| ||||||||||||

It’s never a bad time to review your progress toward your retirement goals, but your 40s is an especially important time to do so. Why? Because you’ve probably been working for about two decades, and you still have two to go until traditional retirement age. You’re at a midpoint in your working life where you can assess what’s worked so far and what you might need to change.

Many 40-somethings are juggling all sorts of expenses, from paying off a mortgage to raising children. Staying on track — or getting on track — with your retirement savings plan might feel daunting at this stage of life. On the positive side, you may be well-established in your career and enjoying the highest earnings of your life. (Related: Behind on life's milestones? Maybe not)

Of course, that’s not true for everyone: Some people may have experienced financial setbacks related to a job loss or health challenges. Some 40-somethings may be underemployed for the level of education they’ve earned (and are still paying for). Still others may be caring for a special needs child or an aging parent.

Regardless of the hand life has dealt you so far, here’s what you can do now to see where you stand and to begin making progress toward a comfortable retirement in your 60s.

- Evaluate your progress toward popular benchmarks.

- Assess whether those savings goals are realistic for you.

- Start working toward longer-term goals.

Let’s start with some common guidelines for how much you should have amassed for retirement by midlife.

Connect with a MassMutual financial professional

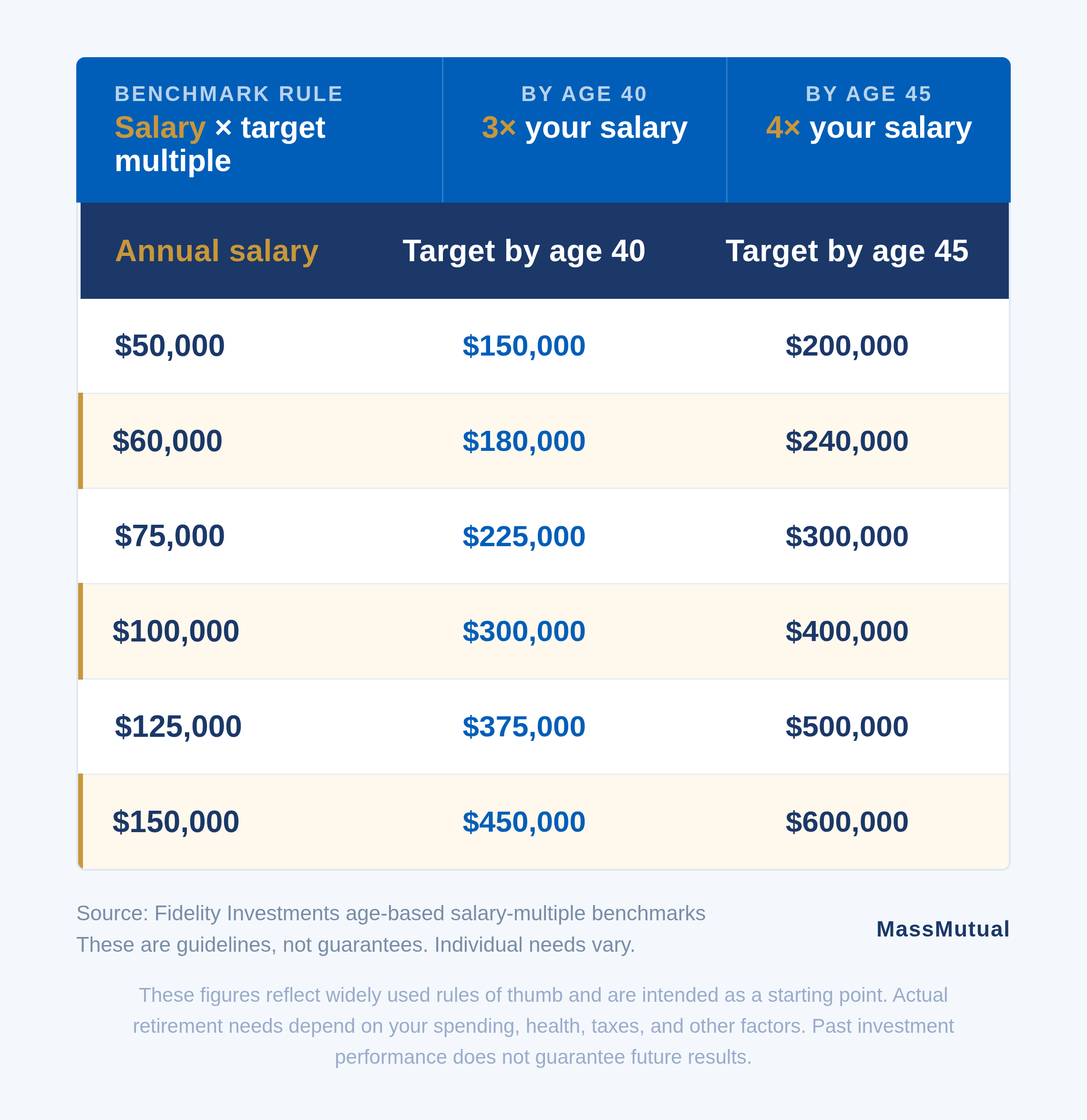

How much should you have saved by 40?

The following savings guidelines can be a starting point for evaluating your progress toward a fully funded retirement. These rules of thumb say you should have saved ...

- 3 times your income by age 40.

- 4 times your income by age 45.

These income-based targets assume you can live on a similar or slightly lower income during retirement. The absolute dollar amount you need for retirement can vary a lot depending on where you live, health needs, and other variables.

But using these guidelines, you get this math …

No matter how much you earn, these amounts might seem high, especially if you’re raising children, have high medical expenses, or are paying off a mortgage. You might also have realized that if the goal is to save a percentage of your income and your income changes, then you’re chasing a moving target. However, if you aim to save a consistent percentage of each paycheck (financial professionals typically suggest 15 to 20 percent) and not a fixed dollar amount, you may be able to keep up.

Savings goals in your 40s: Are they realistic?

For Gen Xers, millennials, Gen Z, and the younger generations that follow, achieving the above goals can be challenging. The members of these generations are often faced with high student debt loads and tough economic conditions. Also, especially for those living near growing urban centers like Silicon Valley or New York, living expenses can be significant and the high cost of real estate can put home ownership out of reach.

As a result, the standard advice to not take on debt is a privilege, not the norm, said Alejandro Mendieta, a managing partner of Coastal Wealth, a MassMutual firm and one of the largest financial services firms in Florida. But, he noted, there may be a solution: A financial plan with a time-bound goal to pay off debt, combined with a savings plan to keep pace with inflation and achieve growth toward set goals. (Related: Establishing a financial plan)

“If you have a financial plan to reference, you know what you can and can’t do,” Mendieta said.

A plan that balances earnings against expenses can empower you to meet daily, weekly, monthly, and annual goals for becoming debt free and saving for a comfortable retirement while still enjoying activities like travel and dining, but with a limit.

Thinking longer term

What if you’re already in your 40s and it’s too late to meet the above goals? Here’s how you might get back on track for the long run.

Let’s say your annual income is $100,000 and you want to have 10 times your income saved by retirement. The examples below show how you could save $1 million by age 65 if you’re now age 40 or 45.1

Obviously, your contributions at age 45 need to be higher to achieve the savings goal, since there is less time to meet it. Both examples assume that you’re starting with a nest egg of $50,000, making contributions at the end of every two weeks, and that you’ll have a strong allocation to stocks in your investment portfolio, earning a conservative hypothetical 8 percent annual return that is consistent with the historical returns of the stock market. (Learn more: Why a balanced asset allocation is never one and done)

Saver 1: Age 40

Goal retirement age: 65

Years to accumulate retirement savings: 25

Biweekly savings: $305

Assumed annual investment return: 8 percent

Total savings by age 65: $1,001,620 before taxes and inflation

Saver 2: Age 45

Goal retirement age: 65

Years to accumulate retirement savings: 20

Biweekly savings: $590

Assumed annual investment return: 8 percent

Total savings by age 65: $1,004,352 before taxes and inflation

Of course, average annual returns of 8 percent may not be achievable. Market-based investments have risk and past performance doesn’t guarantee future performance.

Further, emotion-driven market timing prevents many people from achieving the same returns as the market and causes them to underperform. And some people may not be comfortable with a heavy asset allocation to stocks.

If we instead assume a 5 percent average annual return using the examples above, our 45-year-old ends up with $662,546 by age 65, and our 40-year-old ends up with $569,070.

Will one million or half a million dollars be enough for a comfortable retirement? Not for everyone. But it could be better than relying on Social Security alone. MassMutual’s retirement calculator can help you see if you’re on track for retirement.

How a financial plan can help

You don’t have to work toward these major life goals alone, and you’re more likely to achieve them with a plan. What’s in that plan will depend on individual circumstances and what kind of financial vehicles — workplace retirement programs, IRAs, investment portfolios — are available. (Related: 3 strategies to boost your retirement savings (even if you're behind))

Many people find having help from a financial professional to formulate a plan and keep it on track gives them a leg up.

“Working with a financial professional who can hold you accountable is essential,” Mendieta said. “Your financial plan is just as important as finding the right financial professional who can hold you accountable, be your coach, and help you to achieve a comfortable retirement regardless of the challenges you might face.”

Since 1851, MassMutual has been focused on helping people secure their future and protect the ones they love. That purpose is why we have thousands of financial professionals to assist you on your journey through insurance, investing, retirement planning, estate management, and more. You can find a MassMutual professional with this tool or you can let us know you’d like to talk to one and we’ll have one of our financial professionals contact you.

___________________________

Frequently Asked Questions about retirement savings in your 40s

Q. What if I'm behind on retirement savings in my 40s?

A. Being behind is more common than you might think — the majority of Americans fall short of benchmark targets at every age. The key is to start closing the gap now by increasing your savings rate and taking full advantage of any employer 401(k) match.

Q. How much should I be saving each paycheck in my 40s?

A. Financial professionals generally recommend saving 15 to 20 percent of gross income for retirement. If you're starting from a smaller base in your 40s, even modest increases — such as saving $305 biweekly starting at age 40 — can grow to over $1 million by age 65 at an assumed 8 percent annual return, as outlined above.

Q. Is it too late to catch up on retirement savings if I'm in my mid-40s?

A. It's not too late, but the math becomes more demanding the longer you wait. A 45-year-old would need to save roughly twice as much biweekly as a 40-year-old to reach the same $1 million goal. Working with a financial professional can help you build a realistic plan.

_________________________

Discover more from MassMutual…

Retirement savings catch up: 3 moves

How to get, or keep, your retirement savings plan on track

3 financials to check on your birthday

This article was originally published in November 2020. It has been updated.

_________________________