important tax management and supplemental retirement planning tool for participants.

The odd tension in today’s market for top talent is directly attributable to 2020’s volatility and uncertainty. Companies today need to convince workers of the value of a compensation package as well as manage concerns around employees’ expectations of actually receiving future benefits. Companies can set themselves apart from competitors by communicating to newly hired and potential high value recruits that the NQDC and executive benefit plans offered are informally funded with reserved assets.

After a tumultuous year, where new precedent was established around tax-qualified and ERISA plans, employees’ concerns about future deferred compensation benefits are real.

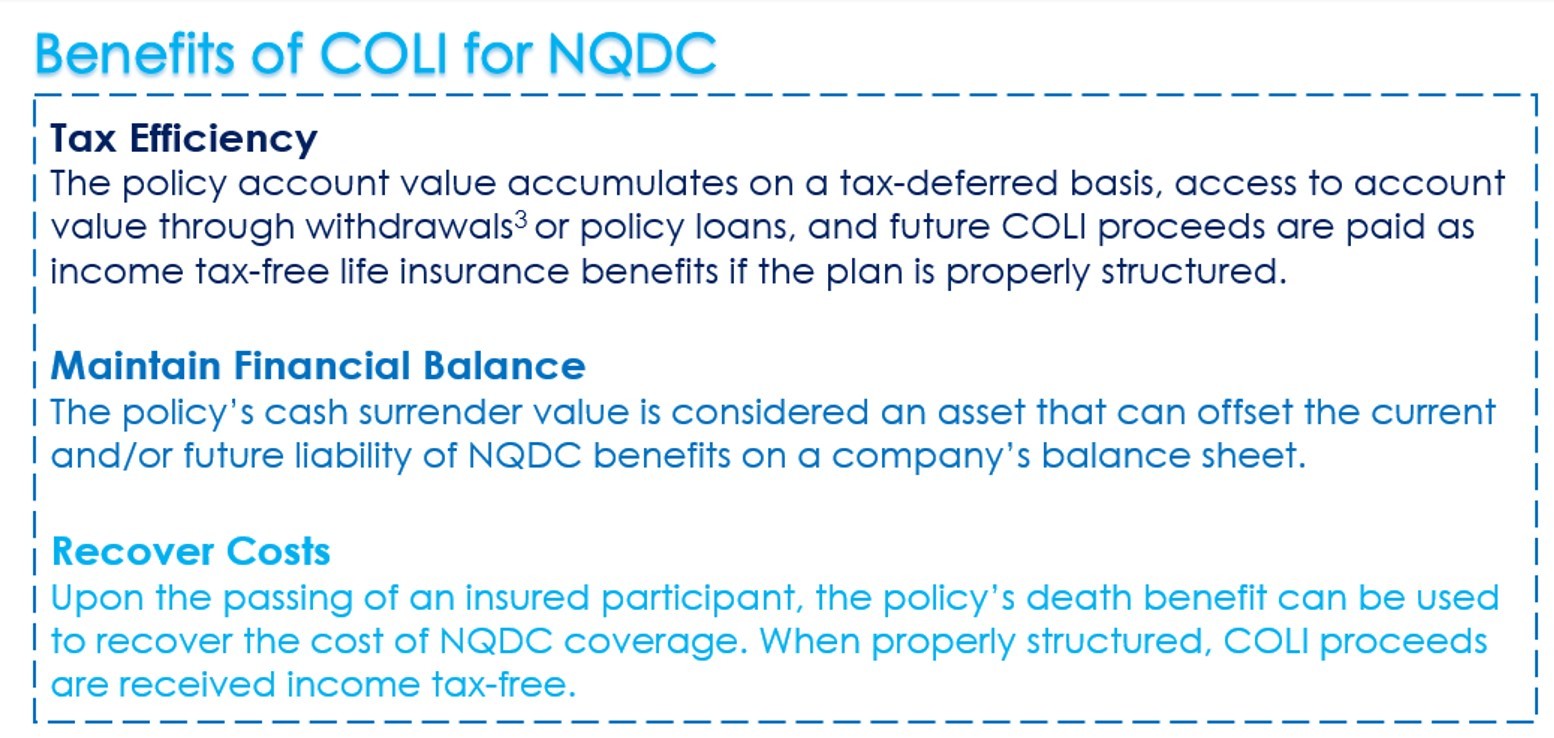

Corporate-owned life insurance (COLI) is a common type of asset earmarked for this purpose. The tax-deferred nature of COLI mirrors the tax features of NQDC plans and is an efficient asset accumulation strategy, particularly in a rising income-tax rate environment. Further, employees’ concerns can be directly addressed by holding COLI in a “Rabbi” trust, protecting those assets from being used for any other purpose.2 Businesses should work with their legal and tax counsel to determine the specific needs of the business.

Altogether, the use of COLI now may be more appealing and valuable than ever before. Often, COLI policies can enable companies to offer benefits that they might otherwise be unable to provide and is a highly effective way to help top talent prepare for and enter retirement. While assets do not need to be set aside to meet NQDC obligations, doing so enables businesses to responsibly make the most of their investment in their highly valued employees.

COLI policies are widely available from life insurance carriers but the long-term nature of NQDC benefits makes selecting a company with strong financial ratings critical. It pays to choose a company with among the highest ratings available from independent rating agencies such as A.M. Best, Standard & Poor’s, Fitch Ratings and Moody’s Investors Service.

Making use of COLI policies as a deferred compensation informal funding vehicle has become commonplace as companies compete harder than ever to attract and retain top talent. Companies that secure coverage can potentially provide themselves with a competitive edge as they grow and prosper.

____________________________________

1NABE Panelists Boost Forecast for GDP Growth in 2021; Expect Current Inflation to Moderate by Year-End

https://www.nabe.com/NABE/Surveys/Outlook_Surveys/May-2021-Outlook-Survey-Summary.aspx

2Short of insolvency; Assets in a Rabbi trust are available to corporate creditors in the event of bankruptcy proceedingsP

3Withdrawals and decreases in Face Amount may have tax consequences. Policy withdrawals are not subject to taxation up to the amount paid into the policy (the cost basis). If the policy is a Modified Endowment Contract, policy loans and/or withdrawals will be taxed to the extent of gain and are subject to a 10% tax penalty if the policyowner is under age 59-1/2. Loans and/or withdrawals also reduce the cash surrender value and death benefit. Access to the account values through borrowing and/or withdrawals will reduce the cash surrender value and may reduce the policy death benefit. Taking a policy loan could have adverse tax consequences if the policy terminates upon lapse or surrender or before the insured’s death.

COLI products issued by Massachusetts Mutual Life Insurance Company (MassMutual), Springfield, MA 01111-0001.