| ||||||||||||

High-net-worth households are doubling down on efforts to protect their wealth in the face of growing market, economic, and political uncertainty.

Many are making moves now not only to insulate against near-term risks, but also to capitalize on opportunities to reduce the size of their taxable estate.

Those risks include:

- A lower lifetime gift and estate tax exclusion limit.

- Reduction of the generation-skipping transfer tax exemption.

- Higher interest rates.

- Election year politics.

What is wealth management?

At its core, wealth management is aimed at helping affluent households grow and preserve their assets. With guidance from a trusted professional, or a team of professionals, that may involve tax-friendly investments, asset allocation strategies, and estate planning tools to facilitate the efficient future transfer of assets to loved ones or favorite charities. (Related: Lifetime gifting: Benefits and considerations)

A wealth management plan, however, is never a set-it-and-forget-it solution. It’s a process that is shaped by market forces and subject to change as your financial goals mature. And there’s plenty in flux at present.

Lifetime gift and estate tax exemption limit slated to be cut in half

Indeed, while tax law changes are never set in stone, it seems that many wealthy households could be facing higher tax bills ahead.

Some context: The Tax Cuts and Jobs Act (TCJA) of 2017 temporarily doubled the federal lifetime gift and estate tax exemption limit, which is indexed for inflation. In 2024, that limit is $13.61 million per person ($27.22 million for married couples). Assets above the limit that get passed along to your heirs are generally subject to a flat 40 percent tax rate. (Related: Planning now? The estate planning 2026 question mark).

Unless Congress extends it or makes it permanent, however, the higher lifetime gift and estate tax exemption limit is slated to revert back to its pre-TCJA levels after December 31, 2025. Thus, effective January 1, 2026, the exemption limit would decrease to $5 million indexed for inflation, estimated to be around $7 million per person, or $14 million for married couples.

“Only a handful of my clients today are affected by the estate and gift tax, but when the current exemption limit sunsets and the limit gets cut in half, that may change,” said Tom Naylor, a financial professional with GoldBook Financial in La Jolla, California. “People are living longer, and many are still accumulating wealth well after retirement. A 70-year-old today with a good amount of assets may live another 15 or 20 years and their net worth could double or triple during that time. So even if they fall below the exemption limit today, they still need to plan.”

Financial professionals can provide valuable guidance to affluent families who are looking to transfer more of their wealth tax-free to loved ones and favorite charities before the exemption limit drops. Some tools to consider include:

- Trusts — Trusts are legal entities that own and manage assets for the benefit of their heirs. Assets gifted into a trust can potentially be excluded from the grantor’s estate, so they are no longer subject to estate tax and are also protected from creditors, probate, and legal claims from ex-spouses. (Learn more: Lifetime gifting: Benefits and considerations)

- Donor-advised funds — Donor-advised funds are increasingly popular among higher net worth families who wish to engage in charitable giving. Such funds allow individuals to make irrevocable contributions of cash, securities, or appreciated assets in one year; claim the tax deduction immediately; and make grants to a charity of their choice in the future.

“Wealth managers stay on top of market fluctuations and changes to the tax code,” said Naylor. “We ensure that your estate planning documents and beneficiaries are current. We make sure that your assets are protected from creditors and that they’ll be passed along effectively outside of probate. That’s the importance of having annual reviews with your financial team,” he said.

Generation-skipping transfer tax

The generation-skipping transfer (GST) tax exemption, which stands at $13.61 million in 2024 ($27.22 million for married couples), is also slated to be cut in half (adjusted for inflation) at the end of 2025 per the expiration of certain TCJA tax provisions.

The GST tax exemption, which is separate from and in addition to the gift and estate tax exemption, enables individuals (often grandparents) to potentially pass more of their wealth along to individuals who are two or more generations younger (often their grandchildren) tax-free.

With lower exemption limits looming for the federal estate and gift tax and for the GST, Robert Brooks, managing partner of IBEX Capital Management in Boca Raton, Florida, said wealthy households should meet with a trusted financial professional today to review their wealth management strategy. With proper planning, he said, it may be possible to maximize the assets you leave behind.

For example, if you’ve reached your lifetime gift tax exemption limit, you might still be able to transfer up to $13.61 million ($27.22 for married couples) in 2024 or 2025 to your grandchildren tax-free.

“As the Tax Cuts and Job Act is expected to sunset, we have a golden opportunity to preserve wealth and pass it down to our children and charitable foundations,” said Brooks. “In light of record budget deficits, we may not see these exemption levels again for a long time.”

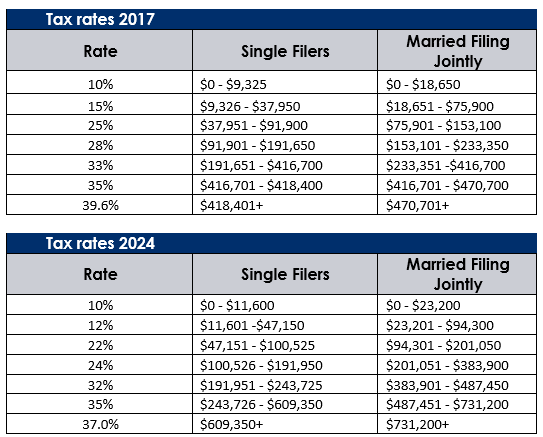

Possible higher marginal tax brackets ahead

The TCJA, which encompasses a number of significant provisions, also temporarily lowered individual tax rates to 10, 12, 22, 24, 32, 35, and 37 percent.

Starting in 2026, those tax rates will revert back to their pre-TCJA, or 2017, levels of 10, 15, 25, 28, 33, 35, and a top 39.6 percent for the wealthiest taxpayers. (Related: How to calculate your net worth)

Until then, however, some may be able to reduce their future tax bill by accelerating income into 2024 or 2025. That can potentially be achieved by selling highly appreciated stock, cashing in stock options, or, for those at least age 70½, using qualified charitable distributions to make direct gifts from an IRA to a qualified charity to reduce their IRA balance and future RMDs. (Learn more: A charitable move with tax and RMD benefits)

Another opportunity to accelerate income and potentially preserve wealth is to convert pretax savings in your traditional IRA to a Roth IRA, a move commonly known as a Roth conversion. The pretax savings you convert would be subject to ordinary income tax today, because those dollars have never been taxed, but you could potentially prevent a bigger tax bill down the road.

Indeed, the benefit of a Roth IRA is that your savings will never again be subject to taxation, including any earnings. Plus, Roths are not subject to required minimum distributions (RMDs), so your savings can potentially generate compounded growth for decades longer, enabling wealthy taxpayers to potentially pass along a bigger financial legacy to their heirs.

With a pretax traditional IRA or 401(k), you must begin taking RMDs at age 72 (73 if you reached age 72 after December 31, 2022) whether you need the money or not. RMDs are taxed as ordinary income. (Learn more: Roth IRA conversions explained)

It is important to consult an estate planning attorney or tax professional before making any decisions that may affect your estate or future tax status.

“No one believes tax rates are ever going to come down, so we should all be planning around the premise that tax rates will either remain the same or go up,” said Naylor.

Higher interest rates

Interest rates remain stubbornly high as the central bank attempts to stamp out inflation. (Learn more: How interest rates work and affect you)

Higher interest rates make it more expensive to borrow money, which negatively affects those who take out a home mortgage, apply for student loans, or carry a credit card balance. But they also benefit savers.

For example, retirees and wealthy investors who are in asset preservation mode can potentially generate a bigger income stream when interest rates are high by allocating more of their savings toward bank deposit accounts (high-yield savings accounts and certificates of deposit) and fixed-income securities, such as bonds and money market funds.

A financial professional can offer guidance on which combination of short-duration securities (and what amounts) might be a fit for your financial goals and liquidity needs.

“High interest rates are generally a good thing for our high-net-worth clients,” said Brooks. “While rates and yield continue to be at respectable levels, we continue to recommend keeping short-term cash in short-duration instruments to maximize their yield while being poised for future opportunities.”

Financial professionals may also help affluent investors optimize their investment portfolio by increasing their exposure to sectors that typically outperform when interest rates rise (financial services) while reducing their allocation to sectors that sometimes pull back (real estate and utilities) when the cost of borrowing climbs. As always, however, remember that past performance is no guarantee of future returns.

Naylor said annuities are increasingly popular among his retired clients who are living longer than ever before and looking for downside protection in their portfolio. (Related: Does an annuity fit your retirement goals?)

“We’re doing a lot more annuities — especially indexed annuities, which are linked to the performance of a market index, for our retirees who want to remain invested but don’t want to take on as much risk,” he said, noting that he typically recommends that older clients allocate no more than 20 percent of their portfolio to annuities. “If you can potentially have some of your savings guaranteed for three to five years at around 5 percent, that may be an opportunity to reduce longevity risk, especially for older individuals who may not need more than 5 percent or 6 percent returns to meet their financial goals.”

Political uncertainty

In an election year, there’s often angst over how stock markets may perform depending on which political party wins the White House. But if history is any guide, those concerns are unfounded.

According to data from LPL Financial, the S&P 500 Index has averaged a 7 percent gain during U.S. presidential election years since 1952. Interestingly, it found that performance is often better in reelection years, averaging a 12.2 percent gain since 1952.1

“We believe this pattern is partly due to the incumbent priming the pump ahead of the election with fiscal stimulus and pro-growth regulatory policies to stave off potential recession and encourage job growth,” the LPL Financial report found. “Every president who avoided recession two years before their re-election went on to win and every president who had a recession within two years before their re-election went on to lose.” (Learn more: 3 ways to financially prepare when elections loom)

Regardless of who wins the election, however, financial professionals caution average investors that the best way to insulate themselves against the political winds of change is to maintain a diversified portfolio that aligns with their need for growth and tolerance for risk. Market timing, in which investors modify their asset allocation based on trends, rarely works, and often undermines long-term returns. (Related: Fix your mix: Asset allocation)

Conclusion

Against a backdrop of economic uncertainty and pending tax law changes, high-net-worth households have ample opportunity to potentially reduce their future tax bill and maximize the financial legacy they leave behind.

By working closely with their wealth management team, they can help build a portfolio that is tax-efficient, poised to deliver long-term growth, and diversified enough to help withstand any political and economic shocks ahead.

Discover more from MassMutual…

Entering the ‘wealth transfer zone'

Stretch IRA: Four possible alternatives

Need a financial professional? Find one here

________________________________________