Rattled yet? Yes, most investors are … and with understandable logic: Equity markets continue to swing wildly, even after dramatic intervention by the Federal Reserve. Yet this is how markets behave when uncertainty and fear dominate.

As we have stated from the beginning of this crisis, we are not epidemiologists, and we have no view as to how this crisis will proceed from a health perspective. Yet we do understand markets, particularly markets during periods of fear and high levels of uncertainty. As such, below, we try to offer a couple of lenses through which to view the recent turmoil, while attempting to set expectations for how markets will likely continue to behave.

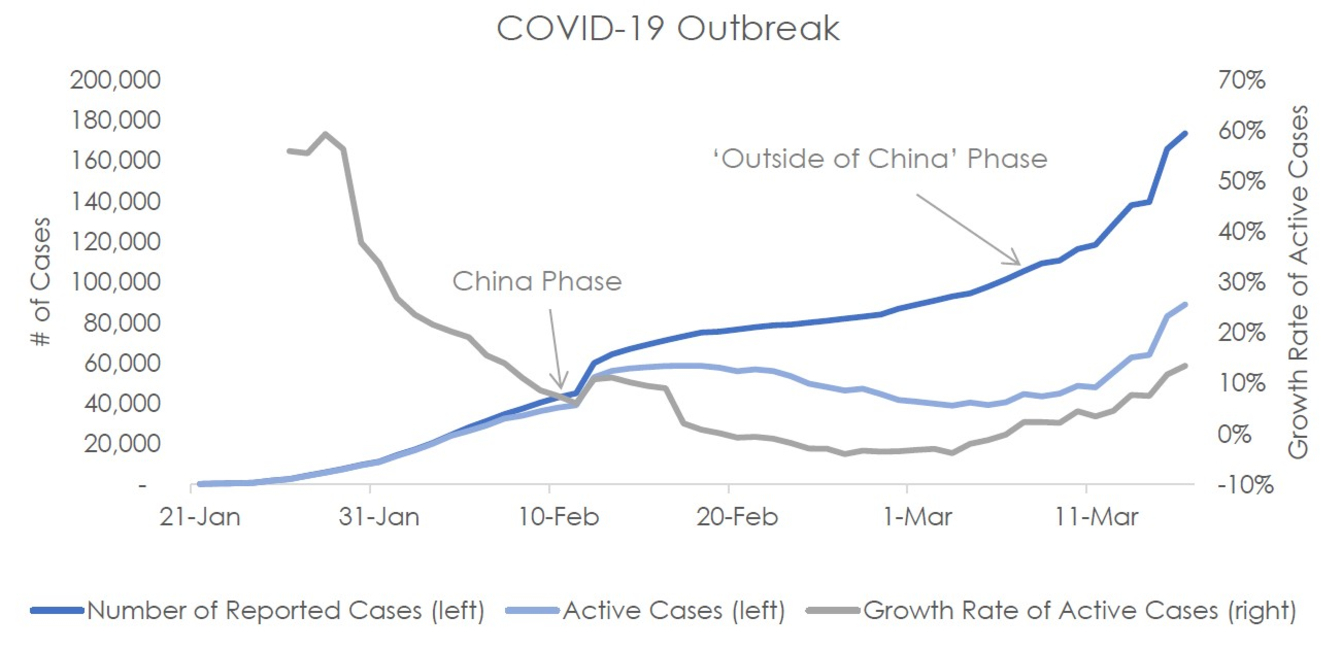

First, let’s begin with a quick update on the nature of the crisis. As of March 16:

1) The novel coronavirus (COVID-19), now present on every continent except Antarctica, has infected nearly 175,000 people and killed more than 6,600 people .

2) There are now more cases outside of China than inside China.

3) In the United States, there are more than 3,800 cases along with 68 deaths , and the number of cases is growing at roughly 30 percent per day (which means we should expect a doubling of cases in a bit less than every three days).

Yes, this is still vastly fewer than the total number of cases from the common flu every year. The World Health Organization estimates 45 million people were infected worldwide with somewhere between 300,000 and 550,000 deaths in the 2018 flu season. But left unchecked, the math is indicating this is likely to get much worse.

As our first chart demonstrates, we have now moved into a new phase of the COVID-19 outbreak. China is no longer the primary location of new cases and has managed the outbreak well enough to begin experiencing a negative growth rate of new cases. For those countries now experiencing the early stages of the outbreak, they are scrambling (with varying degrees of success) to mitigate the damage.

Sources: Bloomberg, World Health Organization

Accordingly, investors worldwide are nervous. Questions abound, and therefore, so does volatility. When will this end? How will this end? How much will economies contract? What will governments do and what will their citizens do?

The short answer is that no one knows the answers to these questions, and therefore, the world speculates and uncertainty dominates. Experts are marched out, assumptions are made, frameworks are created, models are generated … and thoughtful observers are left scratching their heads at the range of answers (some more credible than others).

During times like these, therefore, it is helpful to pause, breathe, and take stock of what we do know.

Here are three perspectives we believe are useful to remember:

1) Volatility begets volatility.

2) Equity markets are beginning to look increasingly attractive (relative to bonds).

Let’s take a closer look at the data and consequences involved in each one of those perspectives.

Volatility begets volatility

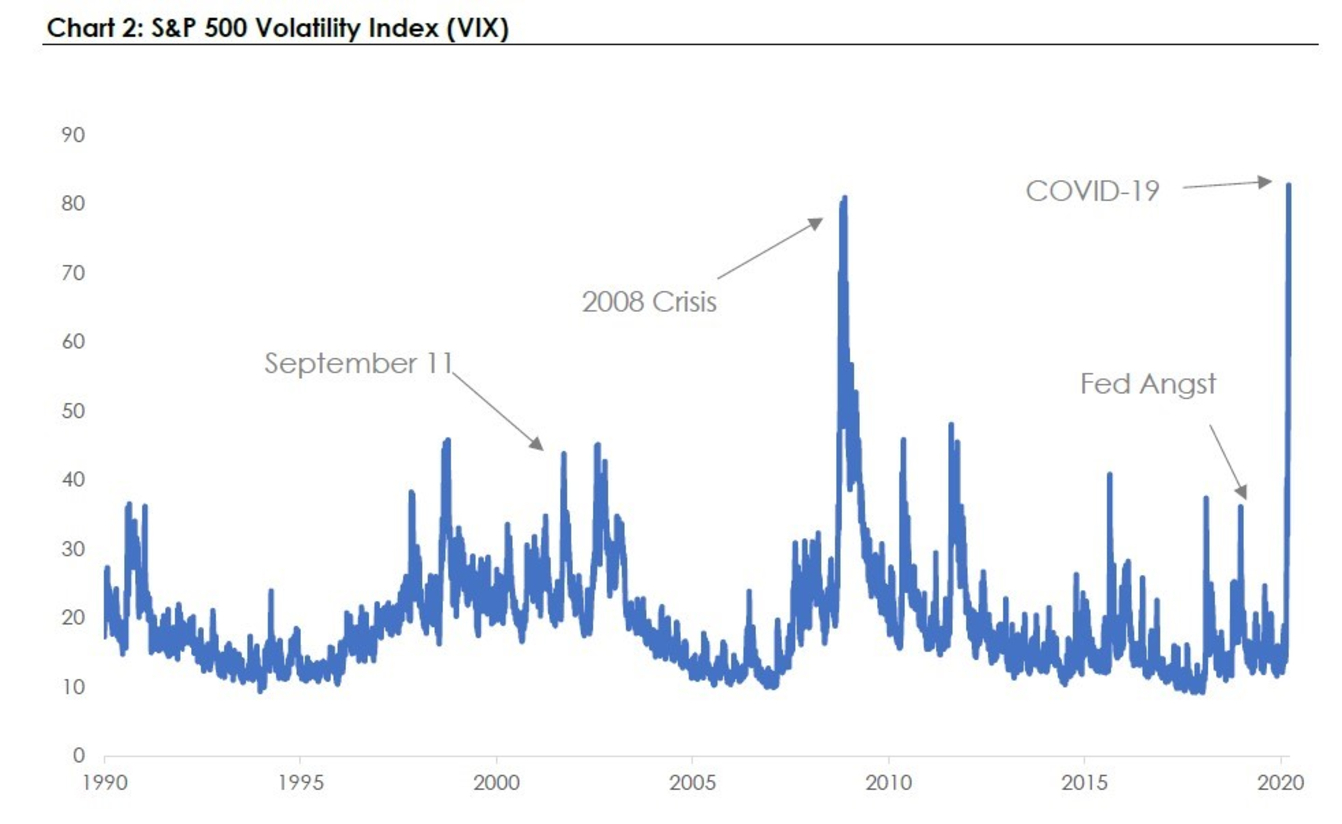

First and foremost, we believe the current volatility is likely to continue. Chart 2 shows how high one measure of volatility currently is when viewed relative to history.

Sources: Bloomberg, CBOE

The precise definition of the index doesn’t matter, but it roughly reflects the markets’ expectation of forward volatility.1 Said another way, this index doesn’t tell us which direction the market will go, but it is telling us that it is likely to be a turbulent ride.

So, while we can take many things from this perspective, one clear signal is that we should not be focused on the noise of the moment to moment. It will be fast, and furious, and in the moment … very hard to understand.

Perhaps more usefully, if you bear with a small bit of math, this index is essentially telling us that we should have daily market moves between -5 percent and +5 percent around two-thirds of the time, and we should have daily market moves between -10 percent and +10 percent around 95 percent of the time. Given the last couple of days, that math seems roughly right.

As such, my primary takeaway is that investors should not make decisions based on what happened today. Or yesterday. Or since Saturday. As tempting as that is, we, as cautious, thoughtful participants and stewards must zoom out. We must make decisions based on what capital markets provide over decades, not over the past several hours.

Increasingly attractive?

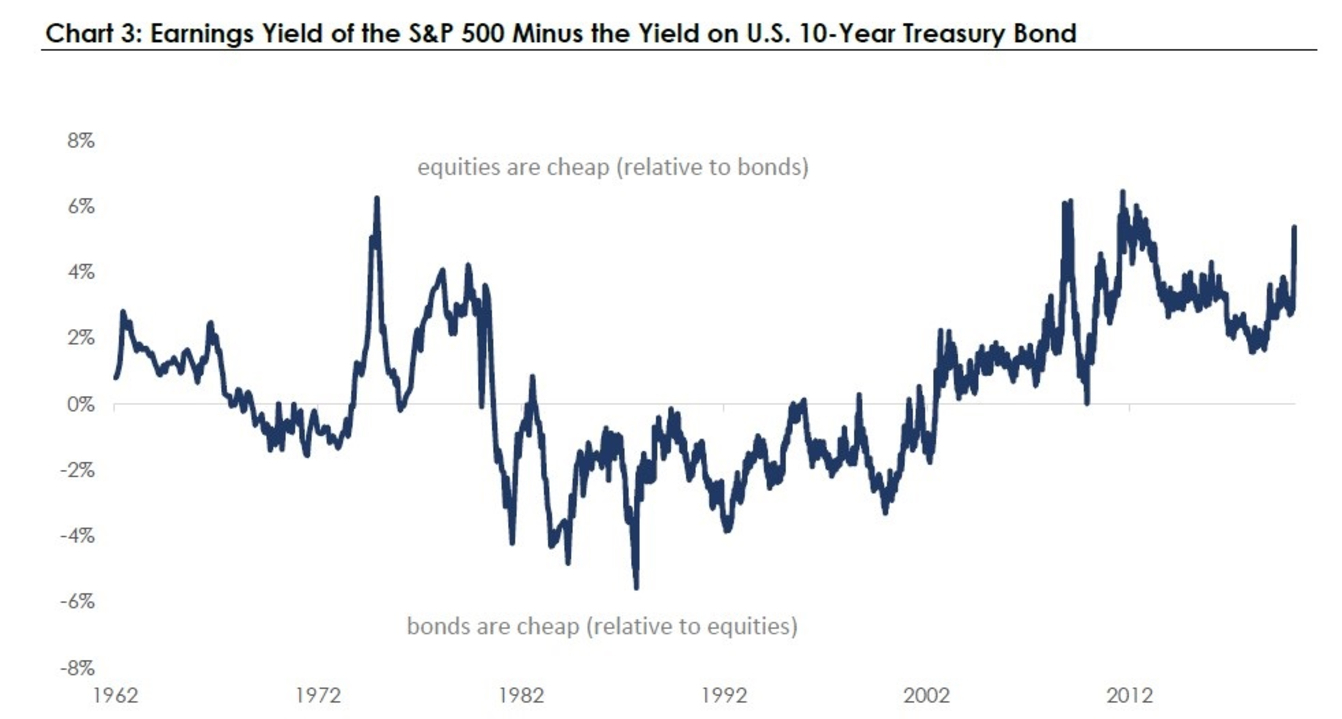

Second, let’s now turn to the perspective of valuations. One wonderful aspect of investment markets is that as they sell off, they become more attractive. Yes, I know it is obvious, but is often forgotten during times like these. As such, let’s compare the two markets most heavily utilized in client portfolios: the Standard & Poor’s (S&P) 500 and the U.S. bond market.2

Source: Bloomberg

Toward the bottom of the chart means that bonds are relatively cheap when compared with equities, and the top of the chart means that equities are relatively cheap when compared with bonds. As of March 16, for example, the S&P has an earnings yield of around 6 percent, and the 10-Year Treasury has a yield of around .74 percent, creating a “spread” of around 5.25 percent.

To be clear, this doesn’t mean that we are guaranteed to earn either of those return expectations, but it does give a rough sense of the relative prices and can indicate a proxy for value (among many other things).

At a minimum, this tells me it may not a great time to be selling out of equities and buying into bonds.

Focus on the long term

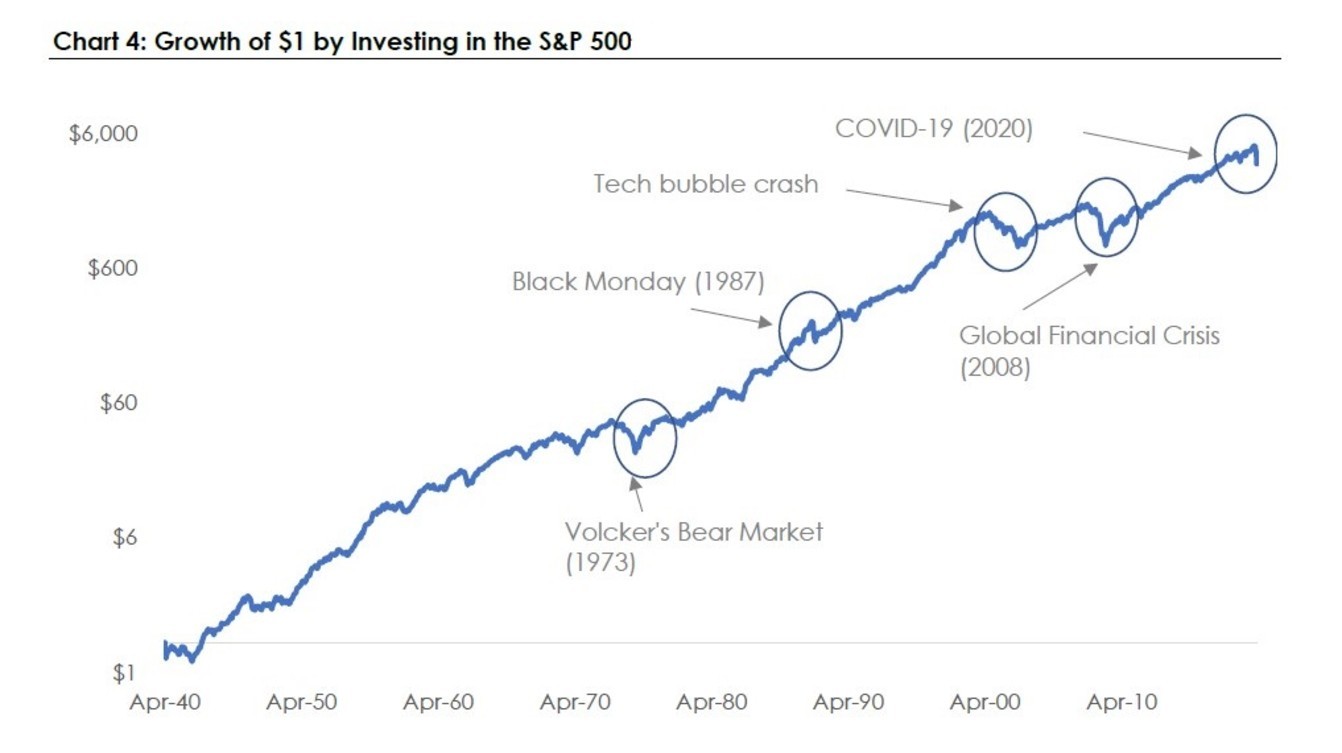

Third, let us zoom out to the chart that offers perhaps the most important lens of all. Chart 4 shows us the total returns of investing in the S&P 500 since 1940.

Source: Bloomberg

This chart demonstrates one of the most wonderful aspects of investing: markets recover. Black Monday in October 1987 was an unprecedented event as the U.S. stock markets fell almost 22 percent in a single day. The tech bubble crash of 1999/2000 was a remarkable destruction of value, and amid the Global Financial Crisis of 2008, pundits and commentators were speculating as to whether we had seen the end of capitalism as we had known it.

And yet, if we zoom out over the long term, equity markets are a remarkable provider of investment returns. This is the lens through which we should make our allocation decisions. During the darkest moments, we should remember why we made those decisions … and adhere to the plans created in those periods of less turmoil.

I do not know how much damage will be tallied when this is over, but I do know that capitalism creates incentives for investment and, over the long term, rewards those who can tolerate the short-term volatility.

In closing, stay safe, stay focused on what you can control, and please turn off the investment news channels.

For individual guidance and advice, contact your financial professional. Don't have one? Find one here .

1 The Volatility Index, or VIX, is a real-time market index that represents the market's expectation of 30-day forward-looking volatility. Derived from the price inputs of the S&P 500 index options, it provides a measure of market risk and investors' sentiments.

2 The S&P 500 is an equity index that consists of the stocks of 500 large U.S. companies measured by market capitalization. The results here include the effect of reinvested dividends. You cannot invest directly in an index.