| ||||||||||||

Cryptocurrency — digital tokens traded through online systems — has become an attention-getting category in the investing world over a relatively short time. And that attention has come for good and bad reasons.

It started out over a decade ago as a financial experiment for digital enthusiasts and outfits with a penchant for new and untested investments. Proponents argued crypto offered a cheap, speedy, decentralized channel for inflation protection. Indeed, some investment companies, banks, and other established financial institutions added cryptocurrency to their portfolios to varying degrees.

But amid the enthusiasm also came some high-profile bankruptcies among cryptocurrency platforms, accompanied by government investigations, lawsuits, trials, and convictions.

Nevertheless, cryptocurrency offerings continue, not only through direct investment but also participation via exchange traded funds and mutual funds. And the category is starting to win over some early skeptics and drawing support from some government leaders.

The question remains: Is cryptocurrency a good investment for the average investor?

Probably not. Most experts advise that only knowledgeable, sophisticated investors with an appreciation for speculation and a high tolerance for risk should consider cryptocurrencies in their portfolio. And, even then, only in a limited way.

“For some, a small allocation, less than 2 percent, may be fine if you are concerned about a hedge for future dollar weakness,” said Daken Vanderburg, head of investments for wealth management at MassMutual. “But cryptocurrencies are not for the faint of heart. They are appropriate only for those who clearly understand the risks and can tolerate the volatility.”

Indeed, the risks are significant. They include:

Added together, those risks present a significant challenge for the average investor, various financial pundits and institutional leaders have suggested.

“My personal advice is: Don’t get involved,” commented Jamie Dimon, chief executive officer of J.P. Morgan Chase, when asked about cryptocurrency for retail investment. “But I don’t want to tell anybody what to do. It’s a free country.”

Understanding risk

When considering cryptocurrency investment, the first place to start is understanding and recognizing your own tolerance for risk. This is comprised of a number of factors, including age, income/savings level, lifestyle, investing knowledge, and personal comfort level with risk. (Related: Why identifying your risk profile is essential to investing)

Your risk tolerance lies at the heart of determining your asset allocation — how much money in your portfolio is in relatively risky investments versus relatively safer investments.

For most retail investors, this comes down to balancing a combination of stocks and bonds. Both types of investments can offer cash flow over time through dividend or interest payments. But they differ in risk.

- Stocks, as a general category of investment, tend to be more volatile than bonds but provide a higher level of return over time.

- Bonds, by contrast, tend to be more stable but generally provide a lower level of return.

So, when an investor is younger and near the beginning of their working years, it might make sense to have more stocks in a portfolio, because there is time to recover from any short-term losses. And as an investor ages, they shift more holdings into bonds to protect against losses as they move into retirement. (Related: Why you can win with a steady investment strategy)

Beyond a basic stocks/bonds mix, some investors add additional types of investments, such as holdings based on commodities or currencies. They can either do this directly or through mutual funds or exchange-traded funds. These types of investments are generally riskier and don’t have an expected cash flow. So, some investors also look for vehicles with guaranteed value over time, like permanent life insurance and annuities, to help mitigate overall risk.

Why would investors put riskier investments into their portfolio? Typically, some investors put riskier investments in their portfolio in hopes of garnering bigger returns. Also, some may have a “fear of missing out” on a popular form of investment. And, if they have the wherewithal, it may pay off for them in the long run. On the other hand, they may incur losses.

In the end, each investor has a different level of risk tolerance. Some people talk with a financial professional to help understand how risk interplays with their own financial goals.

Connect with a MassMutual financial professional

Beyond the general risks common to all investments, cryptocurrency has particular risks that need to be appreciated before jumping in.

Cryptocurrency obsolescence risk

Cryptocurrency essentially uses encrypted computer files as a form of payment. Transactions are verified and records maintained by decentralized networks using blockchain technology, so no government or single entity stands behind the cryptocurrency.

There are a variety of cryptocurrencies in existence — many thousands by some estimates. Two of the more well-known are Bitcoin and Ethereum. But there is obsolescence risk as there is no guarantee that any of these cryptocurrencies will stand the test of time. Many — also thousands by some estimates — have failed.

“It’s a significant risk that is different than other investment vehicles,” said Vanderburg. “No one, for example, knows whether Bitcoin is going to be around in 10 years — or 6 months.”

Cryptocurrency volatility

Nevertheless, although cryptocurrency is less than two decades old, many professional investors have seized upon it, touting its inflation resistance, transparency, and freedom from government control or influence. On the other hand, cryptocurrency has also been criticized for its volatility and use as a medium for illegal activities.

It’s the volatility that any potential investor should be wary of. In the period between 2011 and 2021, Bitcoin was roughly nine times more volatile than the S&P 500 (a leading stock market index) and roughly 30 times more volatile than bonds, according to one analysis.

Indeed, in its early years that kind of volatility led many leading financial and investment pundits to advise against cryptocurrency as a retail investment. And while some have softened their stance, there is still a sense of wariness harbored by many leading money mavens.

“I’ve seen people do stupid things all my life,” said renowned multibillionaire investor Warren Buffett in a televsion interview. “People like to play the lottery ... and cryptocurrencies … they are appealing to the gambling instinct.”

Cryptocurrency value risk

Nevertheless, cryptocurrencies continue to gain speculative interest and have made gains in recent years as a result. Many financial institutions, including MassMutual, now have cryptocurrencies in their portfolios. And there’s been discussion of its future at various levels of government.

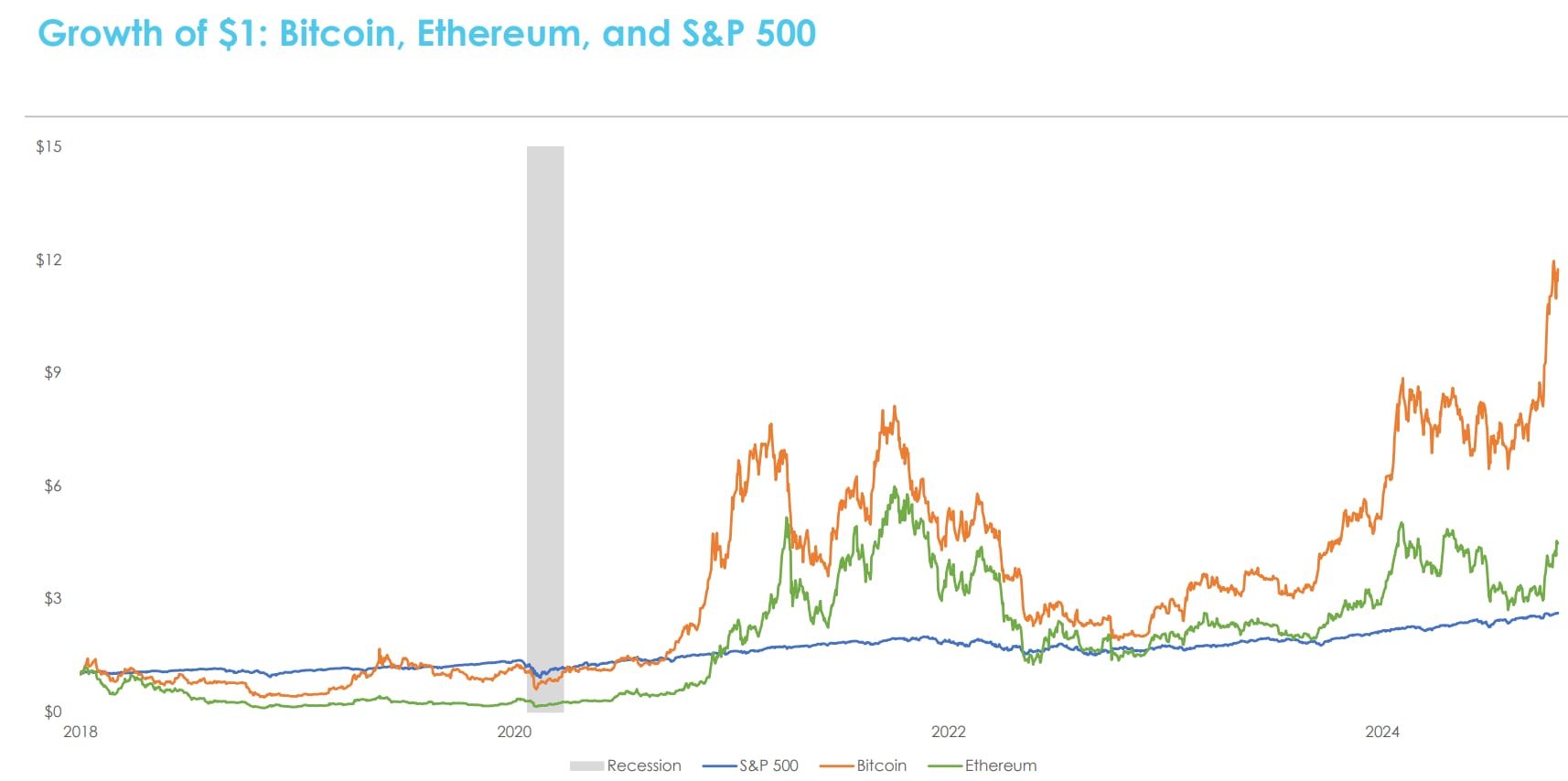

The chart below shows the change in value of $1 entirely invested in either of the two most well-known cryptocurrencies — Bitcoin or Ethereum — or the S&P 500 Index.1

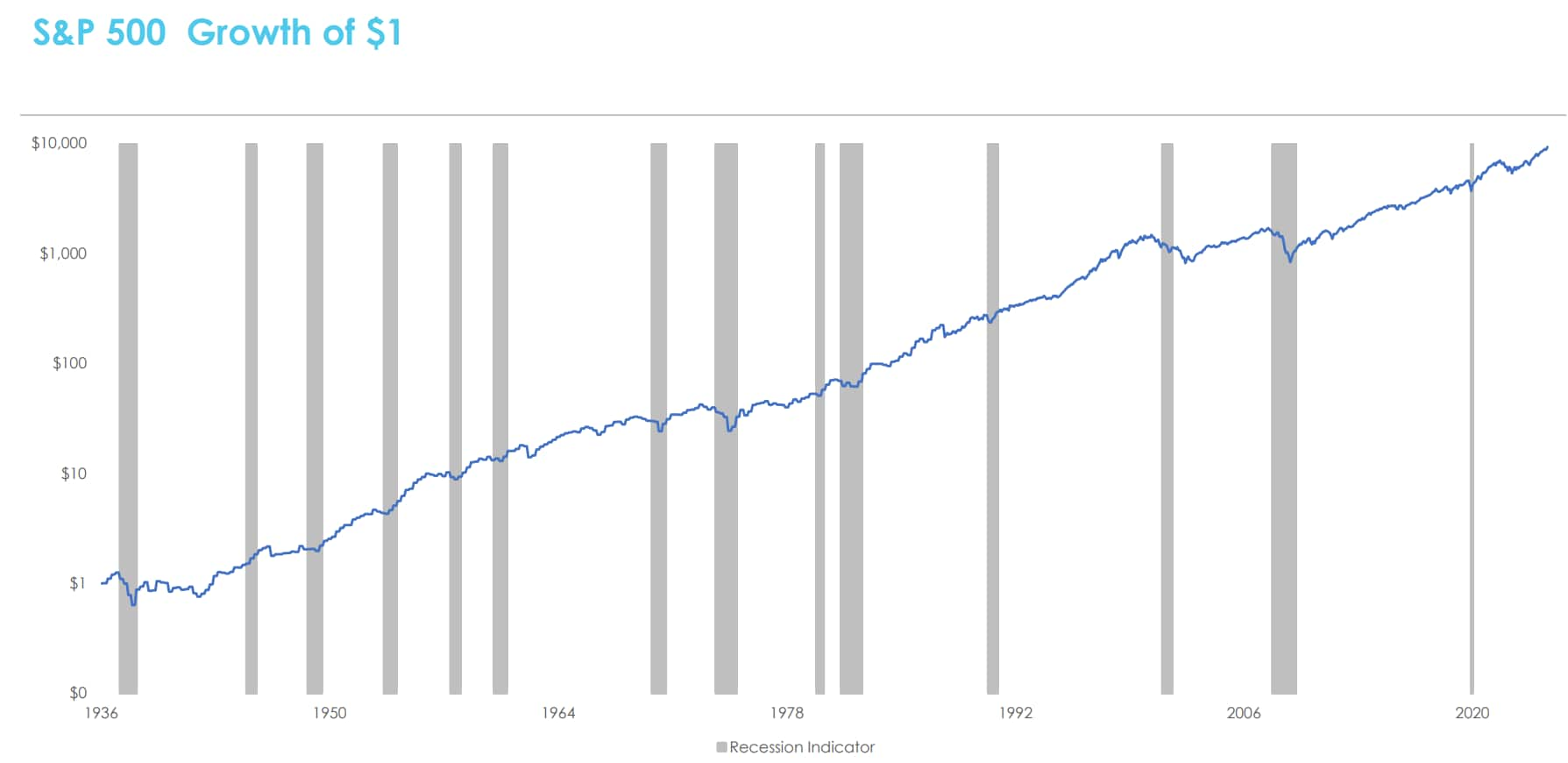

This chart shows recent gains. But it also shows volatility and loss of value for certain periods. Compare that with the historical performance of the S&P 500 in the chart below.2

This chart illustrates steady gains, albeit with some ups and downs (particularly around recessions), in the stock market for roughly a hundred years.3

How does that overall growth come about? Stocks represent ownership in companies that produce goods and control property and means of production — assets. And as those assets produce more, they represent more value.

Similarly, other mainstream investments — bonds, commodities, real estate — have underlying asset value. And currencies, which can fluctuate, are reflective of the value assigned to a particular country’s government policy and economy.

Cryptocurrencies have no such underlying asset base or value. They are simply a means of exchange and a subject of speculation.

“Cryptocurrencies are remarkable innovations, but they are not assets,” said Vanderburg. “They have seen rapid adoption and significant increases in market value in a very short period, but there is no structural reason to believe they will increase as equities, bonds, and real estate have done historically. At best, beyond basic speculation, they can be a small hedge against fluctuations in other mediums of exchange, like currencies. But I wouldn’t advise a large holding for an individual investor.”

Cryptocurrency hacking risk

As a digitally based form of financial value, cryptocurrencies can obviously be the target of hackers. And already a number of costly cyberattacks have taken place at various cryptocurrency platforms over the years. And, unlike banks, accounts on those platforms are not covered by the Federal Deposit Insurance Corp.

That kind of hacking is not a risk with stock and bond investments, which typically make up an average investor’s portfolio.

No cash flow for crypto

Additionally, cryptocurrencies provide no cash flow. Many companies, however, issue regular dividends to stockholders. And bond owners typically receive interest payments on their holdings. And real estate investments can also provide a steady stream of income.

“Cryptocurrency simply doesn’t provide any expected cash flow, whereas bonds, equities, and real estate do,” observed Vanderburg.

Conclusion

Access to cryptocurrencies is becoming easier as more and more financial trading platforms and exchanges are offering various investment products.

But before choosing to invest in cryptocurrency and deciding on a platform, probably the wisest course of action would be to consult a financial professional and carefully consider your financial goals and tolerance for risk beforehand.

Discover more from MassMutual …

5 tactics for investing in your retirement

How life insurance can help your retirement

What should investors do about inflation?

______________________________

1 Source: Bloomberg as of November 30, 2024. Past performance is not indicative of future results. Inception date for calculations is first common based on Bloomberg data feeds (2/8/2018) and the graph is portrayed in log-base 10 scale (exponential growth base factor 10). The S&P 500 Index pays dividends, Cryptocurrencies do not. Dividends reflect past performance and there is no guarantee that they will continue to be paid. Past performance does not guarantee future results. Index returns include the reinvestment of income and dividends. Indexes are unmanaged, and do not have fees or expenses. You cannot invest directly in an index.

2 Source: Bloomberg as of November 30, 2024. Index returns include the reinvestment of income and dividends. Indexes are unmanaged, do not have fees or expenses. You cannot invest directly in an index.

3 Source: FRED and Bloomberg as of November 30, 2024. The S&P 500 Index pays dividends, Cryptocurrencies do not. Dividends reflect past performance and there is no guarantee that they will continue to be paid. Past performance does not guarantee future results. Index returns include the reinvestment of income and dividends. Indexes are unmanaged, and do not have fees or expenses. You cannot invest directly in an index.