Just after 5 a.m. Eastern European time (GMT + 2), Ukraine’s government reported it was facing a “full-scale attack from multiple directions.” We also have learned of many explosions across the country, confirmation of downed Russian aircraft, and mass migrations from Kyiv, the Ukrainian capital.

While the attack had been telegraphed by Russian leadership over the past several weeks, it is still hard to deny this is likely the most significant military engagement in Europe since the end of World War II. As such, today’s market update will be both concise and focused, and will largely address one primary question: “what, as investors, are we to do?”

To answer that question, let us consider the situation through three lenses:

- History

- Timing

- Perspective

History

Before my dear reader begins an eye-roll at the mention of a history lesson, let me try to narrow the scope.

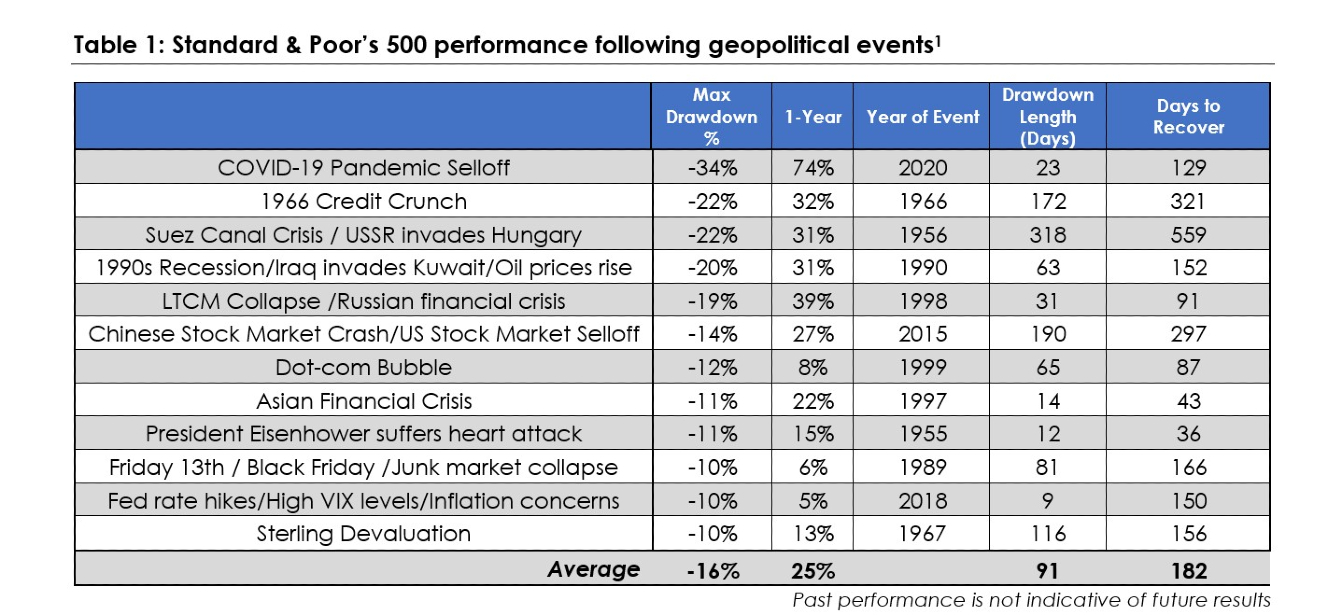

We, as a country, and more specifically as an economy, have experienced pandemics, wars, supply shortages, consumer crises, supply shocks, and many more events over the past several hundred years. As Table 1 reminds us, there have been, in fact, no shortages of trials and tribulations for us collectively to navigate.

Each time, regardless of the severity, the event was resolved, the market recovered, and capital markets continued to generate long-term returns in excess of inflation.

Is the Russian escalation different? Well, yes, of course it is. But so were the World Trade Center bombing in 1993, the Cuban Missile Crisis, and the assasination of President John F. Kennedy. Each event had rampant speculation, analysis, and predictions, and yet, on average, markets found a way to recover.

Timing

Which then brings us to the obvious question of “what if I’m certain?” Said another way, history is littered with examples of individuals who are “certain” of the outcome. Perhaps we understand the Russia-Ukraine conflict better than others, or perhaps we are the world’s foremost expert on Russia’s President Vladimir Putin, or perhaps we just contain a (seemingly frequent) penchant for over-confidence.

The problem is 1) we need to be right, and 2) our timing needs to be perfect.

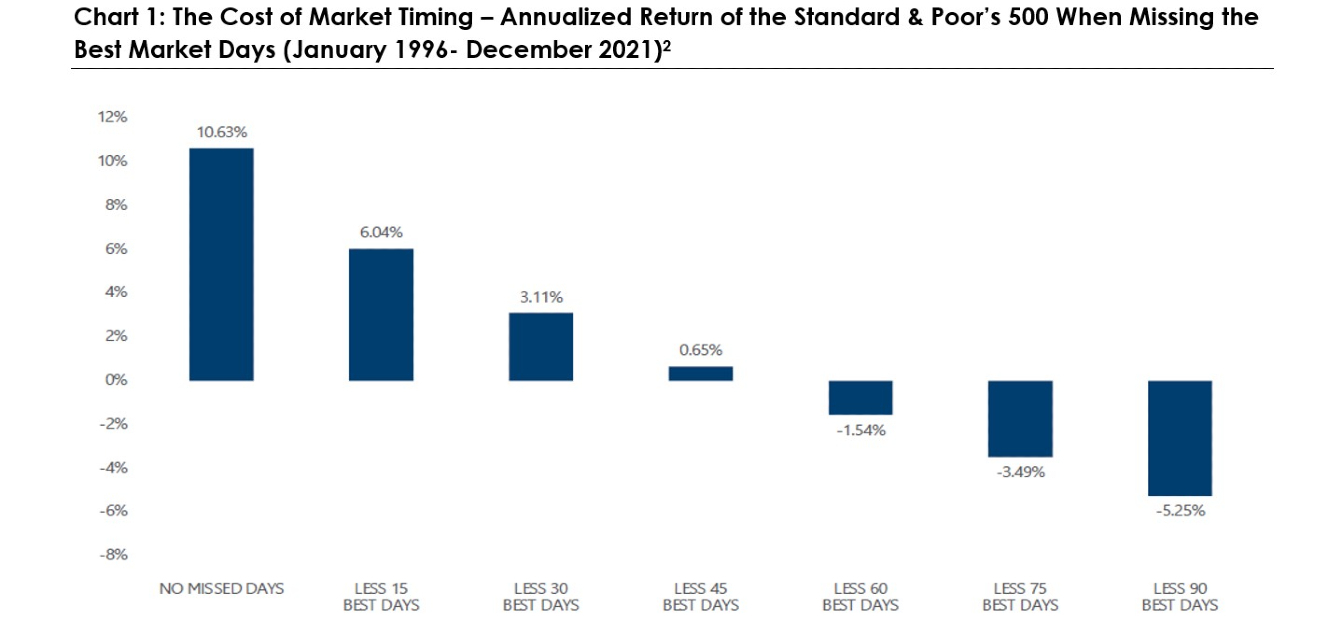

Chart 1, one of my favorites, essentially shows this dynamic.

Let me explain. Chart 1 shows the annualized return from 1996 through 2021 when missing the best market days. To make this clearer, over this time period, the Standard & Poor’s 500 returned 10.63 percent if an investor were to remain fully invested for the entire time period. Yet if the investor missed the 15 best days over the ENTIRE 25-year period, the return dropped to 6.04 percent. That’s the equivalent of missing just one day every 1.6 years. If that investor were to miss the best 30 days (or a little bit more than one day per year), then the return drops to 3.1 percent.

While interesting and fairly staggering, to me, the important question is why?

When markets sell-off, they, by definition, become more volatile. Historically, they’ve moved down more, and they move up more. They, again, by definition, move a lot more.

Yet if we exit the markets when they are moving down a lot, then we are likely to miss those days they are also moving up a lot.

Over the past 20 years, most of the best market days occurred in 2008, 2011, and 2020, all years during which, not coincidentally, the largest crises occurred. In fact, generally speaking, the largest up moves occurred on those days following the largest down moves. This, also not coincidentally, tends to precisely the same moments when the pain is greatest for investors, and they are mostly likely to exit the markets.

All of which is to say, even if one could predict which direction markets will move, and even if one could avoid taxes and the higher fees (both generally impossible), then that person must also get the timing right …or the opportunity costs will be enormous.

Perspective

For the last section, let us take a moment and use a wider lens.

Capitalism is an imperfect system. It does, however, through capital markets, allocate resources to those companies that need it for productive purposes remarkably well.

If, for example, we provide a company our hard earned dollars, we expect it to utilize those dollars to make better products, to create a more thoughtful strategy, and in general to grow our dollars into more than what we gave it.

Generally speaking, that company is fundamentally doing the same thing today as it was yesterday, and it is important to remember the Russian invasion has not changed that dynamic.

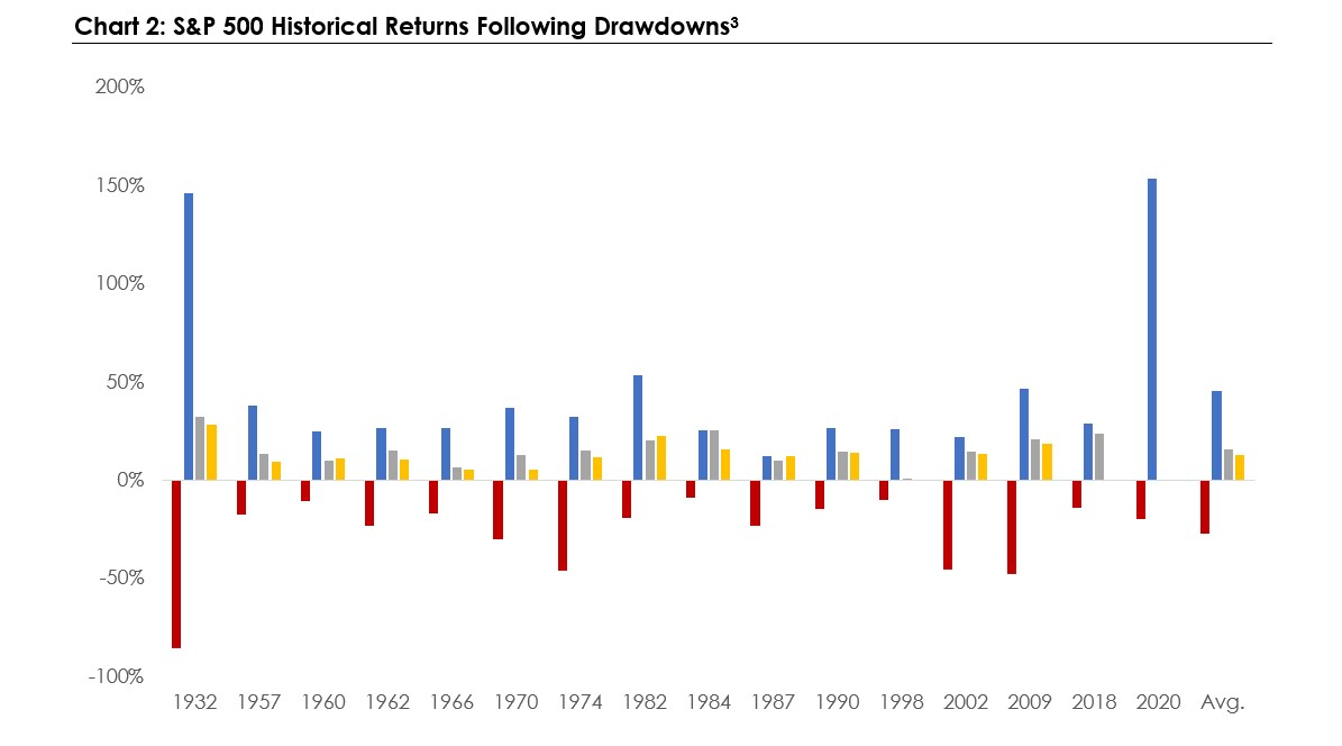

Similarly, over history, we have faced many crises before (as discussed in section 1). Yet, historically, over the long term, markets have a way of generating returns despite those many crises. While table 1 demonstrated specific geopolitical events, Chart 2 reminds us of that dynamic by simply focusing on market sell-offs regardless of the reason.

The red bars represent every loss in the S&P 500 since 1929 along with its magnitude. At the far left is 1932 when the S&P lost nearly 90 percent and at the far right is 2020 when the S&P lost a bit over 33 percent.

The blue, grey, and yellow bars show subsequent gains in the S&P 500 following those losses.

I see two important takeways:

- There wasn’t a single time period over the past 100 years that had a negative one-year, three-year, or five-year forward return (following the loss).

- Those returns for the subsequent time periods were strongly positive.

Will that happen this time? I have no idea.

Which is sort of the point. The short term is impossible to predict. Crises, pandemics, wars…those events seem to be part and parcel with the human condition.

Yet we persevere. We evolve. We learn (hopefully) from those events, and we (hopefully) try to make better decisions the next time.

Markets reflect that dynamic. Markets reflect the idea that the short term is noisy and confusing, but over the long term, incentives reward growth and ingenuity, and have done so in remarkable fashion over the past several hundred years. Try to take the short term in stride and turn your focus to the long term.

Discover more from MassMutual ….

When markets dive, keep your strategic calm

5 ways to prepare for an economic downturn

________________________________

1 Source: Bloomberg, and MassMutual Research as of February 24, 2022

2 Source: Bloomberg;

3 Source: FRED, Bloomberg as of Jan. 24, 2022.