| ||||||||||||

About 29 percent of workers in their 20s haven’t started saving for retirement, says one recent survey.1 And that’s a missed opportunity, because:

- The longer money works, the better the potential returns.

- Retirement saving offers a chance to reduce taxes.

- A nest egg increases options beyond retirement.

Sure, the resistance to retirement saving is understandable.

For one thing, cultural attitudes toward retirement have changed. Many young workers don’t believe in waiting decades to enjoy the good life. They don’t believe in putting off their dreams until a day that might never come or a day when they might be in less-than-ideal health. They want a job they love now. They want meaningful work now. They want to travel the world now. And there’s nothing wrong with that. (TikTok challenge: Retirement savings)

And there are some pragmatic considerations for those just coming out of college and starting careers or businesses. Some challenges include:

- Student loan payments can impede saving.

- It can be hard to find that first good job out of college.

- Starting salaries aren’t always the greatest.

What’s more, many young workers don’t have access to or don’t qualify for an employer-sponsored retirement plan. Even those young workers who are setting aside money for retirement aren’t usually setting aside a large enough portion of their salaries.

But there is a basic miscalculation in decision-making with not starting as early as possible when it comes to planning for your financial future.

That’s because the earlier you start, the easier it is.

Even if you don’t want a traditional retirement because you plan to enjoy retirement-like activities throughout your working years or because you don’t envision ever wanting to stop working, it’s wise to prepare yourself for a day when you might not be able to work. And having a nest egg gives you options.

By starting early with saving and investing in a retirement account, you’ll likely become self-sufficient and have more control over your life. You don’t want to depend on Social Security, Medicare, Medicaid, or even relatives to take care of you in retirement. They’re all unreliable sources that you can’t control. (Calculator: How much for retirement?)

Let’s break down exactly why starting your saving and investing journey today is so valuable.

The early-start, retirement math advantage

Compound interest is a beautiful thing. It grows your money while you sleep, while you play video games, while you’re at happy hour, while you’re out hiking. All you have to do is invest your money over the long run and leave it alone. (Related: Investing basics)

Here’s how much easier it is to amass a comfortable nest egg when you start early.

Results 2 from saving $475 per month and earning an average annualized return of 8 percent:

|

Starting Age |

Nest egg at age 67 |

|

22 |

$2,379,328 |

|

27 |

$1,594,751 |

|

32 |

$1,060,782 |

|

37 |

$697,371 |

|

42 |

$450,040 |

|

47 |

$281,710 |

|

52 |

$167,148 |

|

57 |

$89,179 |

Here’s another way of looking at it. To have a retirement nest egg of roughly $2.38 million by age 67, assuming an average annualized return of 8 percent, here’s how much you’ll need to save per month depending on how old you are when you start saving:

|

Starting age |

Required monthly savings |

|

22 |

$475 |

|

27 |

$710 |

|

32 |

$1,070 |

|

37 |

$1,625 |

|

42 |

$2,515 |

|

47 |

$4,015 |

|

52 |

$6,765 |

|

57 |

$12,680 |

No matter what, by getting started early on saving for retirement, your investments will do a lot of the hard work for you. You’ll have more disposable income for other things: buying property, investing, traveling, donating to charity, sending your kids to college, or starting a business, for example.

A nest egg of $2.38 million could provide a comfortable retirement for many people. The actual amount you will need to retire depends on many factors, of course, such as what the cost of living is during your retirement years, where you retire, how healthy you are, and what kind of lifestyle you lead. Many opt to talk to a financial professional about gauging their savings to lifestyle and retirement goals.

Reduce your income taxes

When you have money withheld from your paycheck and placed directly into a 401(k) or 403(b), those sums don’t get taxed. The same is true if you have a self-employed retirement account or a traditional IRA.

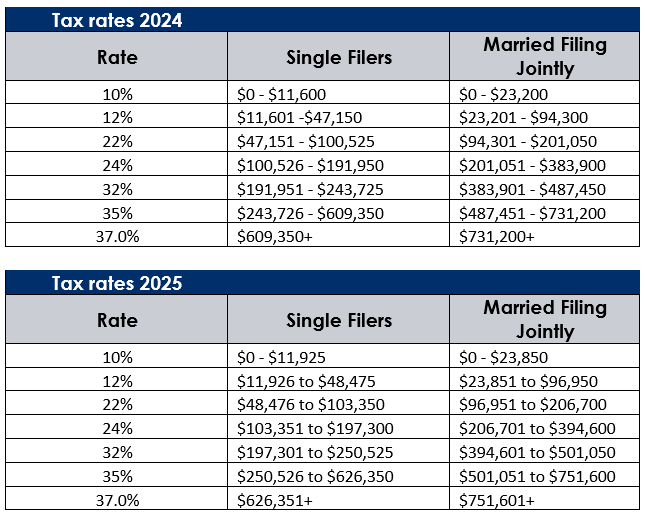

If you’re in the 24 percent tax bracket, you save $240 per $1,000 you contribute to your retirement account. (For the 2024 tax year, the 24 percent tax bracket applies to taxable income of $100,526 to $191,950 for individuals and $201,051 to $383,900 for married couples filing jointly.) That tax savings means you have more principal to invest, which means your money will grow faster.

You will have to pay taxes on all the money when you pull it out in retirement. The hope is that you’ll be in a lower tax bracket then or can do some tax planning to minimize your tax bill. (Related: Income tax diversification)

Even if you save for retirement with a Roth IRA that you contribute after-tax dollars to, you’ll still achieve tax savings in the long term. Your investments in any type of retirement savings account will grow tax deferred. And with a Roth, you won’t pay taxes on the money you withdraw in retirement.

The tax-deferred aspect of all these retirement accounts is a huge benefit that you should start taking advantage of as early in your working years as possible.

Busy, but still saving

Retirement is not the only important thing you’ll need to save for in your life. By developing an early habit of not spending 100 percent of your paycheck, you’ll be better positioned to save for other goals like:

- Building your own business.

- Buying your own place.

- Going on the trip of a lifetime.

If you have trouble developing this habit, try automating it. Determine how much you can save each month, then have that amount automatically transferred from your checking account to your retirement savings. If you’re contributing to an employer-sponsored retirement account, you have no choice but to automate your savings. Your contribution will get automatically deducted from your paycheck and transferred to your retirement account.

Conclusion

Regardless of your views on retirement, getting an early start on saving for your future gives you a huge advantage. The younger you start saving and investing, the less you have to work today to have a financially secure future, because you can let compound interest do the heavy lifting.

Learn more from MassMutual…

7 things financial planning does for you

Working with a financial professional vs. DIY

This article was originally published in November 2018. It has been updated.

_____________________

1 Bankrate.com, “Survey: More than half of American workers feel behind on their retirement savings,” Sept. 25, 2024.

2 This is an example of a mathematical concept. The assumed 8 percent return is hypothetical, and there can be no assurance that any rate of return -- or nest egg amount -- can be achieved.