Before we begin our analysis of COVID-19 and the markets, let us begin with a story.

There once was a boy born into a middle-class family, with plenty of opportunity and resources. As a young child, the boy demonstrated significant intellectual abilities, so his family did everything they could to ensure he received an education (uncommon at the time) and every opportunity possible.

As the child grew, he generally succeeded in his local village schools. He received top marks on a couple of key exams and was eventually asked to enroll in one of the larger, more competitive schools in a nearby town.

While he had been successful in his local village, as the competition and rigor increased, unfortunately, he failed the next threshold exams and was forced to return to his village to pursue agriculture.

Undaunted by the failure of the first exam, this young man tried again the next year. Unfortunately, he failed again. Mustering up the strength to try one more time, he signed up and dutifully took the exam a third time. While effort accounts for a good deal, unfortunately, again…he failed.

A lesson in risk

This seemingly simple story holds an important lesson for us all: namely, the story of risk. Let us consider that what we know thus far can be considered fundamentals: the building blocks of the path we believe this young man will follow. Given his failures thus far, and what we know about his surroundings and upbringing, based on the limited information, it would seem logical to expect the young man will likely return to his village, and follow the agrarian lifestyle.

That view, in essence, is our range of expectations. We believe, based on what we know, that this young man is likely to go down a certain route.

The risk, therefore, is that we have made faulty conclusions. As with markets, humans are driven by generally predictable motivations and incentives, but often exogenous variables intervene and paths change.

There is no crystal ball

With that digression, let us return to the story to see what happened. This young man was named Hong Xiuquan, and he was born in 1814.

After he failed the third exam, Hong had a nervous breakdown, and it was during this breakdown, that Hong dreamt of visiting heaven. With little knowledge of Christianity other than some pamphlets he had read, Hong believed he was the younger brother of Jesus Christ and somehow managed to convince many others of the same idea.

Between 1850 and 1864, Hong led what remains the bloodiest civil war in history and the largest conflict of the 19th century. Somewhere between 20 and 30 million Chinese perished (although some estimates are as high as 70 million) in what is now known as the Taiping Rebellion.1

This, ladies and gentlemen, is one definition of risk. The idea that a negative, and unexpected,

consequence can occur that is far outside the realm of expectations. Given the fundamentals previously discussed, it is fair to say very few would have predicted the subsequent bloodshed that occurred.

In many ways, this concept of risk was similarly demonstrated in 2020.

Beginning the year, the fundamentals of our economy were reasonable. The government was largely accommodative, the consumer was optimistic (demonstrated through borrowing and spending) and, while businesses had some issues (frustrating lack of capital expenditures), profitability was high and unemployment was quite low.

And yet…

We experienced one of the largest exogenous shocks in recent memory: COVID-19. It was not expected, it was largely not contemplated, and we clearly weren’t ready for it. That is … in a word … risk.

The 1973 commodity shock was not expected. The inflation of the late 70s was not expected, the efforts of Paul Volcker, former chair of the Federal Reserve, to break the back of inflation in 1980 were not expected, the crash of ‘87 was not expected, nor was the 40-year bull market in bonds, or the dotcom crash, or the Global Financial Crisis, or, etc., etc., etc.

This is precisely why risk occurs. If we expect or contemplate the risk, then we will likely have dealt with it, or at least prepared for it. Risk is what happens outside of our expectations.

The four chapters of 2020

As such, today, with the year ending, we will focus on four dimensions of the year, while concluding with how to deal with risk itself. This will be a story largely told through four chapters, namely: COVID-19, the U.S. Government, the consumer, and U.S. equity markets.

With that, let us begin.

Chapter 1: COVID-19

Unfortunately, 2020 will go down as the year of the coronavirus. With any luck, 2021 will hopefully go down as the year of the vaccine.

Regardless, let us go back before we go forward:

As of Dec. 10:

- There are now more than 69 million people worldwide that have had confirmed COVID-19 infections (a little less than 1 percent of the world’s population).2

- There are now more than 15 million Americans that have had confirmed COVID-19 infections (roughly 4.7 percent of the United States population).2

- There have been a bit more than 1.5 million deaths attributable directly to the COVID-19 virus, and nearly 300,000 of those came from the United States.

From a United States perspective, as I have argued throughout the year, markets have been optimistic for several reasons:

- Growth rates (of both cases and deaths) were unsustainably high in the beginning of the year, but fell rapidly as we learned, evolved, and protected the most vulnerable portions of our populations.

- Death growth rates fell more quickly than case growth rates and have remained low despite the summer jump in cases and, more recently, the post-Thanksgiving increase in cases.

- Vaccine development began with a level of cooperation and at a pace previously unimaginable in the history of the world.

In short, markets have been looking past the abyss and have focused on the positive developments to come.

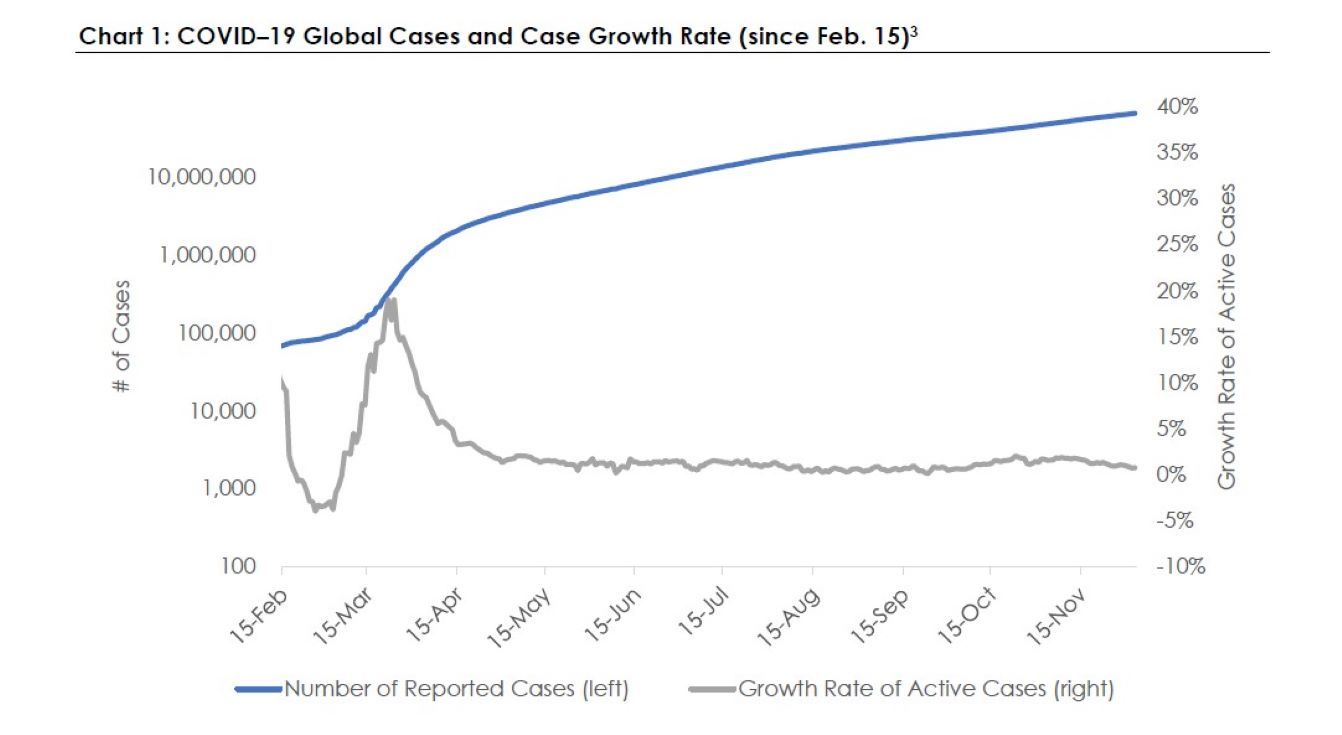

Charts 1 and 2 provide a bit more context. Chart 1 lookes at COVID-19 growth rates globally:

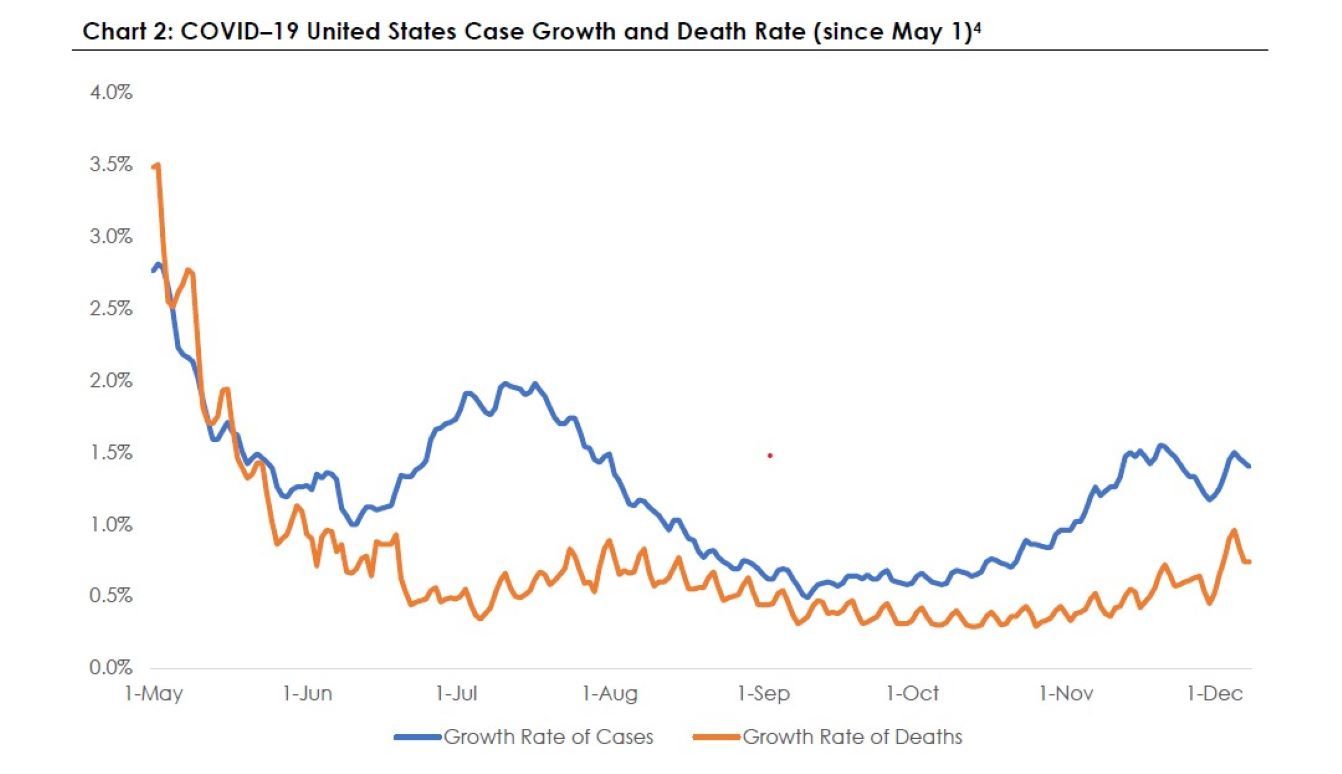

Chart 2 looks specifically at the United States:

In short, absolute numbers continue to climb worldwide (clearly bad news), while growth rates of those numbers have fallen (less bad news).

While there is no good news to be had, we are at least finding ways to co-exist until the vaccination development and production can be delivered in earnest … and, as all know, that can’t come soon enough.

Chapter 2: Federal Reserve

For this next section, we look to another material driver of markets this year: the U.S. Federal Reserve.

As a reminder, the U.S. Federal Reserve is essentially the central bank of the United States (and perhaps philosophically, the world).

The Federal Reserve has essentially two primary mandates:

- Price stability — the responsibility to ensure prices of goods and services are stable and expected, and

- Maximum Sustainable Employment — the responsibility to ensure Americans are employed to the maximum possible sustainable level.

The question, and one that is debated ad infinitum, is how far can or should a Federal Reserve go to achieve those mandates? Regardless of one’s view, let us look back at 2020 for a perspective to that question.

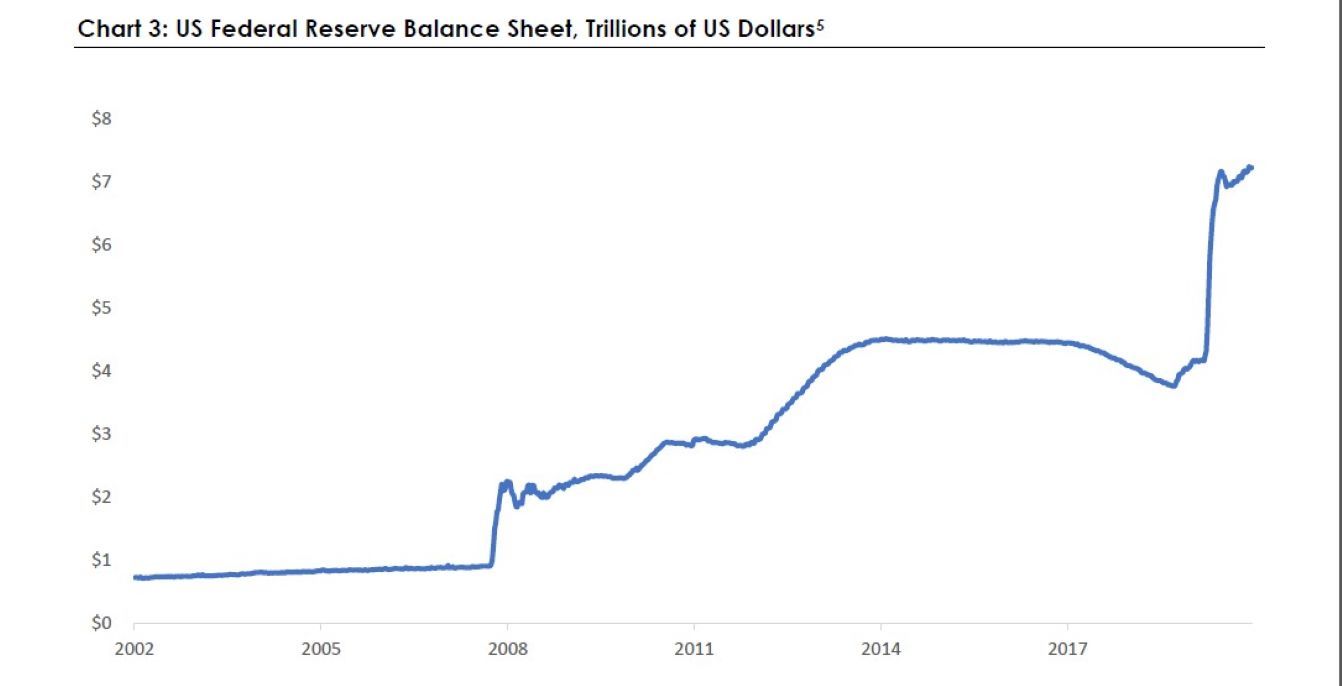

The U.S. Federal Reserve witnessed the crisis of March 2020 and expanded its balance sheet from a previously “hard to understand” size to an “even more unfathomable” size.

As of this writing, the Federal Reserve (through its various levers) has essentially created a bit more than seven trillion dollars out of thin air and has used those dollars to:

- Provide liquidity.

- Purchase assets.

While there are clearly questions of what occurs when the Federal Reserve begins to reduce its balance sheet, at a minimum, the massive infusion of capital played a major role in re-inflating markets and pushing equity markets to where they are today. What happens in the future is a topic for another letter…

Chapter 3: U.S. Consumer

As we’ve discussed before, as goes the U.S. consumer, so goes the economy. In an economy of roughly $21 trillion, the U.S. consumer is one of the prime determinants of growth.6 As such, when the COVID-19 shutdown occurred in March, and consumers were forced to stay home (and therefore stopped spending money), the economy stalled.

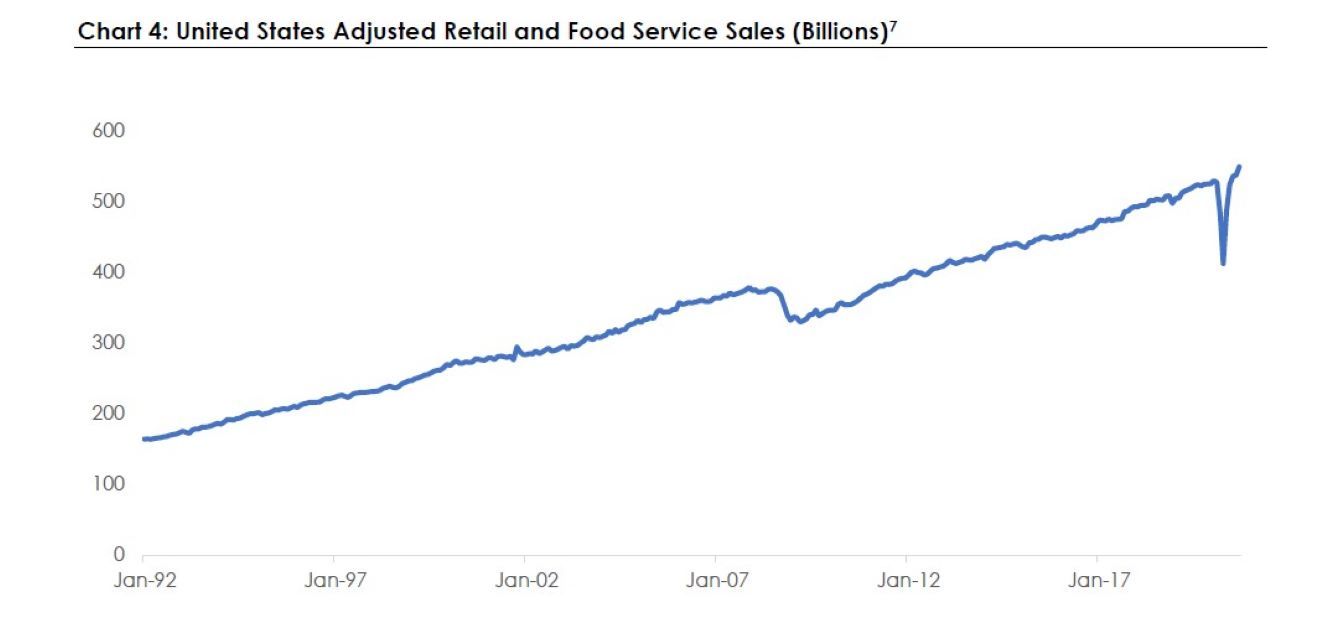

One of the best barometers of the consumer is retail sales. Produced monthly by the U.S. Census Bureau, this number essentially measures the total purchases of durable and non-durable goods from all food service and retail stores.

The summary from Chart 4 is:

- The consumer took an unprecedented pause on spending.

- The consumer picked up where they had left off with remarkable speed.

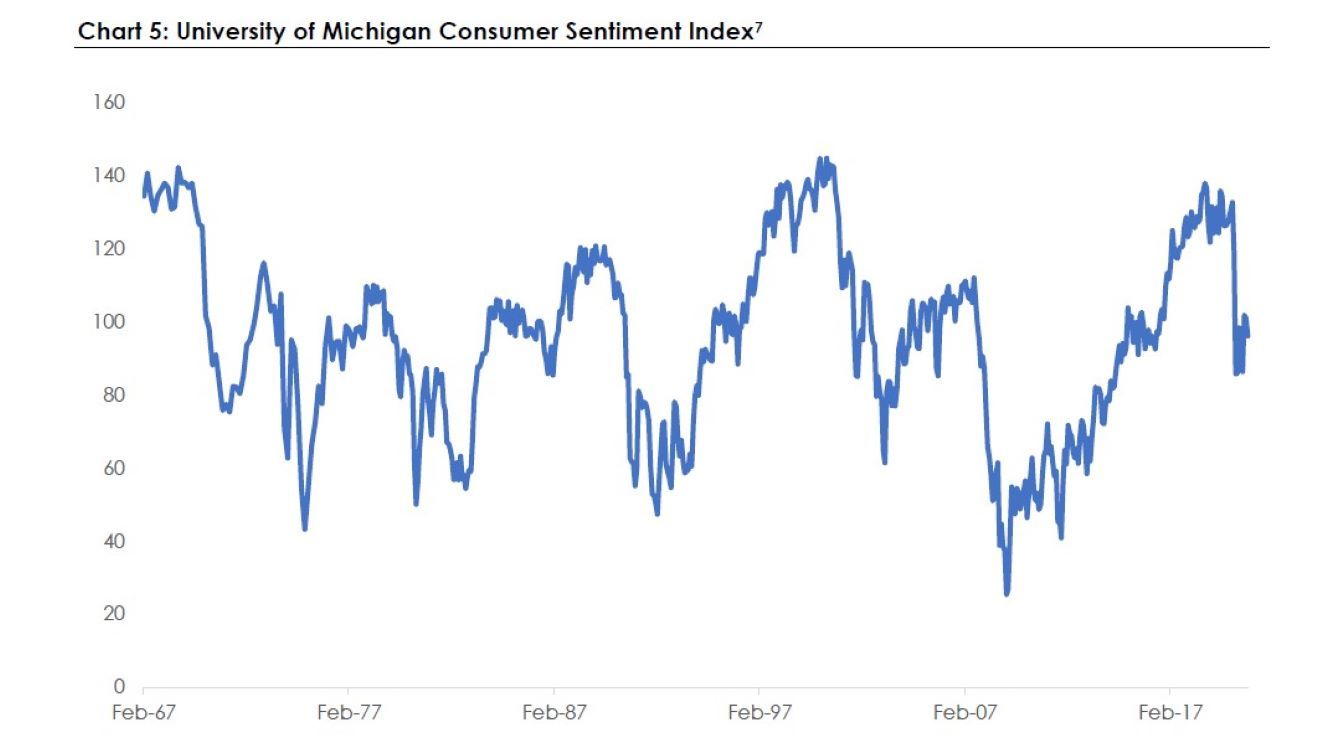

To get a better sense of how the U.S. consumer is feeling, we can literally ask them. The University of Michigan has a particularly useful consumer sentiment survey that is reasonably objective and has a reasonably thorough history. This data is shown in Chart 5.

Interestingly, the U.S. consumer, arguably because of the massive amounts of stimulus provided, never fell to the levels of pessimism that occurred during any of the recent recessions (Global Financial Crisis, Dot Com Bubble, 90/91, etc.).

This can potentially enable rapid economic growth once there is a return to normalcy … particularly if the U.S. Government (including the Federal Reserve) remains in its stimulative stance.

Section 4: U.S. Equity Markets

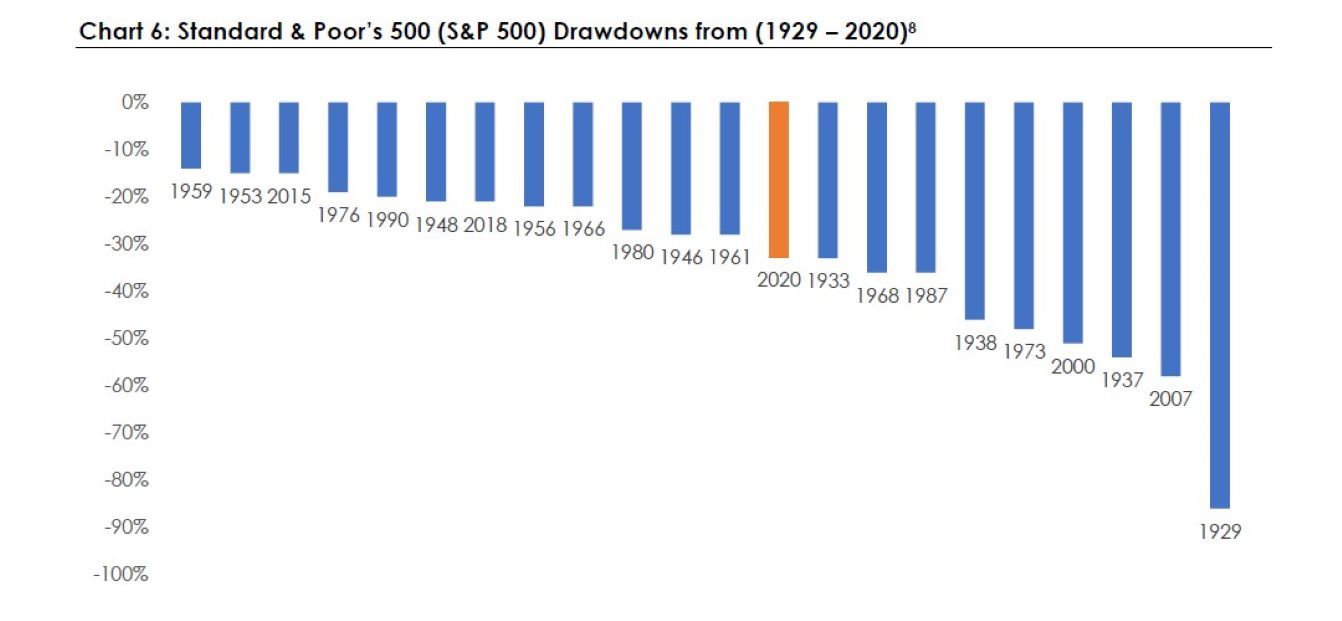

For a moment, let us revisit and acknowledge the speed, the level of fear, and the depth of the sell-off that occurred in March. It was terrifying for many and confusing for nearly all.

It was, perhaps interestingly, also about middle of the pack relative to other drawdowns over the past 100 years. Chart 6 displays every drawdown worse than 15 percent going back nearly 100 years.

As a reminder, between Feb. 14 and March 23, the Standard & Poor’s 500 (S&P 500) lost roughly 33 percent.9 This is more than the sell-off in 1959, for example, but far less than the dramatic losses of 2007 and 1929.

Therefore, again, before we move forward, let us summarize what we have experienced:

- We started the year with good, not great, fundamentals from the U.S. consumer, U.S. businesses, and a supportive Central Bank policy.

- We encountered an unknown risk in the form of the COVID-19 virus that subsequently shut down the U.S. economy, forced consumers to stay home, closed businesses, schools and community gatherings, and rapidly changed how we engage as a society.

- As a result, equity markets around the globe sold off rapidly and harshly.

- The U.S. Central Bank (and Central Banks around the world) responded with an unprecedented level of stimulus.

- Consumers responded tepidly, unemployment remains higher than desired, and the U.S. economy has begun, but not yet achieved, a slow climb back to previous levels.

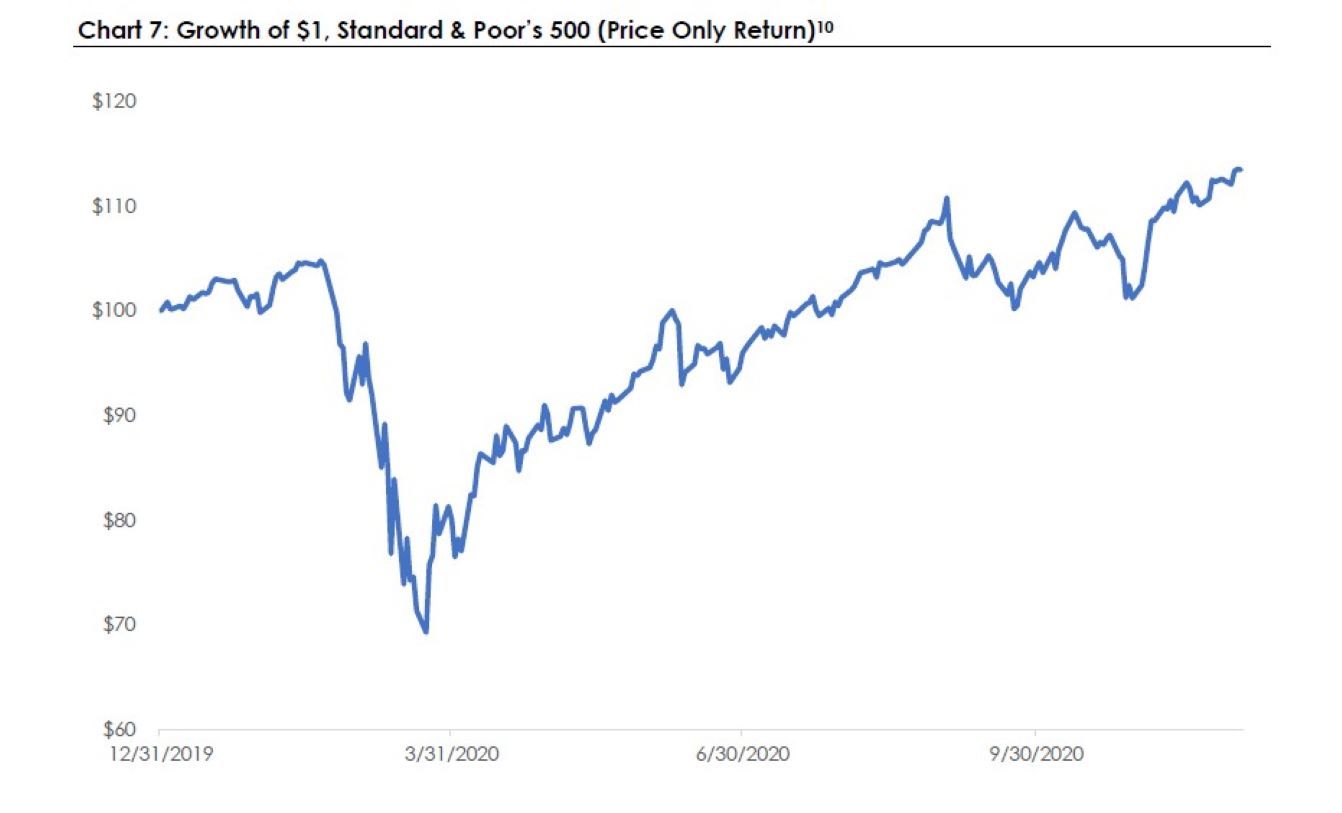

This, then, brings us to our final chart for this retrospective. The total performance of the S&P 500 for the year.

As we all witnessed, this chart tells the story of two distinct experiences. First, a very rapid and fear-stricken sell-off in February followed by, second, a steady and fairly remarkable increase since the low on March 23 that has now placed equity markets in fairly strong positive territory for the year.

Having started with $100 on Dec. 31, 2019, if an investor had fallen asleep after investing in the S&P 500, and then awoken this morning, they would have roughly $112 in their possession.

What then, are we to make of it all?

I offer no predictions, but I will offer that this year, while clearly unique, is a fairly good synopsis of the investing experience. We analyze and optimize what we know and understand, and yet we prepare for that which we don’t. Thoughtful investors recognize that the short term is remarkably confusing and unpredictable, and therefore, we should, as much as possible, try and stay focused on the long term.

What drives strong investing returns over the long term are structural incentives. Capital markets, as extensions of capitalism, provide those incentives. I, as an investor, provide a company with capital for productive purposes. If that company is effective with my capital, I will benefit as the company produces its goods and services, and provides me with a return of, and on, my capital.

We, then, as investment professionals, build portfolios to take advantage of those structural incentives, while striving to build those portfolios to protect us as much as possible from the unknown.

The year of 2020 provides a wonderful lesson in that regard. The protection of capital is paramount and must always be considered.

In short, control what can be controlled. Save, mitigate taxes, minimize expenses, and be quite cautious and thoughtful about taking unnecessary risks … for it is those risks we haven’t contemplated that put our capital in the greatest peril.

In closing, stay safe, and please turn off the investment news channels.

Discover more from MassMutual…

Crazy stock markets? Count your financial eggs

Need financial advice? Contact us

________________________________

1 https://www.history.com/topics/china/taiping-rebellion#:~:text=Estimates%20vary%2C%20but%20the%20Taiping%20Rebellion%20is%20believed,one%20of%20the%20deadliest%20conflicts%20in%20human%20history

2 https://www.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6

3 Sources: Bloomberg, World Health Organization as of Dec. 10, 2020

4 Sources: Bloomberg, World Health Organization as of Dec. 10, 2020

5 Sources: Federal Reserve Economic Data, https://fred.stlouisfed.org, as of Dec. 10, 2020, Total Assets (Less Eliminations from Consolidation): Wednesday Level, Trillions of U.S. Dollars, Weekly, Not Seasonally Adjusted

6 https://www.bea.gov/news/glance

7 Sources: Bloomberg, University of Michigan, as of Dec. 10, 2020

8 Sources: Bloomberg, US Census Bureau as of Nov. 10, 2020

9 Source: Bloomberg, as of Dec. 10, 2020

10 Sources: Bloomberg, as of Nov. 10, 2020