| ||||||||||||

This election season was volatile, emotional, confusing, unpredictable, and yet … also reliable, fair, and secure. And the outcome was a representation of how Americans voted. In this market analysis I will try to provide some hope for those downtrodden souls and some temperance for those feeling excessively cheerful. And along with that perspective, in my conclusion, I’ll dare to request something from you for the most perilous of political venues: the upcoming Thanksgiving dinner.

Elephants and donkeys

One of the more interesting aspects of the human psyche is how often the aperture we have directly affects the statements we make. As a particularly timely example, I was recently told within a 24-hour period how much better Republicans are for stock markets, which was then followed by a just-as[1]adamant statement about how much better Democrats are for stock markets. Both humans were similarly confident and well-informed. What’s fascinating to me is that neither is correct.

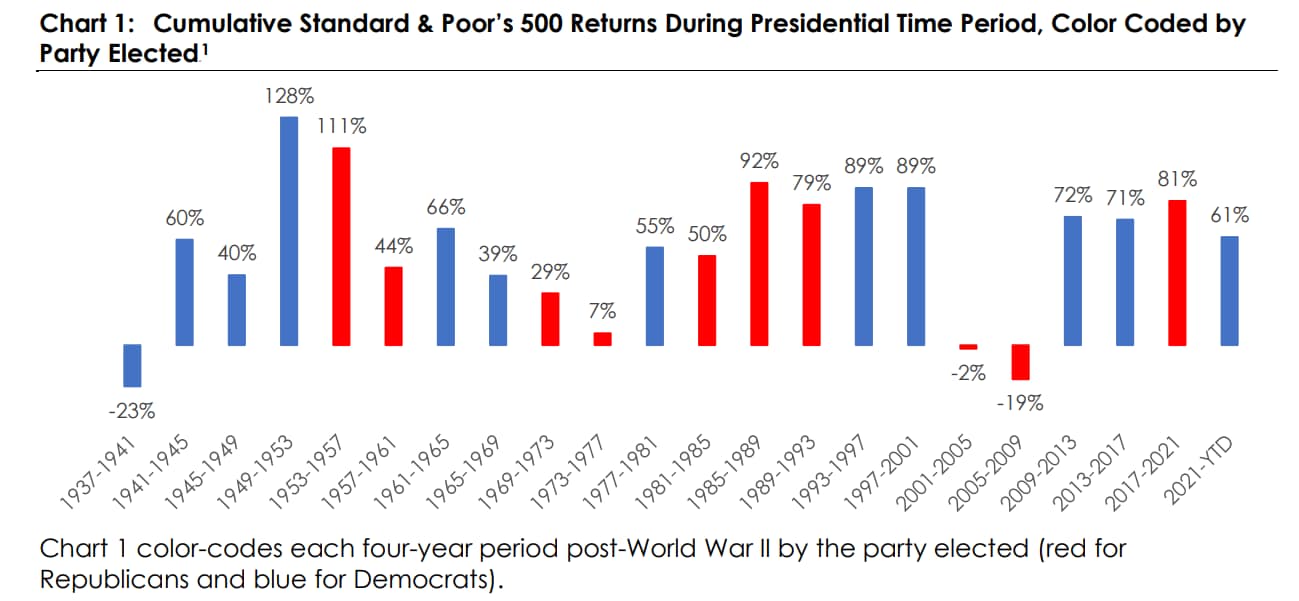

Which brings me to Chart 1.

There are several obvious takeaways.

- First and foremost, the vast majority of four-year return time periods are positive, and significantly so.2

- Second, there is no statistical significance between the red bars and the blue bars. Some are higher than the average, some are lower than the average, but there is clearly no discernible pattern.

Checks and balances

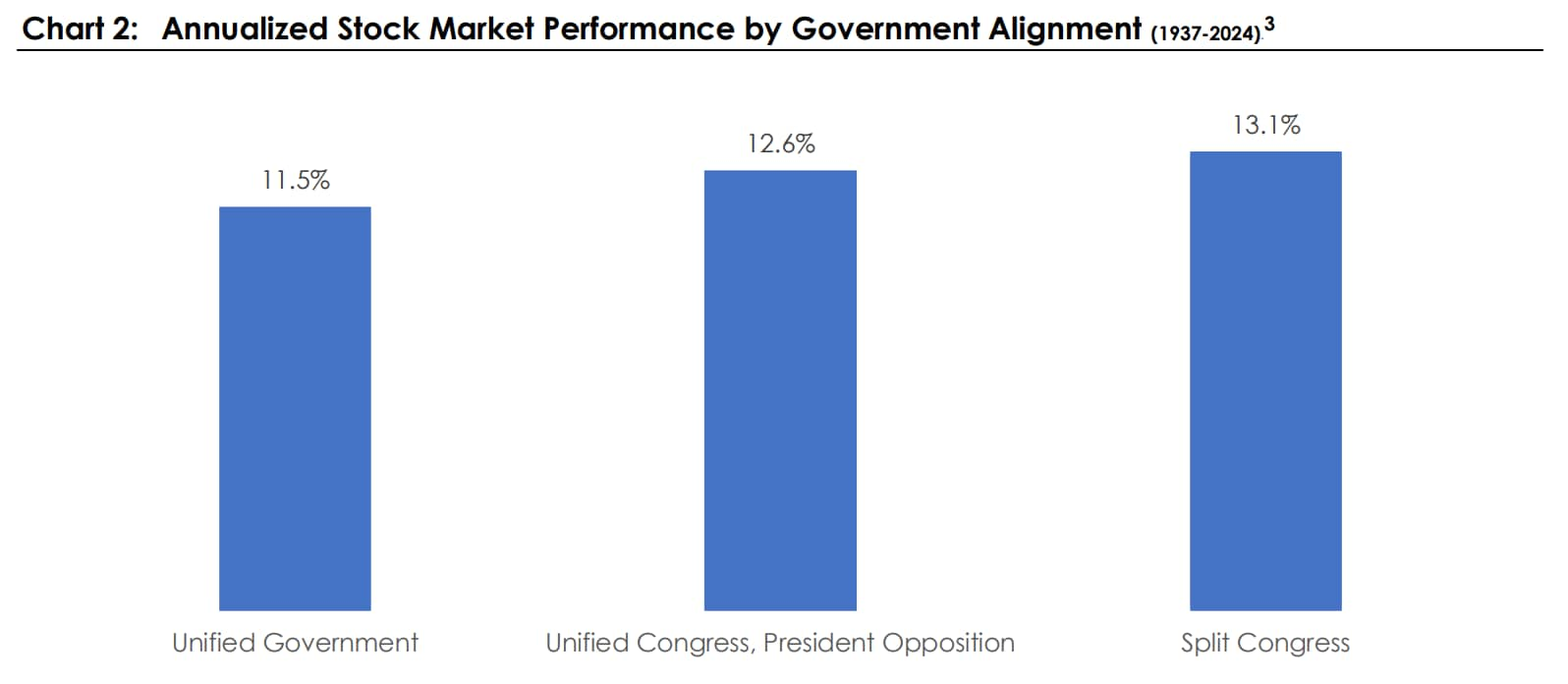

“But, but, but” I then hear…this time is different! Aha … which brings me to Chart 2.

Chart 2 shows annualized stock market performance as impacted by government alignment. The first bar is the annualized return of the S&P 500 when the Senate majority, the House majority, and the presidency have been represented by the same party. The second bar is the annualized return when the Senate and House majorities have been the same party, but the president is of a different party, and the third bar is when the Senate and House majorities have been opposite parties, and we ignore the party of the president.

Blur your eyes, and I think you will notice two important takeaways.

1. All returns are material, and all returns are VERY similar.

2. Having checks and balances (as shown in bars 2 and 3) tends to increase returns slightly.

Are these differences statistically significant? Absolutely not. Are they logical? I think so. My thesis is that when congress is divided, the parties must work together to get any legislation through and, when that occurs, only the most compelling and reasonable legislation gets approved. Is that right? Well, it’s impossible to discern … but it does seem aligned with the guiding principles of how this country was founded.

Does that mean this next four-year period will be the same as above with Republicans now controlling the Senate, the House, and the presidency? Absolutely not, as there are far too many variables at play to predict with any precision … but it should give us all some reassurance that there is very little difference between the above returns regardless of the alignment of power.

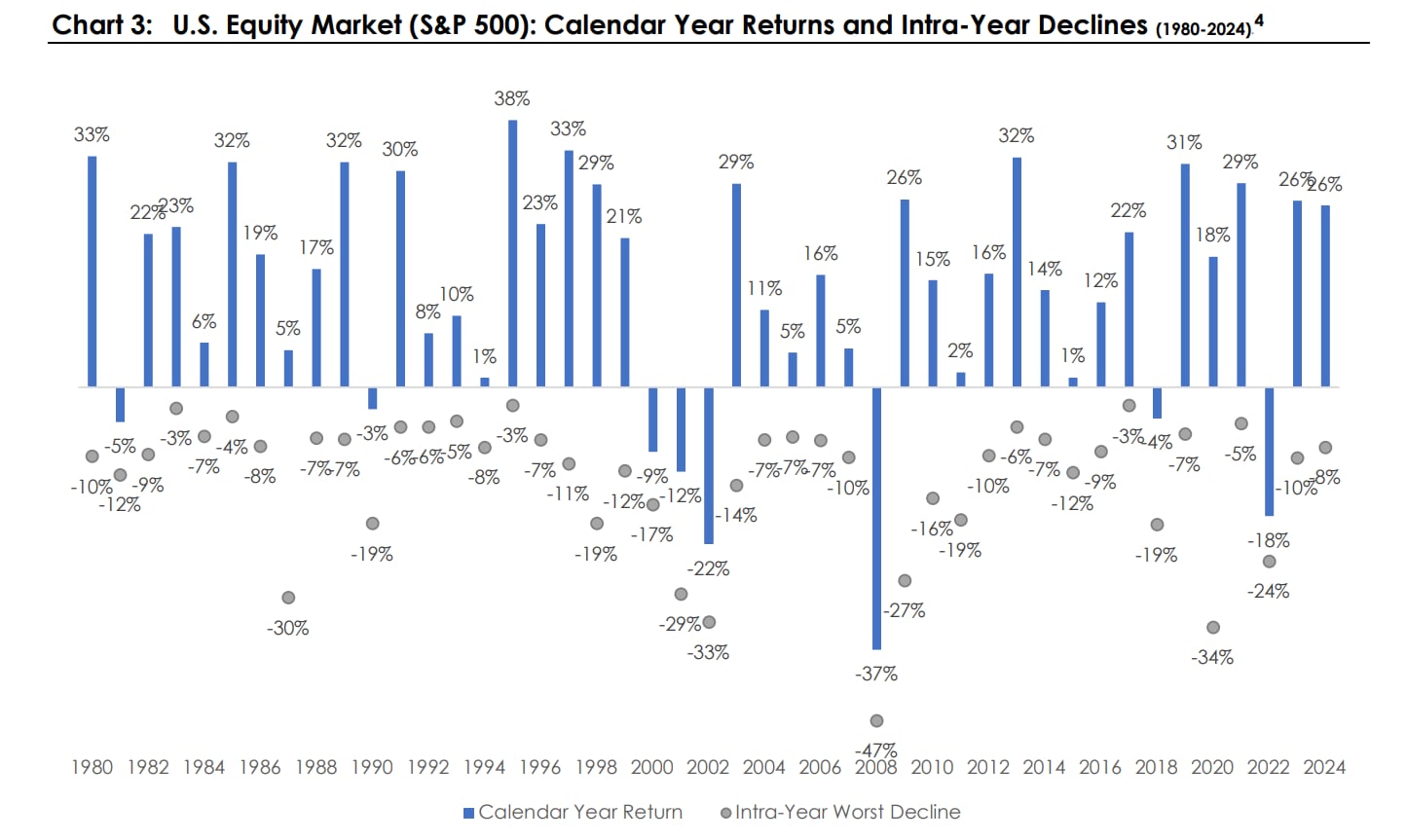

Which brings me to my final chart today…my beloved “dots and bars” chart.

Let’s start with the grey dots. Those are the worst selloffs in each individual year. So, for example, at some point in 1980, the market was down 10 percent, and at some point in 1981, the market was down 12 percent.

The blue bars are the calendar year returns. So, in 1980, for example, from Jan. 1 through Dec. 31, the market was up 33 percent, and for the 1981 full calendar year, the market was down 5 percent. Those full returns are INCLUDING the selloffs represented by the grey dots.

Now think about what was happening during those years from a presidential standpoint. We had Ronald Reagan for eight years, then George H. W. Bush, then Bill Clinton, then George W. Bush, then Barack Obama, Donald Trump’s first term, Joe Biden, and now Donald Trump’s second term. We’ve had crashes, rallies, inflation, deflation, great monetary policy, and dubious monetary policy. We’ve had budget surpluses, deficits, and everything in between. We’ve had trade surpluses and trade deficits plus chaos around the globe, political escalations, a pandemic, health scares, minor skirmishes, major conflicts, and countries falling apart and then being rebuilt.

And yet… look at the chart.

- First, EVERY single year has a selloff of some sort. Expect it. It happened in 2024, and it will happen in 2025 and every single year going forward. It’s healthy and something we should understand is part of the capitalist process. It doesn’t mean the world is ending, and it doesn’t (necessarily) mean our political system is doomed.

- Second, if we then look at the calendar year returns, MOST of them are positive, and MOST of them are very meaningfully positive. Said another way, markets generally move higher NOT because of the president, but because of incentives. And incentives are created as the result of capitalism … and those incentives remain the same regardless of who is (or isn’t) in office. Can our politicians change the incentives? I tend to think no, in aggregate, but they can certainly lean on certain policies to nudge those incentives in certain directions.

All in, have faith and focus on the long term. Whether the outcome of this presidential race was disastrous or ebullient for you, keep in mind that any individual person is just a person. They wake up every day, have a cup of coffee, put on their pants … and just like many of us, do their best to impact a system that is complicated, very well entrenched, and mostly driven by incentives that have been very well worn.

And with that, if you have made it this far, you certainly deserve a reward but, unfortunately, I can offer only a request. We, as Americans, are approaching that most treacherous of meals, and this year is particularly so: the Thanksgiving dinner. If you believe the election results reflect the make-up of the country (as I do), then there is a very good chance that the person sitting to your right or left at Thanksgiving will likely not hold your views. As such, might I suggest we leave politics on the sidelines for this one small window of time. With the likelihood of changing your neighbor’s mind being close to zero, and in the context of this election season being particularly heated … perhaps let us discuss the weather, the cardinals on the back porch, the football game on TV … or the things that we have in common, not those that separate us.

After all, there is far more that unites us than divides us … and as the world’s wealthiest and most prolific country in all of human history … we certainly have much for which to be thankful. Happy Thanksgiving.

Discover more from MassMutual …

Market volatility?! Two charts to help soothe investor worries

The three keys to choosing your investments

Why AI can’t replace your financial professional

_______________________

1 Source: Bloomberg, WMIT, through Aug. 20, 2024

2 Note: FDR was the first negative bar (1937-1941) along with George W. Bush in the 2001-2005 and 2005-2009 time periods

3 Source: Bloomberg, WMIT

4 Source: Bloomberg, WMIT