I once heard the story about how Warren Buffet and Bill Gates met. Both are known to be a bit reclusive, intolerant of wasting time, wildly curious, and avid bridge players. As such, people in their circles had long thought they should get together.

And so, with some hesitancy, both men agreed.

As the story goes, the dinner (which Bill Gates’ mother hosted) went phenomenally well. The pair became fast friends and remain close to this day.

What I find fascinating is what happened at dinner. Apparently, while discussing their lives and proclivities, Bill Gates’ father asked them to think for a moment and reply with a single word to describe why they had been so successful. Interestingly, both Warren and Bill landed on the same word: “focus.”

With all due respect to Messrs Gates and Buffett, today we are going to reject that advice, and go wide, instead of deep. From time to time, we like to share the “charts we’re watching” to help provide perspective.

Groundhog Day Part Deux

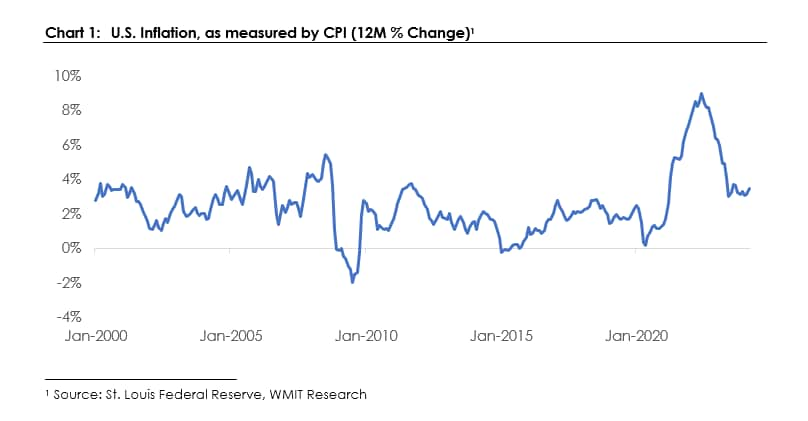

If I had to choose a single word to describe the economic disruption we’ve experienced the last two years it would be “inflation.” We (I’m looking at you, Federal Reserve) laid the groundwork for inflation, we then propagated inflation, quickly reversed course, and now have tried to bring inflation back down. While previous market updates explored each of those phases ad nauseum…if one thing is clear it is that the inflation caused confusion and uncertainty, rankled markets, and has now remained (unsurprisingly) high despite Fed efforts. Which brings us to Chart 1.

For decades prior, we experienced inflation that mostly bounced between 0 percent and 4 percent, and then suddenly jumped over 8 percent (and higher in many other countries). Yes, pent-up demand contributed, and yes, supply chains disruptions contributed…but the dominant cause in our opinion was the remarkable increase in money.

As the chart above shows, inflation has fallen, and has (thankfully) fallen relatively quickly. And yet it’s now paused, much to the market’s chagrin, as the market realizes that the Federal Reserve will not cut rates as aggressively as previously hoped.

The risk, of course, is that inflation doesn’t stay here, but instead reverses course, and either moves back higher as growth picks back up or, perhaps more frighteningly, increases WHILE growth stalls further (what is referred to as stagflation). As such, that brings us to Chart 2.

Chart 2 provides a fairly clear and comprehensive depiction of the remarkable increase in money supply in 2021; which was then followed by an even more remarkable contraction of money supply.

If this is confusing (and yes, it is), let’s imagine a simple model. There’s a country where nothing changes, except for money. Citizens are still working, schools are still teaching, and everyone is doing basically what they did the day before. And, this country uses paper money to transact everything they buy or sell.

Clear so far?

Now, imagine all the money for that country sitting on a large table. And literally all that happens is that the folks that can print more money do, indeed, print more money. They actually print around 40 percent more money, and then they just dump it on the table on top of the existing money. What happens? Remember, economic output is exactly the same. Well, all things being equal, that money is just worth less….about 40 percent less in fact. So, all goods that were purchased for 1 unit of money are now purchased for 1.4 units of money.

Zoom out, and that’s basically what happened in the United States. Houses are priced in dollars, and the value of those dollars went down. Ergo, the perceived price of houses went up. Groceries are priced in dollars, and the perceived price of those groceries also went up, not because of some mysterious forces…but because the dollars that we own are literally WORTH LESS. That’s inflation, dear readers, and at least in this very specific version of something called monetary inflation, we created inflation by creating more dollars….which should explain why we’re watching the supply of money about as closely as we can, and collectively kneeling by our beds at night to ask the Treasury to stay away from the printing press.

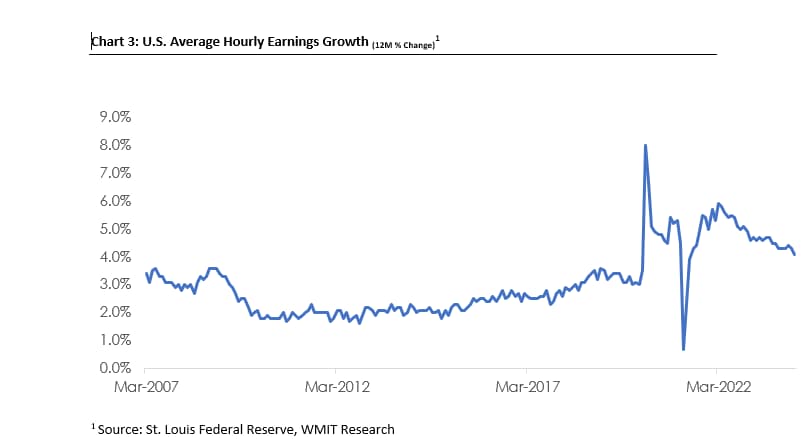

But wait, you say! What about jobs! Ahh…yes…that brings us to Chart 3.

Let’s imagine you just graduated college, go out and get a job, and you make $100 per day. Nice work – feels good, right?! What do you do? Well, you do what most people do, you spend (and hopefully save) the money you earn. You rent an apartment, get your first car, get an occasional dinner out, and generally go about your life. Great — straightforward so far.

Now, let’s imagine a year goes by, and you now receive $105 per day. Ahh, life is good. What happens? Well, for most humans, they now buy more. Usually about 5 percent more, in fact.

Therefore, what happens? Well, by and large, if wages are increasing EVERY year at around 5 percent, then by and large, consumers will purchase 5 percent more goods. If prices were to stay the same as the year before then the quantity of goods would (helpfully) be 5 percent higher, but that’s not generally how it works because this process is circular. Prices went up because the quantity of money went up. When prices went up, employees said they needed more money to pay for goods they were already buying, and so employers responded accordingly.

Ahhh…but this is where it gets interesting. The Fed says, “whoops – we went too far – let’s bring inflation back down.” BUT they don’t control wages. They control the incentives for borrowing and saving. And how many companies do you know that are going to be able to quickly LOWER wages? Right…none. Which is one of the many reasons that inflation remains sticky and has for the past 300 years. It goes up quickly and goes down slowly. Over and over again.

Okay, let’s pause for a moment and recap:

- Inflation is coming down (yay!).

- But has paused that decline (boo…).

- But wages have gone up (yay!).

- But aren’t growing as fast as they were (boo…).

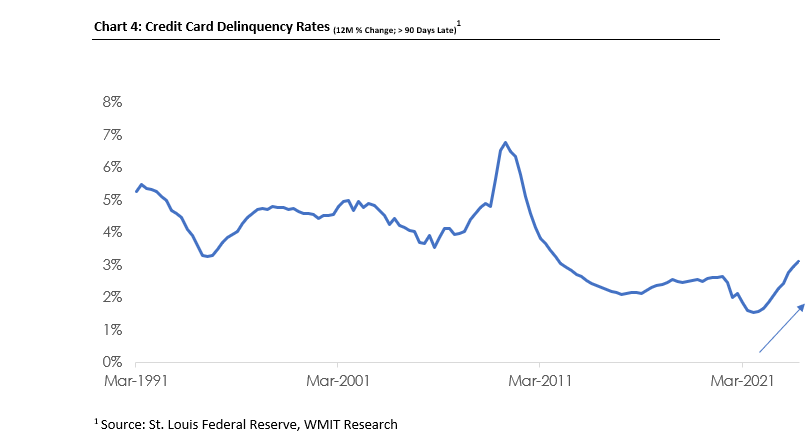

Alright – mostly good news, right? Which brings us to my most concerning (and final) chart of the day.

The chart above shows the number of people (in percentage terms) that are late on their credit card payments by more than 90 days. At even a cursory glance, we will notice the recent increase in credit card delinquencies from arguably a VERY low level to a lesser low level. That’s right my dear reader, more and more folks are behind on their credit card payments now than in early 2022 (the trough was September 2021, by the way).

Astute readers will likely ask “why?” Well, attribution is always challenging in a dynamic and multi-variate economy. My hypothesis (which we are working on confirming) is as follows:

During and following the COVID pandemic, the U.S. Government (primarily through the U.S. Treasury) printed an unprecedented amount of new currency, and quite literally deposited that money into checking accounts and mailed it to mailboxes. That resulted in, by definition, a massive increase in dollars in the ecosystem. At the same time, rates were incredibly low, so it was very easy to obtain loans at very low interest rates. It wasn’t precisely “free money,” but it was pretty close.

That resulted in, again, an unprecedented amount of excess savings for the U.S. consumer. By our accounts, something like $2 trillion dollars of excess savings, in fact.

And this is where it gets interesting, folks.

The Federal Reserve then observes a massive spike in inflation, quickly reverses course, raises rates and….wait for it…nothing happened. No recession, the economy still expanded, wages still rose (see Chart 3).

Why didn’t the economy collapse, you ask?

Well, because no one cared that the Fed raised rates. Credit card payments went up and consumers just paid a slightly higher payment (because they had excess savings). Car payments went up, and consumers just paid a slightly higher payment (because they had excess savings). House payments went up (for those with variable or new mortgages), and borrowers just paid more.

BUT! And here’s the big "aha!" All that excess savings is gone. Yes, that’s right — all $2 trillion has been spent, and this is when it starts to matter.

So, yes, ladies and gentlemen delinquencies are on the rise, and we are therefore watching closely. Does this mean calamity is nigh? Of course not. Does this mean a recession is almost here? Unlikely.

It does however mean that risk is on the horizon, and it is our job to try and understand those risks and position ourselves accordingly. It is also worth noting that you can choose any single day in the history of our country (post industrial revolution), and I would be able to find similar risks on the horizon. It is, I believe, a necessary characteristic of the human condition. Memories are short, incentives are strong, and the pendulum will always swing.

Discover more from MassMutual…

When markets dive, keep your strategic calm

Is your retirement portfolio inflation ready?

Need a financial professional? Find one here

_______________________________________

1 Source: St. Louis Federal Reserve, WMIT Research