A key consideration in executing a Pension Risk Transfer (PRT) is whether to fund the group annuity contract premium through an Assets-in-Kind transfer (AIK). In an AIK transfer, an insurer accepts an agreed-upon portfolio of assets as partial payment for a PRT annuity purchase premium in lieu of cash. As we note in our paper, “Mitigating group annuity buy-out risks with Assets-In-Kind Transfers,” AIK transfers can eliminate certain costs and risks for both the insurer and the buyer, including delay costs, interest rate risks, and credit spread risks. Given the substantial size of many PRT transactions, some AIK transfers have saved the insurer and sponsor millions of dollars.

Because insurers value the diminished costs and risks from an AIK transfer— such as the delay costs associated with investing large sums of cash in the market and exposure to interest rate risks and credit spread risks -the insurer may offer a plan sponsor a discounted premium quote when it’s paired with an AIK transfer of desirable assets.

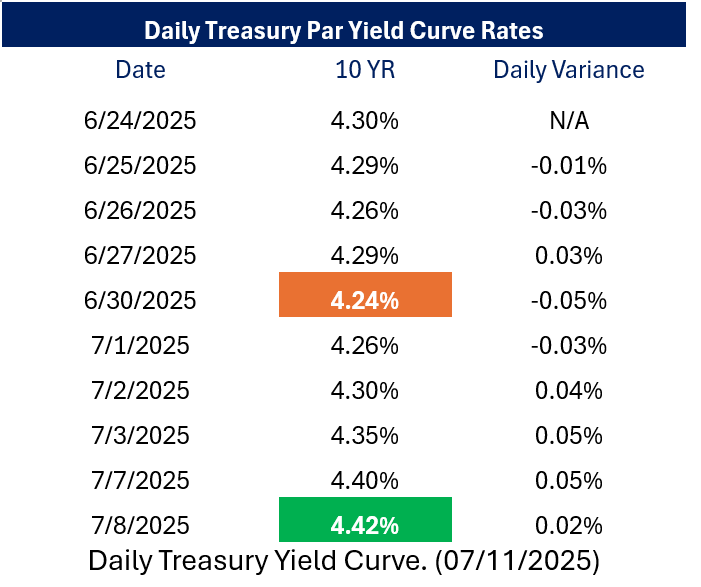

When exercising cash purchases of a PRT group annuity contract, it’s important for plan sponsors to understand that a volatile rate environment can result in a significant cost change even if the exposure only spans a few days. A review of the Daily Treasury Par Yield Curve Rates1 of the last five business days of June 2025 compared to the first five business days of July 2025 demonstrate the unpredictability- trending downward in June and upward in July, with rates fluctuating nearly 20 basis points during the period:

For a deeper understanding of how volatility impacts costs and risks in a PRT, and how an AIK transfer can help mitigate those costs and risks, please refer to our white paper, “Mitigating group annuity buy-out risks with Assets-In-Kind Transfers.”

We would appreciate the opportunity to engage with you and your pension plan customers to discuss how a PRT group annuity might help meet their objectives. For more information, please contact us.

______________

1Daily Treasury Yield Curve. (07/11/2025) https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value=2025