Before examining what’s happening in the markets lately, including bond surges and equity stumbles, it might be useful to consider perspective.

The story of Rubin “Hurricane” Carter can help with that. The professional boxer was falsely accused of murder and sent to prison. But he never accepted the role of prisoner, refusing all the accoutrements and routines associated with it. He made the decision that perspective mattered as much as innocence, and perspective was something HE could control. That perspective was vital in enabling Carter to survive his injustice.

Beyond handling tough situations, perspective can also be used to make better decisions and, if done well, create better outcomes (including in the investment world).

Consider this simple example: If someone told you that there were 57 unprovoked shark attacks in the United States in 2022, your reaction may be to spend a bit less time in the water.

And yet, a more helpful perspective might be that five people are killed by sharks each year (on average) worldwide. It would likely be helpful to know that even among the subset of people who go to beaches, a person's chance of being attacked by a shark is 1 in 11.5 million, and a person's chance of getting killed by a shark is less than 1 in 264.1 million.1 Or, further, that it is significantly more likely that a person can die from dog attack, wasp sting, or snake bite.

Perhaps even more reassuring to those who like to swim in the ocean is that there have been more people killed while taking a selfie than from shark attacks (between 2011 and 2017, selfies accounted for 259 deaths while sharks killed 50 people worldwide during the same period).2

In short, perspective matters. What follows is an analysis of how it can affect our investing behavior starting with current market conditions.

With that, let us begin…

Perspective on value and news

Stock markets have gone up, bond markets have gone down, and the economy (U.S. at least) continues chugging along. Inflation was high, then it fell, but it remains stubbornly stuck. Money supply was remarkable, then it contracted, and now continues to shrink. The Federal Reserve provided lots of liquidity, then less so, and then it raised rates very quickly and is now trying to take away liquidity. The consumer spent like crazy, then less so but, despite everything being more expensive…continues to spend. Hmmm….

Confused yet?

One way to remove the noise from the conversation is simply to see what markets are telling us. If, for example, I buy a bond that is yielding 5 percent, I understand that, assuming the bond issuer continues to pay me back, I will receive a return of 5 percent.

What if I buy a stock? Well, we can essentially perform a similar level of analysis. If, for example, a stock earns $5 for each of its shareholders each year, and the stock is currently priced at $100, then, well, it similarly pays 5 percent (earnings divided by price = earnings yield). This basic transformation essentially allows us to compare bonds and stocks…at least with a simplistic view…to get a better sense of what is and isn’t expensive.

Which brings us to Chart 1.

Indexes are unmanaged, you cannot invest directly in an index. Returns assume the reinvestment of dividends and income. Past Performance does not guarantee future returns.

The blue line is the earnings yield for the Standard & Poor’s 500, the light gray is the yield on the U.S. Government two-year bond, and the dark gray line is the yield on the U.S. Government 10-year bond.

Between 2011 and 2021 or so, the stock market (at least from this view) clearly had a higher earnings yield. Buying the S&P 500 during the middle of 2016, for example, was likely to yield a bit more than 5 percent, while bonds were a bit more than 2 percent.

And now? Well, they’re all around the same. As bonds have fallen (and yields have risen), stocks have risen (and therefore yields have fallen)…which means, well, at least from this one simplistic view…they are all a similar level of yield.

While I believe this to be a useful input…it is worth noting several risks and considerations:

- Historically, equities have had a much higher volatility than longer-dated bonds, and longer-dated bonds have had higher volatility than short-dated bonds. Said another way, all yields are not created equal.

- Should an investor purchase short-dated bonds, the reinvestment risk is very important. Said another way, yes, a two-year bond is yielding around 5 percent, but what happens in two years when the money is returned? If rates are much lower at that , the investor clearly would have been better off purchasing longer dated bonds.

This, perhaps, belies the idea that there are truly no absolute decisions in investing…there are only tradeoffs.

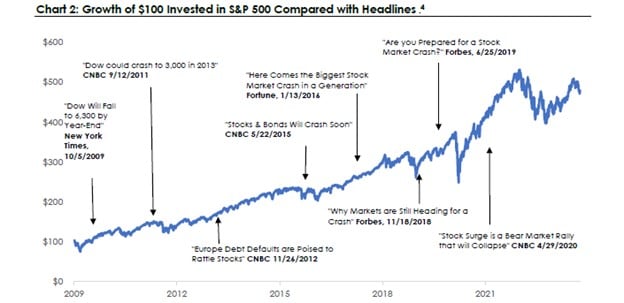

Unfortunately, what we hear daily often runs counter to that idea, which brings me to Chart 2.

Hypothetical example used for illustrative purposes only. Indexes are unmanaged, you cannot invest directly in an index. Returns assume the reinvestment of dividends and income. Past Performance does not guarantee future returns.

Tuning out the noise

Chart 2 shows two things. The first is the growth of $100 invested in the S&P 500 (including dividends) since Jan. 1, 2009. The second is, perhaps, more interesting. I then overlay headlines from various publications that predicted various doomsday events such as “markets are heading for a crash,” or “stocks and bonds will crash soon,” and the like.

The point here, again, is perspective. As we’ve established in prior updates, “bad news sells” because our brains react to negative news much more strongly than to positive news. If a person stopping at a newsstand sees two newspapers and one exclaims, “the world is ending,” while the other calmly states, “things are great, please continue on your day,” which newspaper are they likely to pick up?

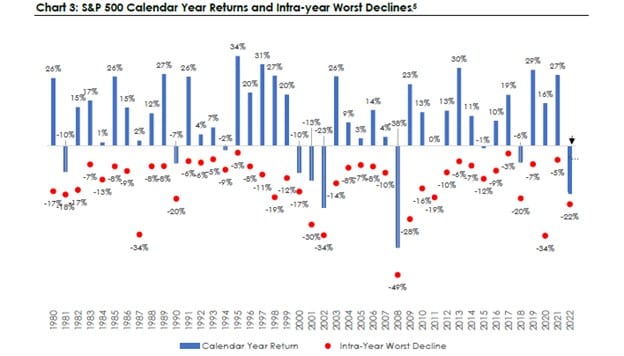

And yet…despite those horrific headlines…and despite the scaremongering…the S&P continued to march upward. Was this a particularly strong time period? Yes, absolutely. Are there many more time periods like this? Also, yes, absolutely. But wait, my astute readers will say, stocks also go down, don’t they? And yes, that is precisely the point, which leads to Chart 3.

Indexes are unmanaged, you cannot invest directly in an index. Returns assume the reinvestment of dividends and income. Past Performance does not guarantee future returns.

Chart 3 has two pieces of information:

- The red dots show the worst selloffs in each year. So, in 1980, the market was down 17 percent at one point; in 1981, the market was down 18 percent at some point, and the like.

- The blue bars include the red dots but show the FULL calendar year returns for each year. So, while the market was down at one point in 1980, for the full calendar year (Jan. 1 — Dec. 31), the market was up 26 percent.

Zoom out and there are two obvious conclusions:

- The stock market goes down nearly every single year.

- In aggregate, and on average, the market has generally been a very good investment (the average year over this period was up more than 10 percent).

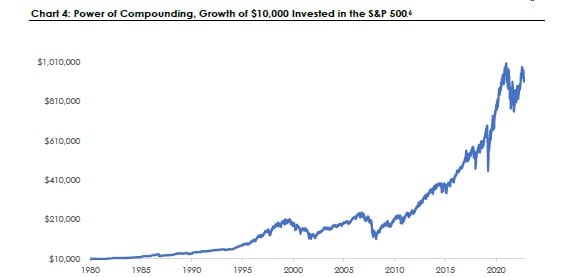

If you then combine all that information, we have Chart 4, perhaps our most profound (and simplest) chart for today.

Hypothetical example used for illustrative purposes only. Indexes are unmanaged, you cannot invest directly in an index. Returns assume the reinvestment of dividends and income. Past Performance does not guarantee future returns.

The power of compounding

If you had begun with $10,000 in the market in 1980 and remained invested (while re-investing dividends)7, there would be a bit over $928,000. This is the power of compounding and ignoring the short-term noise and headlines. The Volcker shock of 1980, the crash of 1987, the dot-com bubble, the global financial crisis, COVID-19, poor policy and monetary decisions…all of those items, which were terrifying at the time, have since blended into the background with the power of compounding.

Said another way, perspective changes everything.

We remain at your service and watching closely. Please let us or your financial professional know how we can serve you.

Discover more from MassMutual…

3 ways to consider market volatility

When markets dive, keep your strategic calm

Need a financial professional? Find one here

________________________________________

1 https://www.floridamuseum.ufl.edu/shark-attacks/odds/compare-risk/lightning-strikes/

2 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6131996/

3 Source: St. Louis Federal Reserve (FRED), WMIT Research

4 Source: Bloomberg, WMIT Research

5 Source: Bloomberg, WMIT Research

6 Source: Bloomberg, WMIT Research

7 Bloomberg, WMIT Research