| ||||||||||||

Well, that’s it, folks. 2022 has ended and 2023 is now upon us. And for those of us in the investment industry, it is also a time to grab a bowl of popcorn and sit back and wait for the annual rite of passage for investment organizations: the publishing of market predictions.

Personally, I have made a bit of a habit to collect these over the years and then, with the benefit of hindsight, review how accurate they were. Take a quick gander at some of the recently published:

- A well-respected Wall Street firm recently clarified that U.S. equity markets were certain to be down for 2023 because we are heading toward a certain recession. Well, that’s unfortunate.

- Yet another, also well-respected firm, recently stated that we have made it through the challenges over the past several years and 2023 could be one of the best years in many. Ahh, I like that much more.

- Another firm said the Standard & Poor’s 500 will be up 11.4 percent this year (I commend them on their very helpful precision).

- Yet another said equities will be down in the near term but didn’t clarify exactly when.

If all of that is a bit too clear and mundane for you, perhaps listening to the pundits and experts on the future of cryptocurrencies is more helpful? One recent expert believes bitcoin could be up 1,400 percent this year, while another bank is equally certain the market has underpriced the risk and bitcoin is likely to be down 70 percent in 2023.1 Hmmm…. (Related: Should crypto be in your portfolio?)

Which leaves the average investor with an enormous challenge … if the most sophisticated and well-equipped organizations on the planet disagree on the future of the market … what are each of us to do?

Well, first, let us take stock of what has occurred and what is occurring now. Perhaps by focusing on getting the big things right, we can reduce the chances that the smaller things get in our way.

The difficulty of a difficult year

Much has been said about how painful 2022 was and yet I still don’t believe most investors know how rare it was.

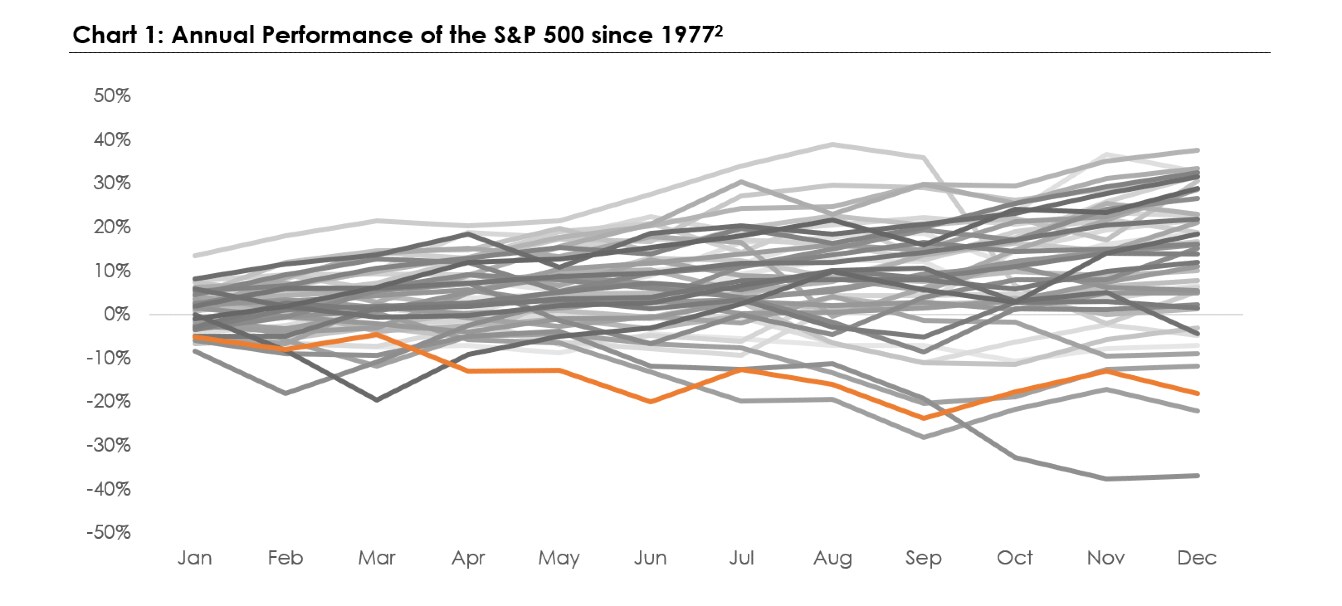

The following chart helps paint that picture.

Chart 1 takes the total performance of the S&P 500 in every year since 1977 and plots them on the same timeline. The orange line is 2022. That’s right, you’ve just lived through the third worst year in equity market history since the late 70s. It’s worth noting the absolute worst year was 2008 (“the end of capitalism” as some pundits referred to the Global Financial Crisis…), and the second worst was 2002.

OK, you say, yes, I know equity markets went down…we all saw the red on our statements.

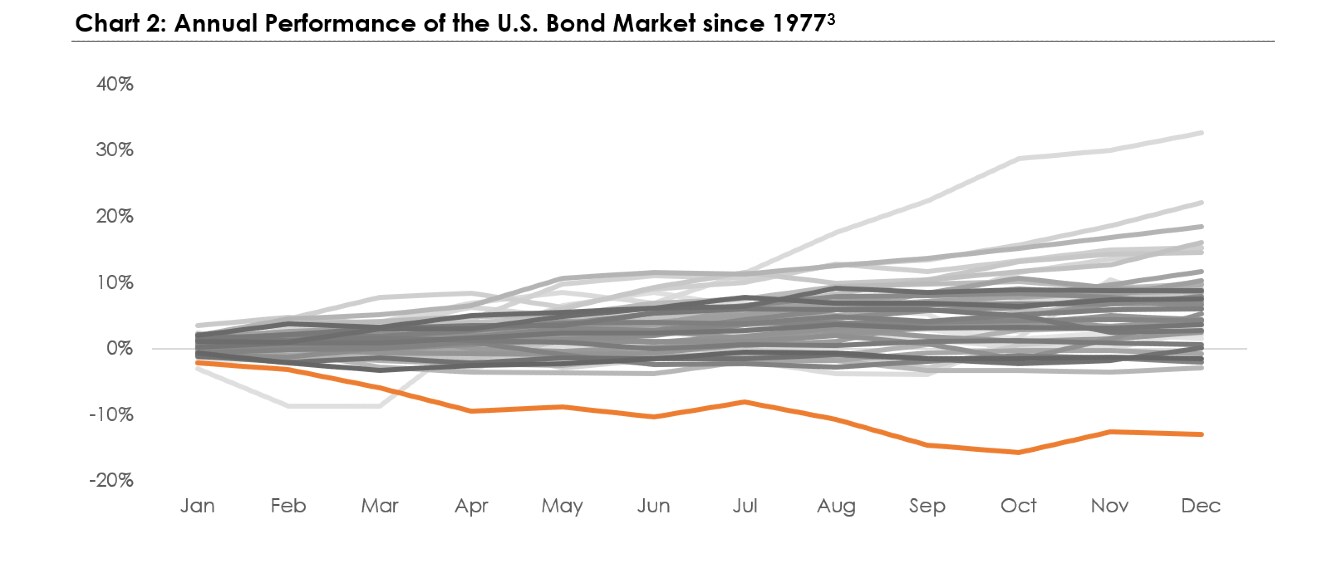

What was different (as we have discussed several times in these updates) is that there were very few places to hide. Historically, during difficult years, bonds have been a buffer for equity market performance and have helped mitigate losses. In 2008, for example, equity markets were down more than 22 percent, but bond markets (as proxied by the U.S. Agg) were up more than 5 percent, which is following a nearly 7 percent return in 2007 and was followed by a nearly 6 percent return in 2009. During that time, at least, bonds helped mitigate the pain felt by equity markets declining.

Chart 2 demonstrates just how bad 2022 was in the bond market.

Put those together and, well, as you might be painfully aware … 2022 was a difficult year to navigate.

Yes, but what do we do with that information? What do we do now that 2022 is over? Is inflation over? Will the Ukrainian conflict end? What … in other words … is the average investor to do?

Let us now turn to what we know about the current economy because, after all, markets, over the long-term, reflect the underlying economy. While we are never arrogant enough to state with certainty what the future holds, we do believe that adept students of history should at least be able to lean toward getting the big things right … or at least not terribly wrong.

The sky is not falling

Anytime anyone asks you about the economy, you should immediately think about two dynamics: growth and inflation.

- How is the economy growing?

- And how stable are prices?

Are there other dynamics? Yes. But many of those dynamics are symptoms, or causes, of growth and inflation.

As such, let us look at the U.S. economy…that historical bastion of global growth.

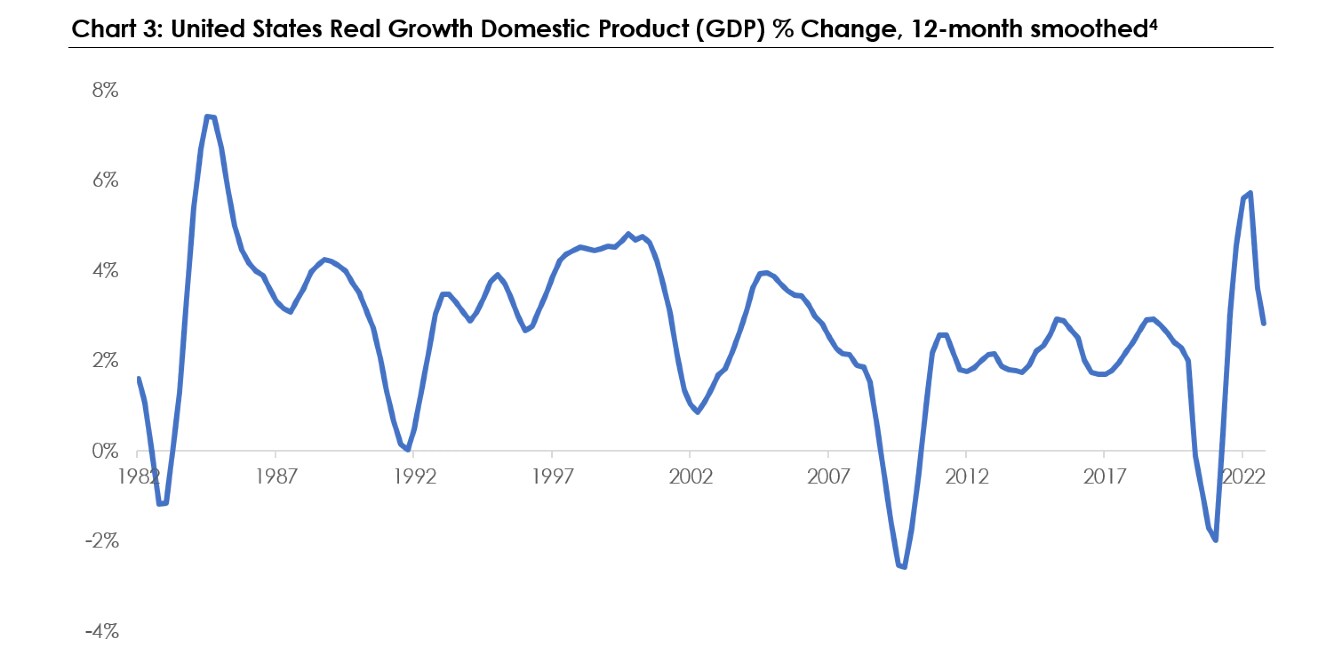

First, some definitions. To measure how much an economy is growing, we simply look at how much a country produces and then measure the change over time. This measure of how much a country produces is known as gross domestic product, or GDP.

The problem with that measure is that it doesn’t account for the fact that prices move around every month. So, if in January prices went up 10 percent, even if the economy didn’t grow 10 percent, then our readings will reflect a different number than we intend. To account for that problem, we must adjust for that effect to determine actual economic growth (what we refer to as REAL GDP).

Chart 3 above shows that data. What is obvious is that:

- The economy is still growing.

- The economy has slowed a bit.

What we should also find reassuring is that the economy is doing something similar to what it has done many times over the past 40 years ... nothing looks particularly extraordinary.

Yes, but who cares you might say! Inflation has been the problem! Fair point, let us look at inflation.

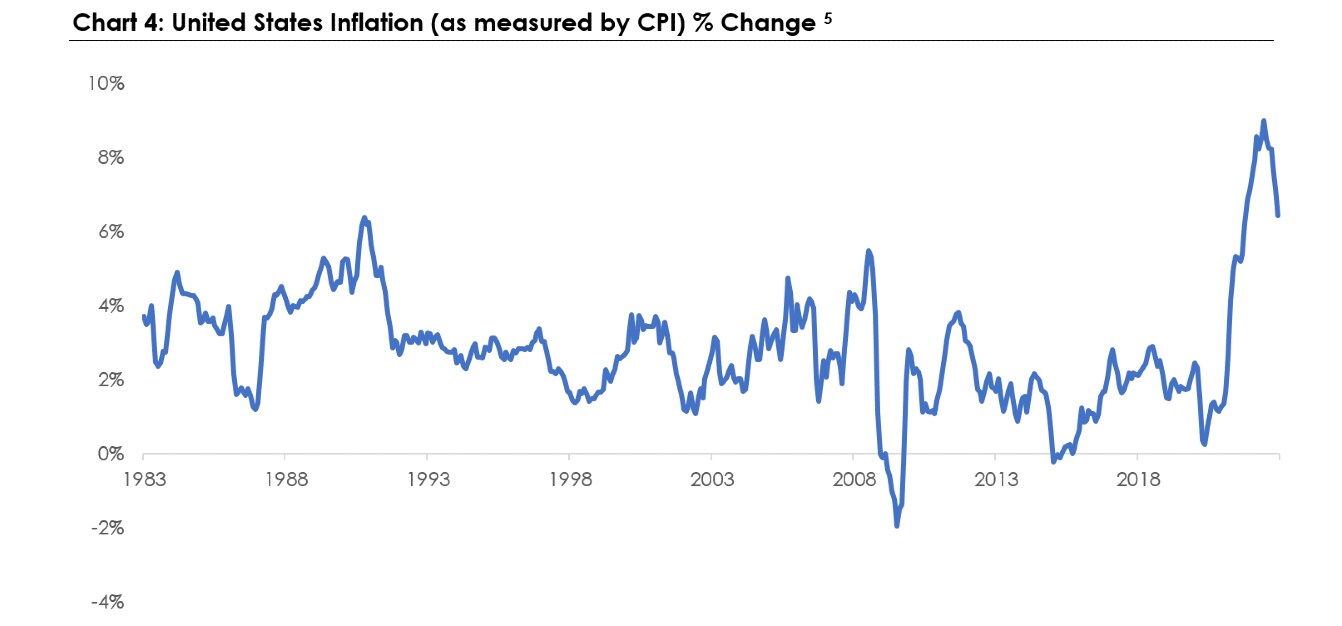

Chart 4 shows that data.

My interpretation of this chart is, again, twofold:

- Inflation is higher than it’s been in 40 years.

- Inflation has begun to fall (as we’ve discussed several times in recent market updates).

Perspectives and summaries

Let’s take stock of what we’ve learned thus far:

- 2022 was one of the most difficult years on record for stock and bond markets.

- U.S. growth is still reasonable, although slowing.

- U.S. inflation is high and yet falling.

And while, admittedly, if you give those three observations to 10 different economists, you will likely have 20 different opinions. My takeaway is simple: The sky is not falling.

Unfortunately, difficult years are simply a part of investing. If there were a way to avoid them, we would (and yes, I’ve tried and failed), and yet those corrections are healthy readjustments to re-align incentives and retract risk.

Markets don’t go up because they should. Markets go up because they reflect cash flows, and cash flows grow as a function of the underlying economy. The economy grows because of its inherent incentives … which, yes, can be negative and destructive, but are generally positive and useful.

In investing, there are very few secrets, but one of them is to get the big things right: Minimize costs and taxes, avoid emotional decisions, stick to your plan (and make sure you have a plan in the first place), and always save more than you think you need.

Discover more from MassMutual …

What’s behind the real estate market shadows?

When markets dive, keep your strategic calm

How higher interest rates may hit consumers

________________________

1 https://www.cnbc.com/2023/01/02/the-boldest-bitcoin-price-predictions-for-2023.html

2 Source: Bloomberg, MassMutual WMIT Research, as of Jan. 27, 2023.

3 Source: Bloomberg, U.S. Treasury, MassMutual WMIT Research, as of Jan. 27, 2023; referencing Bloomberg US Aggregate Bond Index, a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States.

4 Source: St. Louis Federal Reserve, MassMutual WMIT Research, as of Jan. 27, 2023.

5 Source: St. Louis Federal Reserve, MassMutual WMIT Research, as of Jan. 27, 2023.