Please take out a writing implement and a piece of paper. Number the paper from one to four, and answer the following questions:1

- What is the official language of the United States?

- Why were women burned at the stake in Salem?

- What job did Walt Disney have when he drew Mickey Mouse?

- On which spaceflight did humans first lay eyes on the Great Wall of China?

These questions remind me of inflation.

Why, you ask? Well, let’s review the answers.

The United States has no official language, suspected witches were hanged in Salem not burned, Walt Disney didn’t draw Mickey Mouse, and it is not possible to see the Great Wall of China from space.

As with inflation, these questions are perfect candidates for feigned knowledge. The idea that we vaguely understand something, or remember an anecdote we once heard, and therefore (particularly those of us in finance) use that fickle foundation of knowledge to make predictions or allocation decisions.

And yet, the green shoots of inflation seem to be appearing everywhere, and often without the commensurate knowledge to unpack the implications. After all, it has been decades since inflation has been a force worth mentioning, and many market participants today have never had to deal with its effects.

Therefore, today, let us focus on inflation. We will start with some basic definitions, and then turn to possible paths, and lastly, thoughts on what instruments to consider should one believe inflation to be a material risk.

With that, let us begin.

Inflation

Imagine a man who lives in a nice little village with cobblestone streets, quaint rock walls, and a picturesque stream running through the town center. Every day, the man goes down his wooden stairs, out the sturdy front door, and around the corner to the town bakery. On the first day we encounter this man, he buys one loaf of bread, and it costs him one dollar. He takes the bread home to feed his family and proceeds to enjoy the rest of the day. On the next day, he follows the same routine, but when he enters the bakery, the bread is now $1.10. No big deal he thinks, what is a dime? The day after that, same routine, same bakery, and same bread, but this time the loaf of bread is $1.21.

This is inflation. Simply defined as the price of a good or service increasing over time. Deflation is the opposite: prices going down over time.

That’s it — you now know more about the fundamentals of inflation than the majority of Wall Street.

Interestingly, we can also restate that analysis by looking at the value of the dollars purchasing those goods. Said another way, while we agreed the bread increased in dollars, we could also state the dollars now purchase less bread … and by extension, the dollars themselves are clearly worth less (we will come back to this shortly).

Yes, but not fair you say, that was an extreme example! That was 10 percent per day! Well, yes, true. Yet in Germany during the Weimar Republic following the first World War, inflation approached several hundred percent per day … many multiples of our little examples. Venezuela and Zimbabwe have had similar experiences in the last several decades as well, although the data is notoriously unstable.

Imagine how destabilizing that is. As consumers, we would have no idea how expensive a good was going to be in a day, a week, or a month, and thus our incentives would be to purchase more goods more quickly … which means we would be saving less, and businesses would be investing less. For producers, they would have a hard time figuring out their cost of production because the raw inputs are changing so quickly, and thus they would have a very hard time planning for the future. If they charge $10 for a loaf of bread, but the cost of their inputs is now more than $10, they would effectively be losing money on the sale of each loaf! In aggregate, this process of rapid inflation therefore encourages consumers to spend more (and save less), which moves prices even higher, and thus makes the currency worth less.

With the definitions out of the way, let us make this more relevant to today. In an effort to avoid single viewpoints, let us look at this data through three (fairly simplistic) lenses:

- Business, as viewed through manufacturers.

- Consumers, as viewed through prices paid.

- Government, as viewed through the Federal Reserve Balance sheet.

Business through the manufacturing lens

While there are many views to explore, let us start with the Chicago’s Purchasing Managers Index.

Let us ignore the details for a moment, but the general idea is that the nice people at the Institute for Supply Management call the manufacturers in the Chicago area and ask them how things are going. If businesses are selling more and business is improving, the index goes up, if businesses are selling less, the index goes down, and if everything is the same, the index stays at 50. As Chart 1 demonstrates, we have not seen a measure this high since 1973.

While we should always caution ourselves from drawing conclusions from one perspective, it is fair to say that producers are clearly experiencing increased manufacturing activity. This is clearly logical given the COVID-19 shutdown, but the magnitude is at least worth acknowledging.

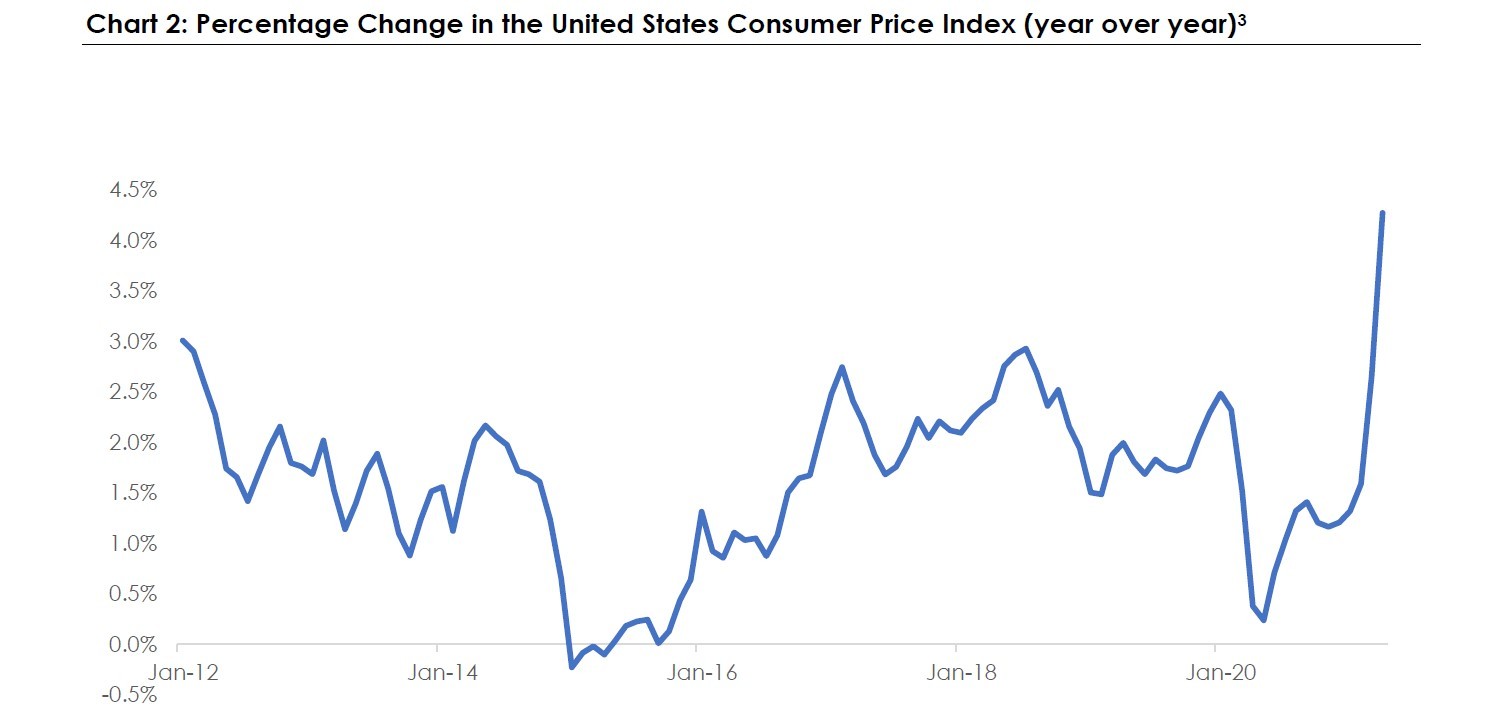

Consumers under the price microscope

For our next perspective, let us explore what consumers are experiencing. As a reminder, the U.S. consumer accounts for roughly two-thirds of the U.S. economy … said another way, the U.S. consumer matters. Again, there are many ways to view this data, but the chart below simply looks at the percentage change in something called the Consumer Price Index. Setting aside the (substantial) details, the index roughly represents a large basket of goods (homes, cars, food, etc.) that consumers purchase, and every quarter calculates the prices of those goods. Over time, we can therefore see if those prices are increasing (inflation) or decreasing (deflation).

This chart represents those changes over the past 10 years, and clearly demonstrates a very material spike in the recent numbers. Again, given the COVID-19 shutdown, the increases are not surprising, and we are clearly witnessing those changes happening in many different places (lumber, housing, cars, etc.) but, again, the magnitude is worth noticing and watching closely.

This leads us to three primary questions as investors:

- What is causing these increases?

- Why do we care?

- What would we do about it if we wanted to address it in our portfolios?

On the first question, ask five economists and you will get 10 different opinions (I am reminded of the quip that economics was invented to make astrology look respectable). Yet, there seems to be consensus that the primary explanations are:

- Pent-up demand following the COVID-19 shutdown.

- Something called base effects (essentially older low values rolling off).

- A massive increase in the supply of dollars.

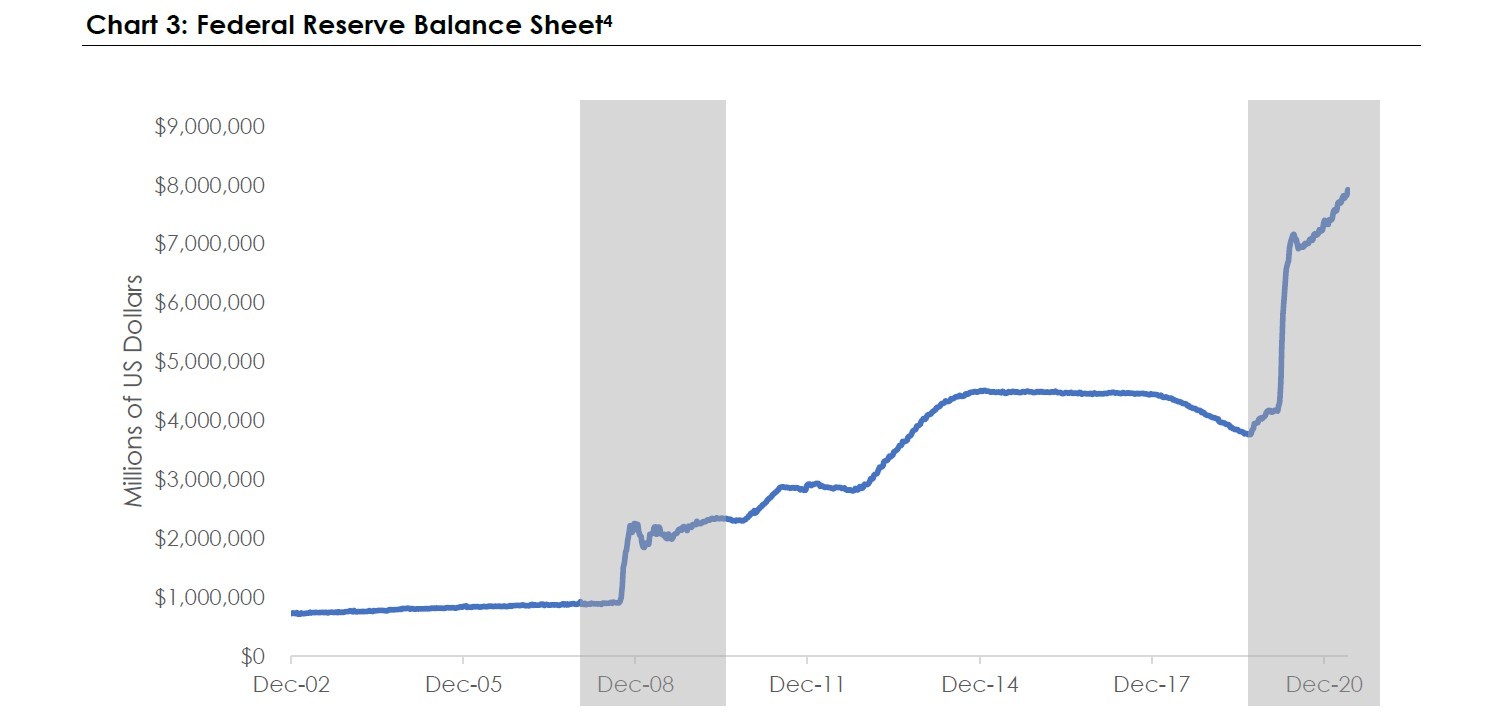

While there are many different exhibits to demonstrate the money supply dynamic, I turn to Chart 3 as the primary exhibit.

* shaded gray region denotes recession

First, let’s clarify the scale as the size is somewhat hard to fathom: $1,000,000 in millions of dollars is $1 trillion dollars. So, following the recession after the dot-com burst (not shown on chart), there was very little balance sheet to speak of. Following the Global Financial Crisis, the Federal Reserve bought massive amounts of assets to encourage risk taking again, and the balance sheet swelled to $2 trillion, and then drifted to $5 trillion just a few years later. During the COVID-19 pandemic, the balance sheet then jumped another $4 trillion to end up at nearly $8 trillion. Considering the entire U.S. economy is $21 trillion, this was a massive expansion, and with unknown consequences (because this entire toolbox is a newly created set of tools).5

Okay, okay, you say, prices are going up, manufacturers are doing well, and the government printed a ton of money…so what?

Well, let me set the stage. What are the two primary assets in U.S. investors’ portfolios? U.S. stocks and U.S. bonds. Of course, the details vary but, generally speaking, those two assets (in their many forms) make up the vast majority of portfolios. Some hold the Standard & Poor’s (S&P) 500, some hold individual stocks, some hold U.S. government bonds, and some hold corporate bonds, but blur your eyes … and many portfolios hold a good deal of instruments that rhyme with those assets.

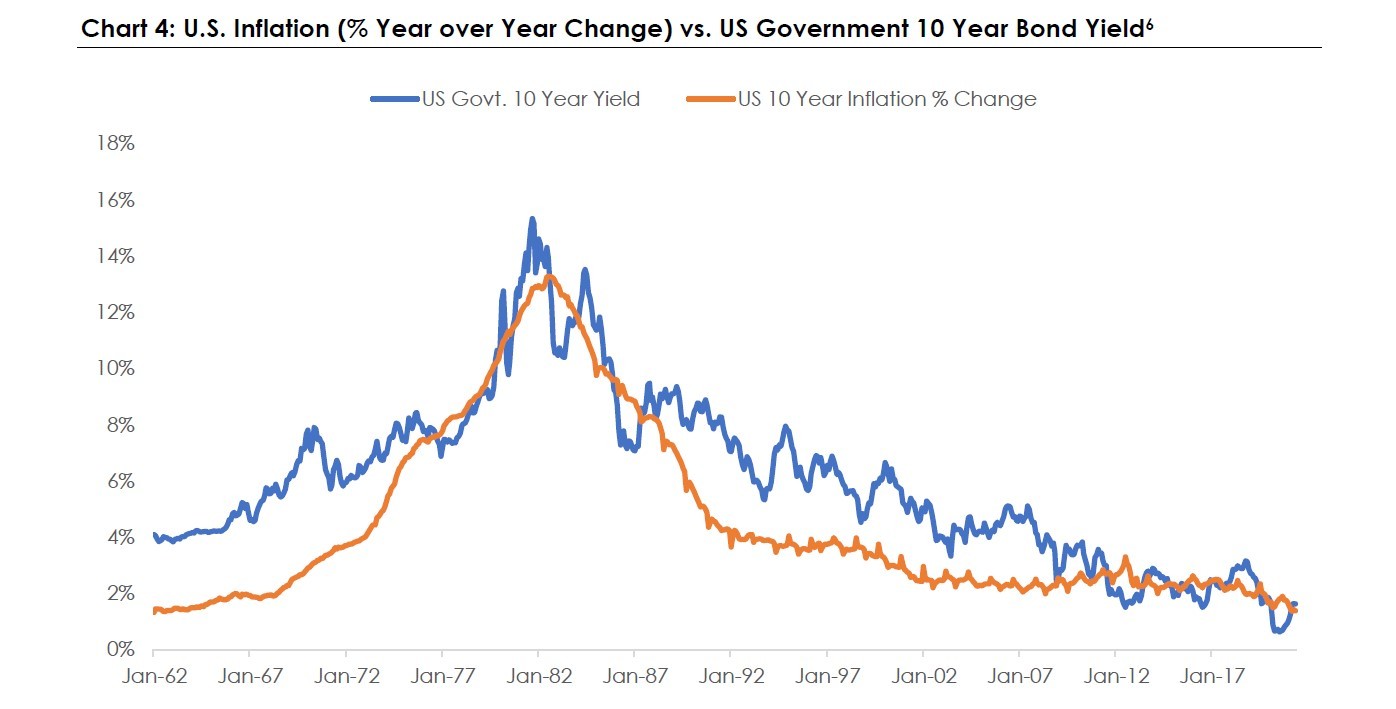

This then brings us to Chart 4.

The blue line represents the yield on U.S. Government 10-Year Treasury Bonds, and the orange line represents the rolling 10-year change in U.S. inflation (a longer version of Chart 2 above). The chart goes back to 1962 and tells three stories.

- First, in the first 20 years, bond yields went up (and because bonds move inversely to yields, bonds went down).

- Second, in the next 40 years, bond yields went down (and bond prices went up)—very consistently in fact.

- Third, and most important, over this time period, as went inflation, so did bond yields. If inflation went up, bond yields moved up, and if inflation moved down, bond yields moved down. This is logical as investors wouldn’t want to receive less than inflation for a fairly low risk bond. If inflation is 5 percent, and a bond pays 3 percent (so an investor is guaranteed to lose money), very few investors will buy the bond. Thus, the investor demands a higher yield, and the bond will fall to adjust to the desired yield.

In summary, therefore, inflation is beginning to increase for several reasons, and inflation (at least in part) drives a very important component of many portfolios.

To be clear, I do not believe we will see hyper-inflation anytime soon. I also do not believe the monetary or fiscal response to the recent recession and pandemic has been irresponsible, nor do I believe we will see anything resembling the hyper-inflation examples mentioned earlier. Further, the U.S. Federal Reserve has several very important (although somewhat crude) tools at its disposal to prevent runaway inflation. Quite simply, it can discourage spending, and encourage saving, by changing rates should inflation increase. While the Fed’s language is currently quite against that stance, it has historically shown a willingness to do so (e.g., Paul Volcker, Fed chairman in 1980), and I have no reason to believe it has structurally lost that resolve.

What should investors do?

This then brings us to the conclusion. What, if anything, as investors should we do?

- First and foremost, awareness is key. Inflation is likely to increase throughout the year (and perhaps further), and bonds are likely to at least be less of a stalwart than they have over the past 40 years. It is important to realize that is possible and we should all be prepared for lower near-term performance in fixed income markets.

- Second, diversification is key. Equities, for example, have historically been a reasonable asset during certain inflationary periods as companies can often pass through increased costs.

- Third, now is a good time to explore other forms of inflation protection, as well as a broader diversification of fixed income instruments.

Last, and perhaps most important, remember that markets cannot be timed. While I do believe this is very worth being aware of, I am also very confident that, over the long term, the best portfolio is one that is well built, monitored closely, diversified, and limits turnover, taxes, and expenses.

Discover more from MassMutual …

Financial protection tactics as you near retirement

Understanding the basics of investing

Market analysis from Daken Vanderburg

________________________________

1 Derived from Adam Grant’s excellent book “Think Again,” p. 40

2 Sources: Bloomberg, https://www.ism-chicago.org/insidepages/reportsonbusiness/

3 Sources: US Bureau of Labor Statistics; https://www.bls.gov/cpi/

4 Sources: St. Louis Federal Reserve, https://fred.stlouisfed.org/series/WALCL

5 Source: Bureau of Economic Analysis, https://www.bea.gov/index.php/

6 Source: Bloomberg, U.S. Treasury, U.S. Bureau of Labor Statistics