| ||||||||||||

Real estate markets are volatile right now. So much so that some are wondering if a significant correction may be in store. To analyze the market forces at work, it might be useful to remember a certain allegory taught in most introductory philosophy classes.

It concerns a deep cave within which sits a row of people, who have never known life outside the cave, staring at a wall. Behind these people is a large fire that casts light onto the cave wall. And between the fire and the row of seated people is another set of individuals, who are raising images in front of the fire which are in turn reflected on the cave wall.

For the people on the floor watching the images, how do they discern what those shadows really mean — what is real and what is a replica? For example, is the image of a dog bounding across the cave wall “real,” or just a replica of something real? And importantly, how does the viewer know? They are clearly experiencing the image which, according to some, is what makes a thing real.

Now keep this allegory in mind when thinking about real estate.1 What, after all, drives the price of real estate?

- At the fundamental level, it is some dirt, some boards, some wire, and some paint. Clearly real estate is just the sum value of those materials, right?

- Or is it something more? Is it the collection of experiences in the home, or is it the collective value created? Where does perception come into play?

- If I take those same raw materials and assemble them in one state versus another, why, for example, does the price of that real estate change so significantly?

- Further, if I took those boards and paint four years ago, I would have one price, but if I did the same thing today, I would have a drastically different price. Why is that? My needs for the home haven’t changed dramatically. It is still a place to sleep, and protect my family … so does it really make sense that the price is now nearly twice what it was three years ago?

Therefore, for our purposes, we will explore the drivers of real estate (both past and present), and attempt to provide some perspective on the environment we are in.

Inflation continues to dominate

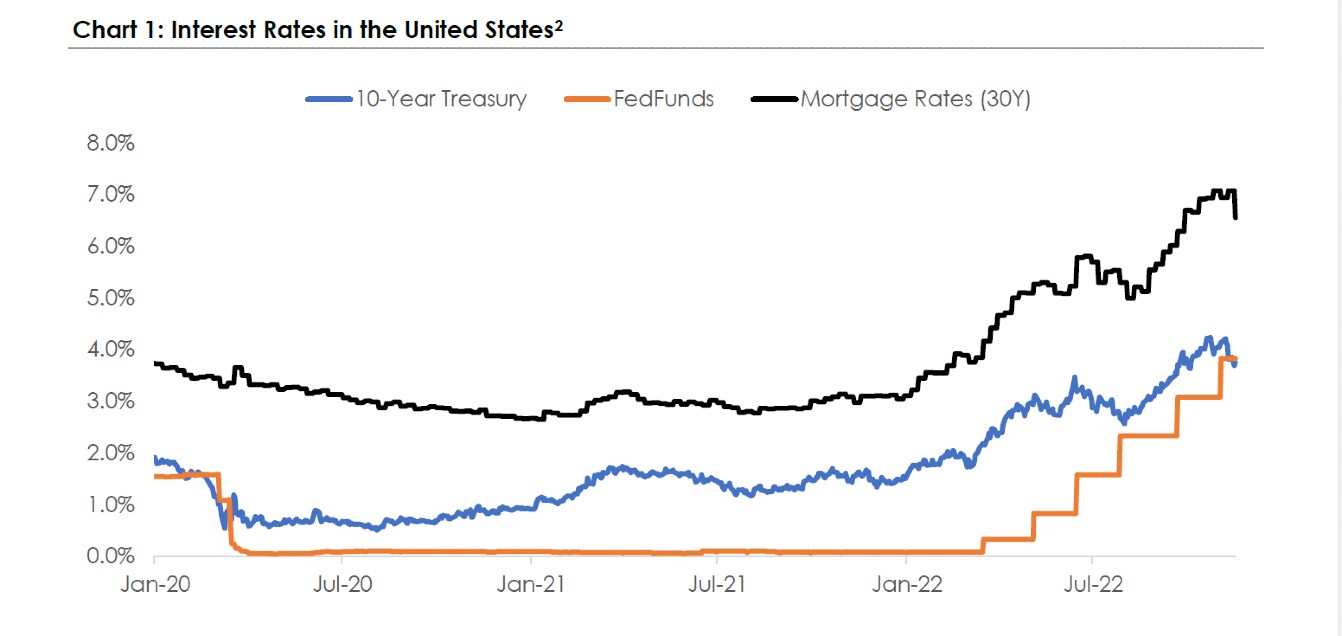

As we have discussed (many, many times), inflation has been, and remains, the dominant macroeconomic theme of 2022. We covered the “why it has occurred” and “what the Fed is doing about it” in prior updates, and yet Chart 1 likely demonstrates the best view of the “effects of inflation.”

The orange line is the rate the Federal Reserve (mostly) controls. The blue line is what the market has adjusted to given changes in inflation and the change in the orange line.

Interestingly, the black line is the average US 30-year mortgage rate, and that has, for a number of reasons, continued to move higher.

If, for example, someone wanted a $500,000 mortgage at the beginning of 2021, the monthly payment would have been just barely over $2,000. The same mortgage at the end of last month (November 2022) would have been $1,345 more…for a total of $3,360 per month (before taxes and insurance).

Clearly a remarkable difference, and obviously one which is likely to decrease demand.

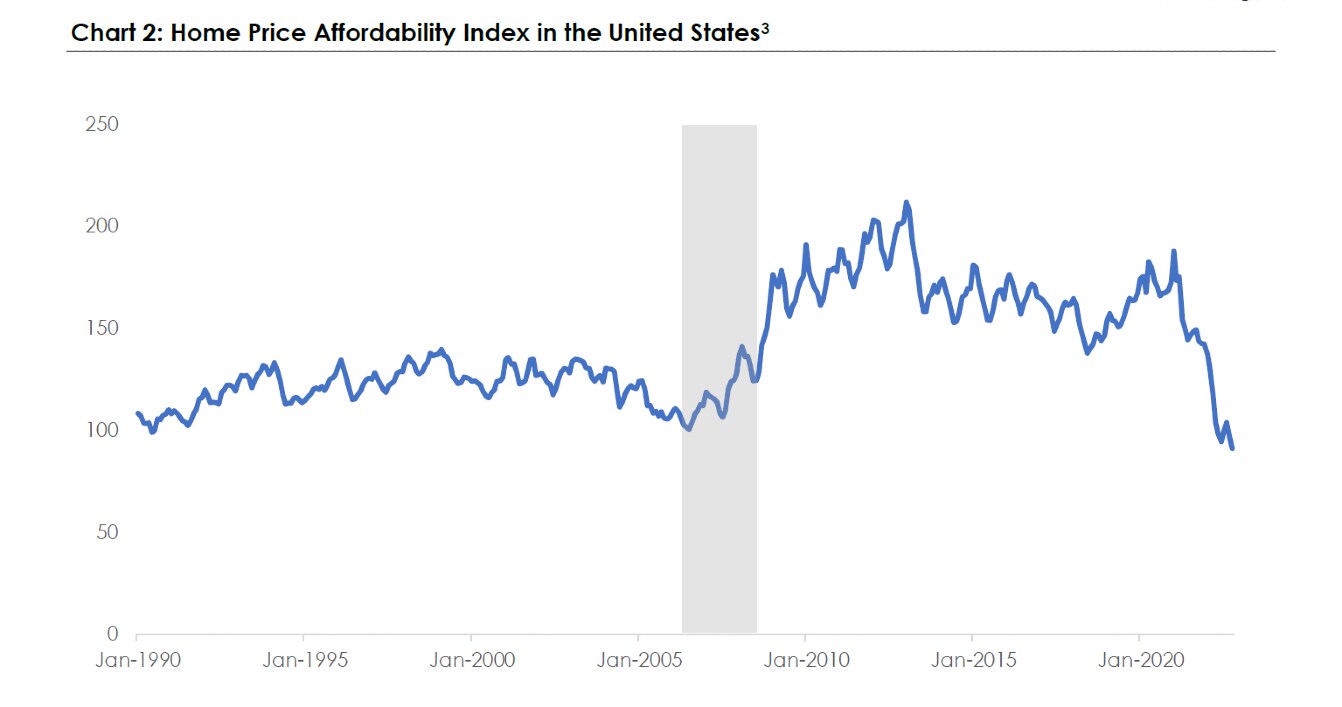

Chart 2 takes this same information but adds the fact that while mortgage rates have increased, so have the cost of houses.

To orient, when the line is at the top of the chart, the cost of owning a home is, on average, more affordable. When the line is at the bottom of the chart, the cost of owning a home is, on average, expensive.

As the chart demonstrates, we are now at a point where, between the combination of home prices and mortgages rates, it is now more expensive to own a home than right before the global financial crisis occurred.

What's different?

It is tempting, as many pundits have done, to confuse correlation with causation, and claim “therefore, we will see a similar level of crisis as we did in 2008.” While we are never confident enough to predict with certainty, there are several things that make this markedly different than the period before the global financial crisis.

- First and foremost, there is much less consumer leverage in the system. Leverage is one of the strongest indicators of a “crisis to be”, and we are not seeing those signs so far.

- Second, one of the causes of the inflation we are experiencing was an unprecedented increase in money supply … which resulted in unprecedented amounts of cash held by consumers. This reduces the likelihood of forced sales en masse.

- Third, wages have increased rapidly along with an especially strong job market, which further reduces the risk that homeowners are forced to sell urgently.

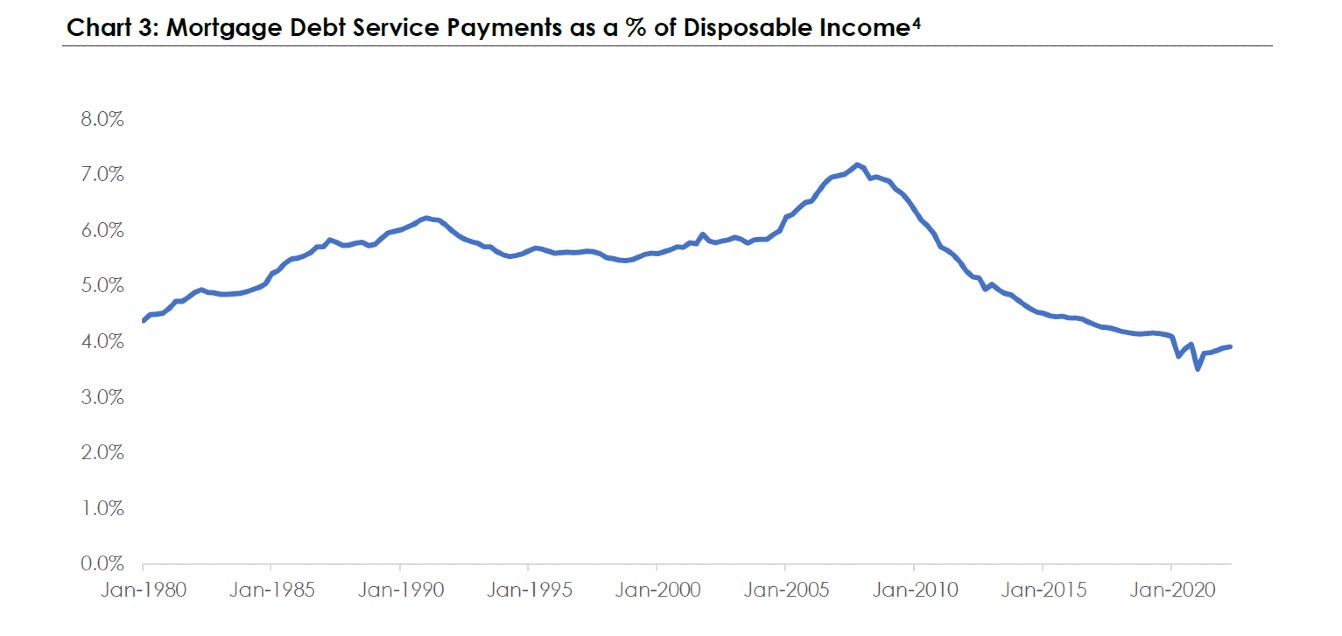

This brings us to the final chart of the day…probably my preferred perspective for understanding current pressures in the residential real estate market.

This chart shows the required debt service payment as a percentage of disposable income in the United States. To be clear, there are some flaws to this calculation, but it does give a sense (particularly relative to history) of how the cost of debt has changed as incomes have changed.

The obvious takeaway is that consumers felt significant amounts of stress in 2007 (for example), that they clearly don’t feel now. While there are many other factors at play … particularly given the Federal Reserve is not yet done raising rates and the economy is just beginning to slow … this is clearly a positive sign that leans us towards believing real estate will slow, but it is unlikely to crash.

In short, while prices and interest rates have moved higher, we see few reasons for a harsh correction in real estate and we lean more towards a slow creep down for the foreseeable future.

Discover more from MassMutual …

3 ways to consider market volatility

When markets dive, keep your strategic calm

How higher interest rates may hit consumers

________________________

1 With courtesy (and apologies) to Plato, who referred to this as the allegory of the cave and used this to argue why philosophers are valuable.

2 Source: Bloomberg, US Treasury, MassMutual WMIT Research, as of Dec. 19, 2022.

3 Source: National Association of Realtors, Bloomberg, MassMutual WMIT Research, as of Dec. 19, 2022.

4 Source: St. Louis Federal Reserve, MassMutual WMIT Research, as of Dec. 19, 2022.