Every four years, a closely watched event occurs: The presidential election. We cast our ballots and do our civic duty to vote for whom we believe represents our values and our vision. In less than two short months, we will be casting those votes again. As such, because this is a market update, we will explore how markets have historically reacted to those events, and what, if anything, we should do about it.

Therefore, what follows are two sections. First, we review the latest on the pandemic (because, after all, it seems to be the primary determinant of our lives and the markets right now). Second, we dive into the past hundred years of markets and try to provide some perspective on how markets react to various political winds. Remember, my goal is not to predict the future (because that has shown to be a futile exercise); my goals are instead to:

- Separate fact from fiction.

- Offer some perspective using history as a guide.

With that, let us begin.

COVID-19: Where we stand

As of Sept. 16, there are nearly 30 million people that have had confirmed COVID-19 infections. Nearly 7 million of those are in the United States. Tragically, we are now close to passing 1 million deaths worldwide, and nearly 200,000 of those have come from the United States.1

These are remarkable numbers both for their absolute size of the human loss and the incredible sadness that accompanies those numbers. Remember, for context, there were roughly 400,000 Americans killed in World War II. We are clearly in the midst of an event both terrifying and historic, and we are not yet out of the woods.

Having said that, there continue to be signs of hope.

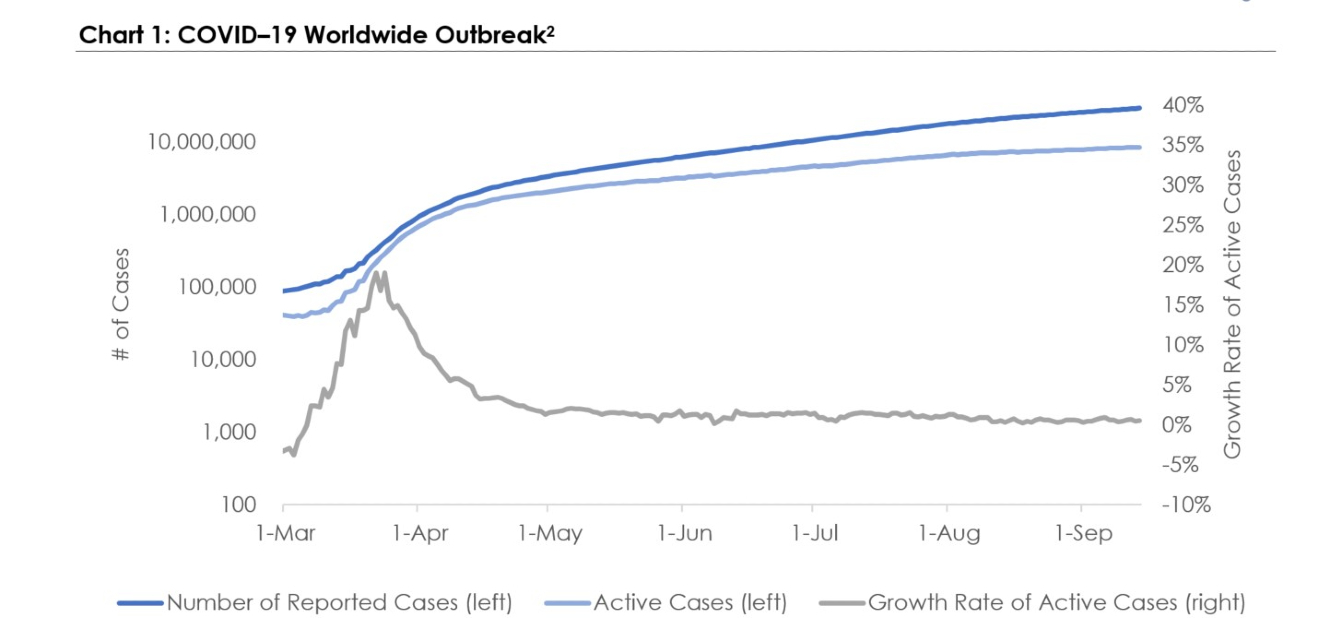

I continue to reference Charts 1 and 2 below because I believe they demonstrate what is happening in the world with respect to COVID-19. They a) ignore the headlines, b) zoom out far enough to discern the relevant trends, and c) show both the levels and growth rates. (I continue to argue the growth rates are what matters and what the market is focused on.)

To orient, the blue lines demonstrate the total number of cases around the world and correspond with the left axis. The grey line demonstrates how the number of cases is growing and corresponds with the right axis.

The summary, thankfully, is that the growth rate of cases continues to slow. Both globally and domestically, the outlook continues to improve, and in dramatic fashion. Each time we check the statistics, we are thrilled to see both case and death growth rates continue to fall. Things are getting better, and markets continue to demonstrate significant levels of optimism.

During the last update, I wrote that case growth in the United States had fallen to all-time lows (since the pandemic began), which, fortunately, has continued.

Back in March, when COVID-19 was spreading rapidly, case growth in the United States was growing at more than 30 percent per day, which was both terrifying and unsustainable. We, as a society, made changes, and growth rates fell to the mid-teens in April, down to 2 percent in June, and now, U.S. COVID-19 cases are growing at less than 0.6 percent per day (on average).2

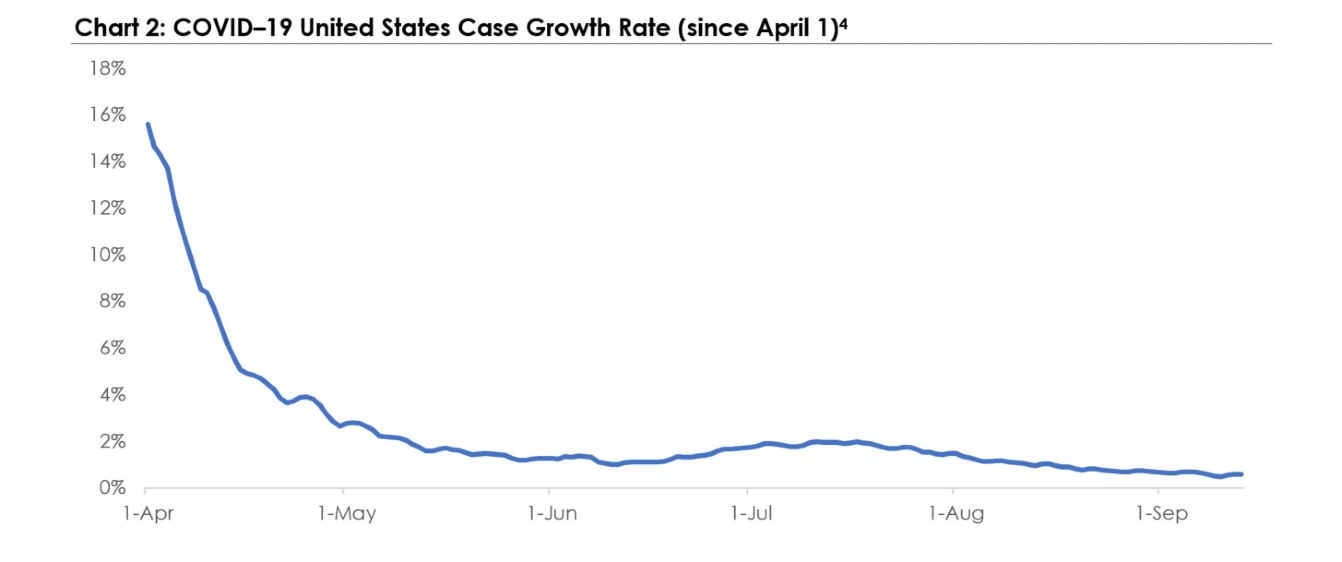

Chart 2 demonstrates this further by zooming in on the growth rate since the beginning of April.

The blue line (U.S. only) in this chart corresponds with the grey line (global) in Chart 1. The growth rate was very high in early April, then fell very quickly, then rebounded a bit toward the beginning of July (as growth in the South exploded) and now continues to find all-time lows (roughly 0.59 percent on a five-day smoothed basis).

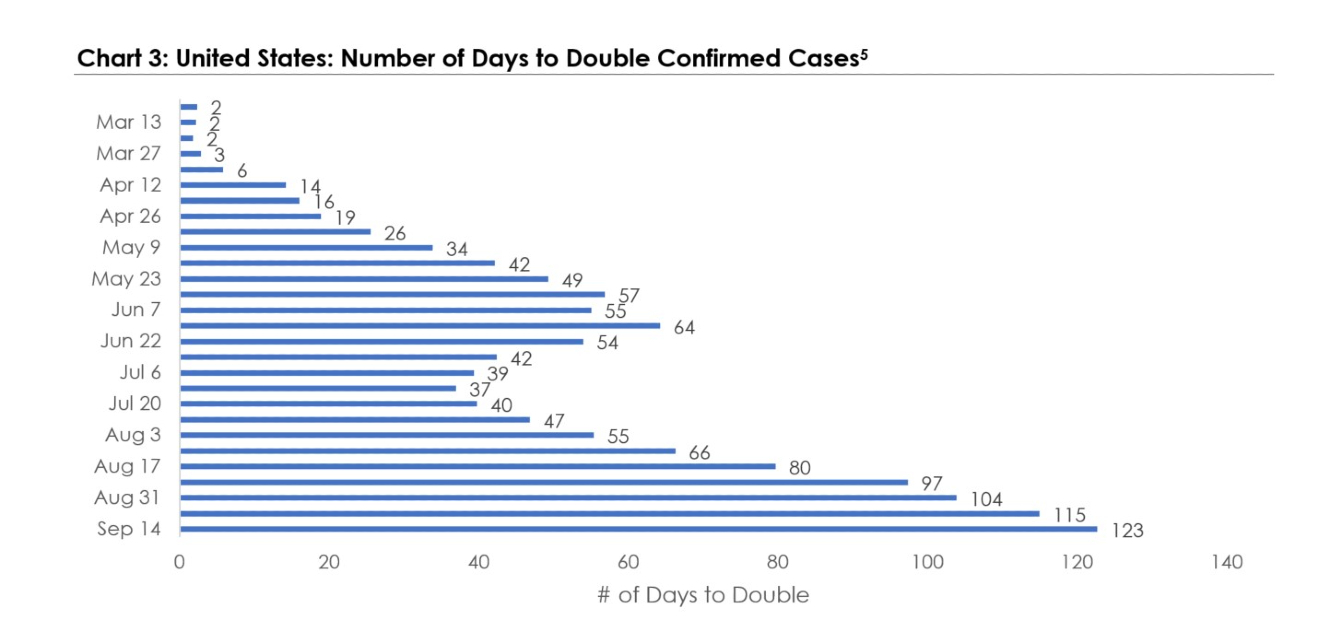

Lastly, Chart 3 takes the very same data and converts it to the number of days to double the cases in the United States. This is often a more intuitive and relatable way to understand how growth rates are changing.

The chart largely follows the story of the United States. In late March, the U.S. was in complete lockdown as case growth was largely out of control. At that point, the U.S. was doubling cases every three to five days. We learned, we evolved (and no, not quickly enough), but we nonetheless improved to late May and early June where we were doubling cases every 64 days.

The South then began to re-open, and many states pushed back entirely on some of the government guidelines. Growth rates increased again, and the days to double fell to 37 days on July 13.

Fortunately, the trend continues to improve.

The U.S. is now doubling cases every 123 days, which is an all-time high (meaning growth is at an all-time low) since the beginning of the pandemic in March. Despite schools re-opening, and many Americans returning to semi-normal activities, growth rates continue to slow. While lessons abound as to how we could have handled this differently, this is very positive news nonetheless, and offers significant hope.

Presidential elections

Given the sensitivity of the topic, and the polarity of views, this is a delicate update to write. As such, let us establish some ground rules.

- First and foremost, I want to make clear I am not offering a prediction. I am simply using historic data to help us think about what decisions we can make now with respect to our portfolios.

- Second, I am trying extremely hard to remove my own political views from my analysis. Accordingly, I won’t select certain time periods to prove a point or tilt the data to skew the story. As much as humanly possible, if well delivered, this will simply be perspective and thoughts that (hopefully) will help us all make higher quality decisions.

With that preamble out of the way, let us begin.

As sensitive as the topic is, let us first set the scope of what we want to cover. As most betting markets are, so far, showing a toss-up for the election on Nov. 3, it is important to be clear on what we want to answer and what we do not.3

To help guide us, I will explore three primary questions:

1) Are markets in election years more volatile or unique in some way?

2) Does incumbency matter to markets?

3) Historically, do Democratic or Republican presidencies tend to generate higher market returns?

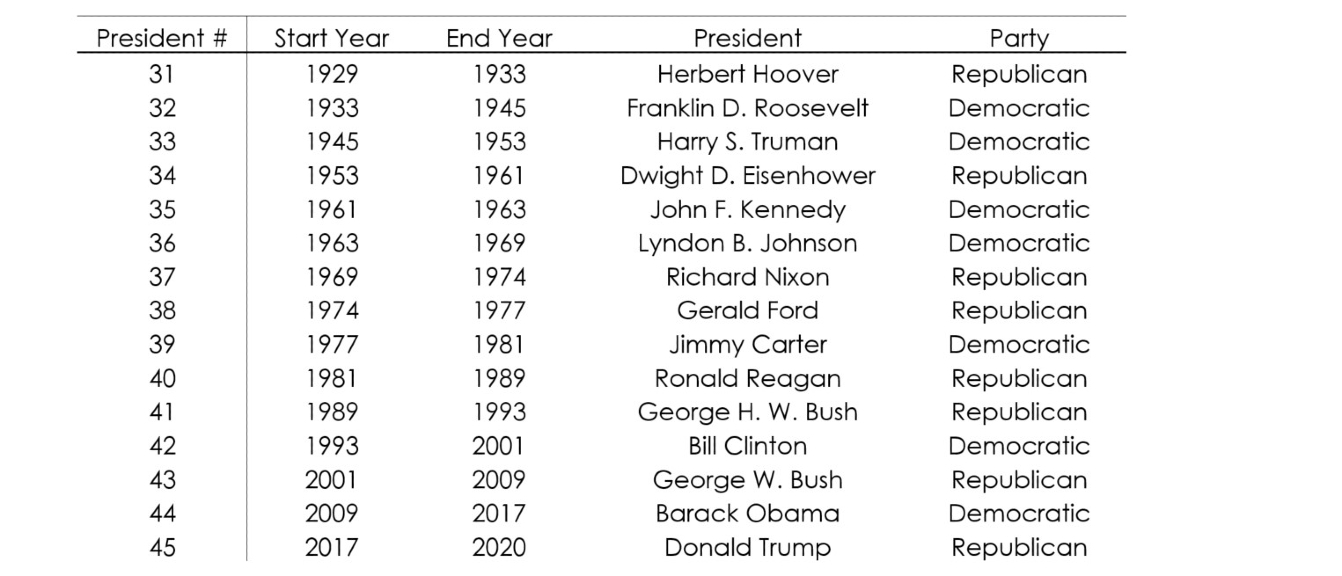

As to the scope, I began roughly 90 years ago because I felt it important to include the Great Depression, but didn’t want to complicate the analysis by going back into very different monetary policies, political systems, and the like. As such, the following presidencies and data ranges are the primary focus:4

Accordingly, this represents 15 different presidents over a period of 92 years and covers 23 election years. Let us now turn to the questions.5

Are markets in election years more volatile or unique in some way?

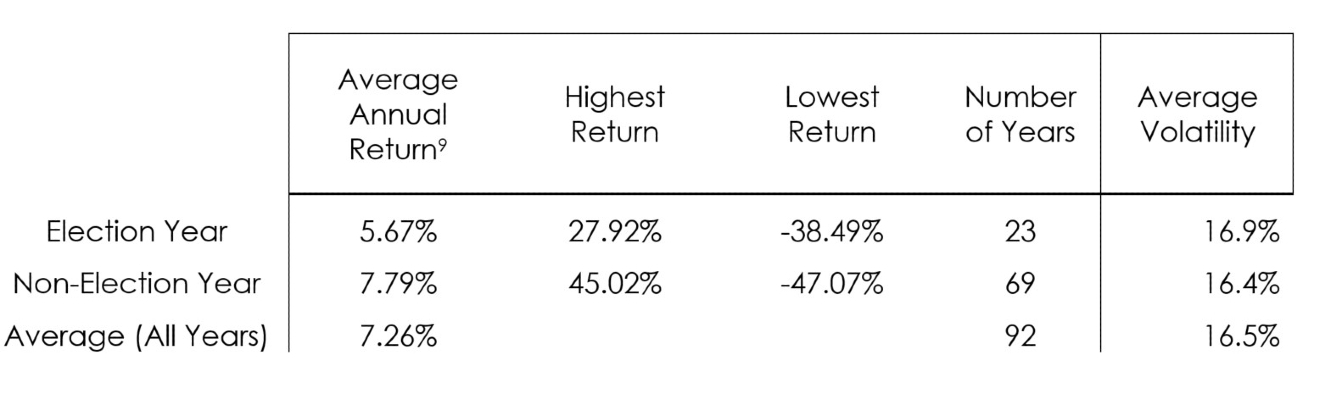

I am frequently asked whether markets in election years are more volatile or hold a higher risk of selloffs. While history is only a guide (and not a crystal ball), historically the answer is no.

We looked back at the daily returns of the Standard & Poor’s (S&P) 500, and then gauged volatility during the years of presidential elections and in non-presidential election years. In short, volatility has been remarkably consistent.

Further, a related perception is that equity market returns are worse during election years, after all, there is a good bit of uncertainty during election years. While that is true at the margins, it is only slightly so. Since 1929, the average annual return was 7.26 percent, while the election-year average was 5.67 percent and the non-election-year average was 7.79 percent.

In short, election years have historically been a bit less positive, but positive nonetheless, and similarly volatile as other years.

Does incumbency matter to markets?

The next question addresses stability. Once an election occurs, if the party changes, there is often a full reboot of our political system. Policies are re-written, employees are fired and re-hired, entire agencies are replaced or closed…in short, chaos often ensues before stability returns. As such, I would imagine that economic growth would encounter some challenges as the new policies begin to take hold, and this is largely what we see:

From 1929 through today, in the year following an election when the presidential party changes, markets return roughly half of what they return in the year following an election when the presidential party doesn’t change.

An example is the Johnson to Nixon election of 1968. Lyndon B. Johnson, a Democrat, was replaced by Richard Nixon, a Republican, beginning in 1969. Accordingly, in the year following Nixon’s election, the S&P 500 returned roughly -11.36 percent.

In short, markets generally like stability and certainty, and changes in presidential parties, on average, have historically produced less positive market returns.

Historically, do Democratic or Republican presidencies tend to generate higher market returns?

Since 1929, of the roughly 91 years, 48 have been governed by a Democratic president, and roughly 43 have been governed by a Republican president.

That time period has covered wars, depressions, famines, pandemics, crashes, rallies, and everything in between. There have been great policies and terrible policies, and great decisions and some less great decisions. We have had a range of monetary approaches and an even wider range of fiscal approaches.

And yet if we distill that down into a very simple lens, there are some interesting takeaways.

First and perhaps surprising to many, Democratic presidencies have tended to outperform Republican presidencies.6

The first column represents the annualized return of essentially holding the S&P 500 on the days governed by a Republican or a Democratic president. The pushback is often, yes, but it’s not fair because Hoover (a Republican) oversaw the Great Depression. Fair enough, the second column represents the same data but removes the Great Depression time period, and instead, begins with Roosevelt (a Democrat).

Interestingly, at least in rough form, the results roughly hold.

Aha, say the Democrats, we finally have our proof!

Well, let’s slow down for a moment. To truly determine political impact on the markets, we need to consider corresponding House of Representatives and Senate majorities and how much political goodwill was in hand. We would need to inquire what valuations were when the presidencies began. We would need to understand how accommodative monetary policy was, and if there were exogenous factors (like COVID-19, for example) that affected the results. We would then need to understand more about how consumers were borrowing and spending, and also think about the impact of how businesses were behaving. Were they spending and hiring, or were they saving, and perhaps buying back their stocks? Also, how were bonds performing, and what was the cultural sensitivity around buying stocks at the time (in the stagflation of the 70s, for example, stocks were largely out of preference).

And this is largely the point: the system is incredibly complex.

We can retrieve individual lenses and view the market through those perspectives, but they are, by definition, inherently narrow. Much as the three blindfolded people who view the elephant by feeling the trunk, the leg, and the tail, we can view the market through simplistic viewpoints, but it is generally futile to try and predict where it is going.

In closing, let’s try to summarize what we have learned:

- First, we confirmed markets return slightly more during non-election years than election years, but volatility during those time periods is largely the same.

- Second, we confirmed markets generally prefer stability (as proxied through presidential incumbency).

- Lastly, we confirmed that, historically, Democratic presidencies have outperformed Republican presidencies (at least through a fairly simplistic lens).

What, therefore, should we do? On Nov. 3, we should vote. Aside from that, we should do nothing we wouldn’t ordinarily do.

Our investment portfolios should be built to withstand the gyrations and volatility of the short term and deliver above-inflation returns over the long term. No one knows who will win the election, and even if they did, it isn’t clear what market move would make the most sense.

What does make sense is that incentives drive behavior, and companies (and the people that run them) are subject to those incentives. Capitalism creates those incentives and, regardless of the presidency, those incentives exist for productive purposes, and will continue to exist after November 3rd. Companies will still produce what they produce and will continue to try to do so in an effective and competitive manner.

We, should, as owners of capital, and therefore investors in those businesses, benefit from that allocation of capital by receiving a return on the capital we invest in exchange for the risk we endured. That dynamic is true regardless of which candidate is elected president on Nov. 3.

In short, save. Minimize taxes and costs. Stay aware of your emotional reaction to market events only as a barometer for whether your portfolio is calibrated properly. Plan with your investment professional for the long term to ensure you meet the goals that are important to you.

And lastly, stay safe, and turn off the investment news channels.

Discover more from MassMutual ..,

3 ways to financially prepare for an election

Estate planning for high net worth households

How to grow wealth: 3 strategies

_________________________________

1 Source: Johns Hopkins University as of Sept. 15, 2020 https://www.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6

2 Sources: Bloomberg, World Health Organization as of Sept. 15, 2020

3 https://www.worldometers.info/coronavirus/country/us/

4 Sources: Bloomberg, World Health Organization

5 Sources: https://www.worldometers.info/coronavirus/country/us/, as of Sept. 15, 2020

6 https://www.betfair.com/sport/politics as of Sept. 16

8 Note: 1929 and 2020 are partial years

9 Source: Bloomberg, as of Sept. 15, 2020

10 Source: Bloomberg, as of Sept. 15, 2020

11 Source: Bloomberg, as of Sept. 15, 2020