| ||||||||||||

The United States has a brilliant, flawed, and wonderful election process. It is the best that exists (to my knowledge), even though it has more problems than I can count. It creates passion, confusion, broken promises, hopes, dreams … and, at the end, results in one person standing to oversee the country for the next four years.

Add on top of that a frenetic news cycle that is quite literally designed to grab attention, an information-dissemination process that is often biased and error prone, a (mostly) two-party system, and poof . . . there’s enough tinder there to catch any family dinner conversation on fire quite quickly.

Yet…does it matter?

In short, yes and no.

What follows is a data-driven exploration of four statements we hear frequently:

- Investors should avoid election years.

- Markets are always better when [insert party] get elected.

- One party spends, the other saves.

- One party borrows, the other doesn’t.

Let’s look closely at each.

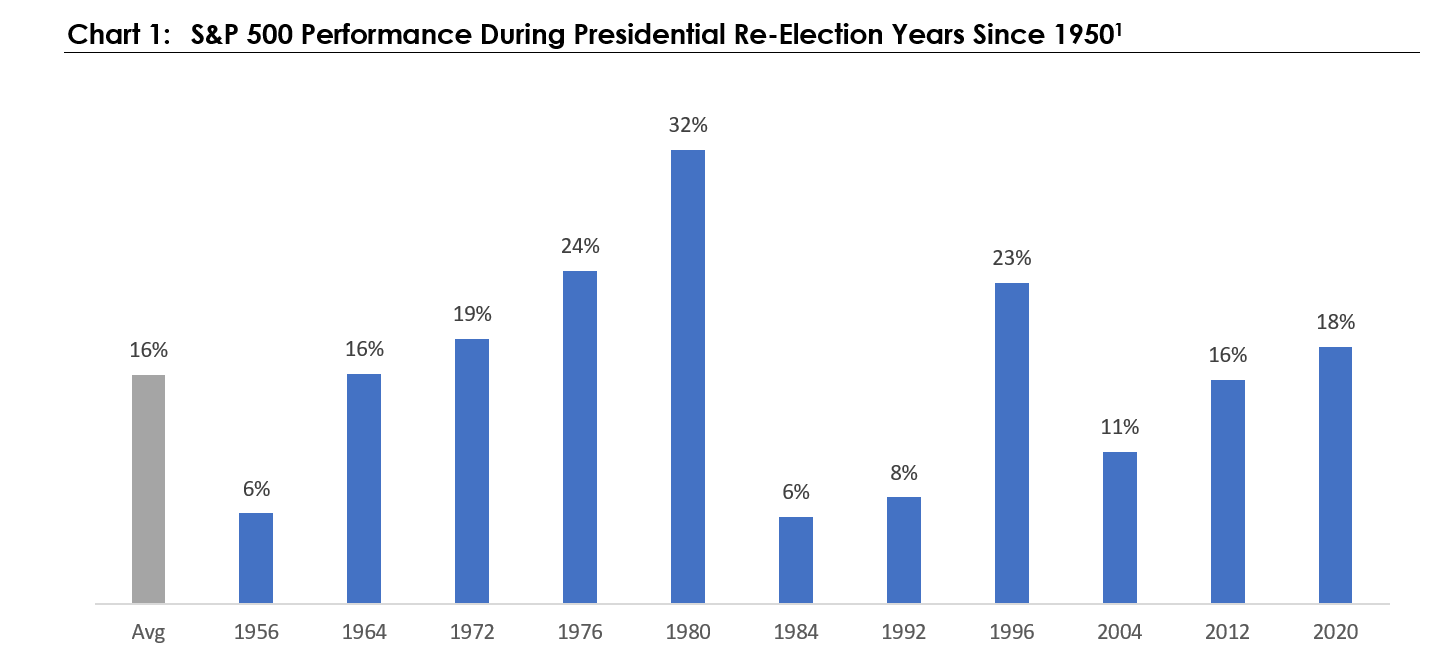

Fact or Fiction No. 1: Investors should avoid election years

Markets dislike uncertainty. Capital markets (and the underlying companies that drive them) benefit from understanding what is likely in the future and, as uncertainty rises (COVID for example), markets will tend to suffer. One could argue that not knowing the future leader of the largest economy in the world is enough uncertainty to make markets nervous.

As such, we simply looked back at the returns of election years when there was a possible re-election, and plotted those returns in the chart below:

Without digging too far into the details, two obvious elements emerge:

Does that mean this year will be the same? Of course not, but it’s at least enough to state that, historically, election years seem to be as good as any other years to maintain exposure to capital markets.

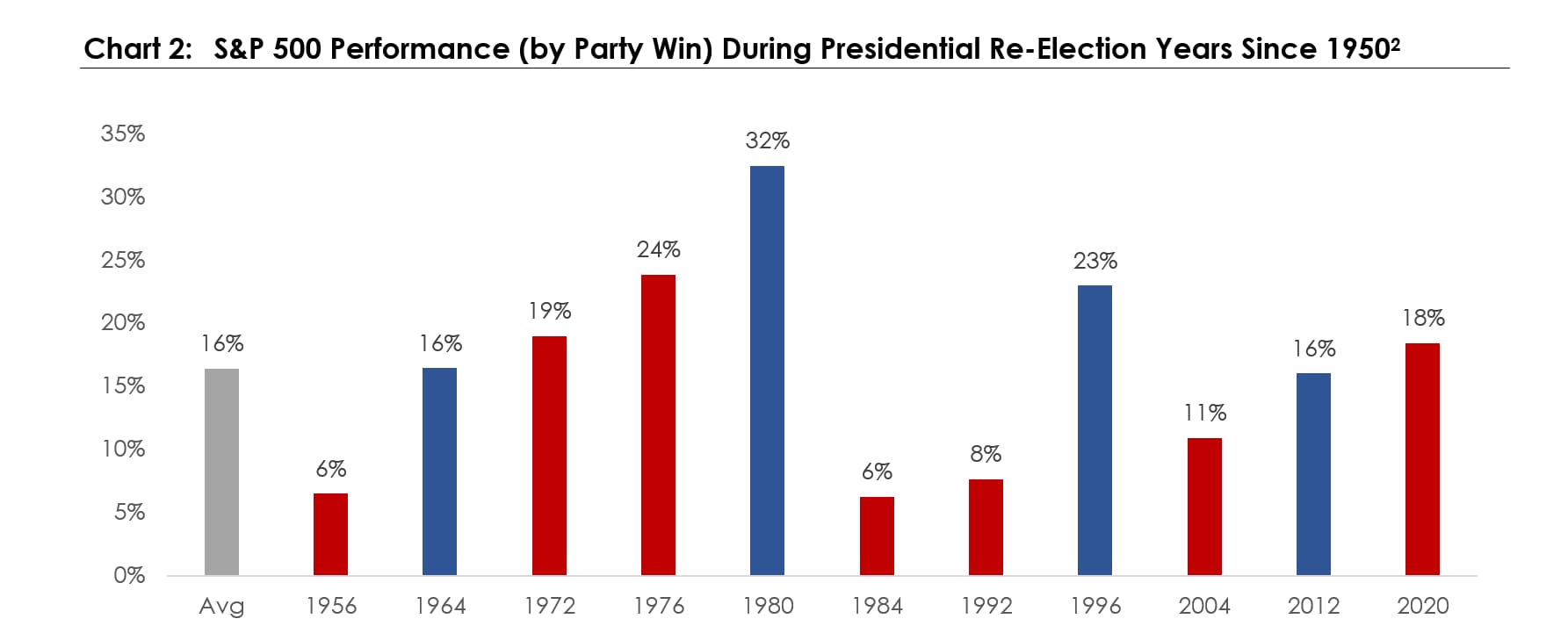

Fact or Fiction No. 2: Markets are always better when [insert party] get elected

This is a statement we hear from passionate members of both sides of the aisle, and both sides argue just as vehemently that their party provides better market returns. As the quip goes, this falls under the category of “frequently wrong, but never in doubt.”

Accordingly, we took the same data above (e.g., calendar year returns of the S&P 500) and simply looked at whether Republicans or Democrats were elected in those years.

First, there are only 11 data points, so none of this is statistically significant…but the result is the same: it didn’t really matter. The average returns when Republicans won was very similar to the average returns when Democrats won.

Said another way, there are so many variables in play (e.g., tax policy, power in Congress and/or Senate, inflation, war, pandemics, and the like) that whether the person holding the Presidential office is Republican or Democrat matters very little.

Which brings us to the third statement we hear quite often…

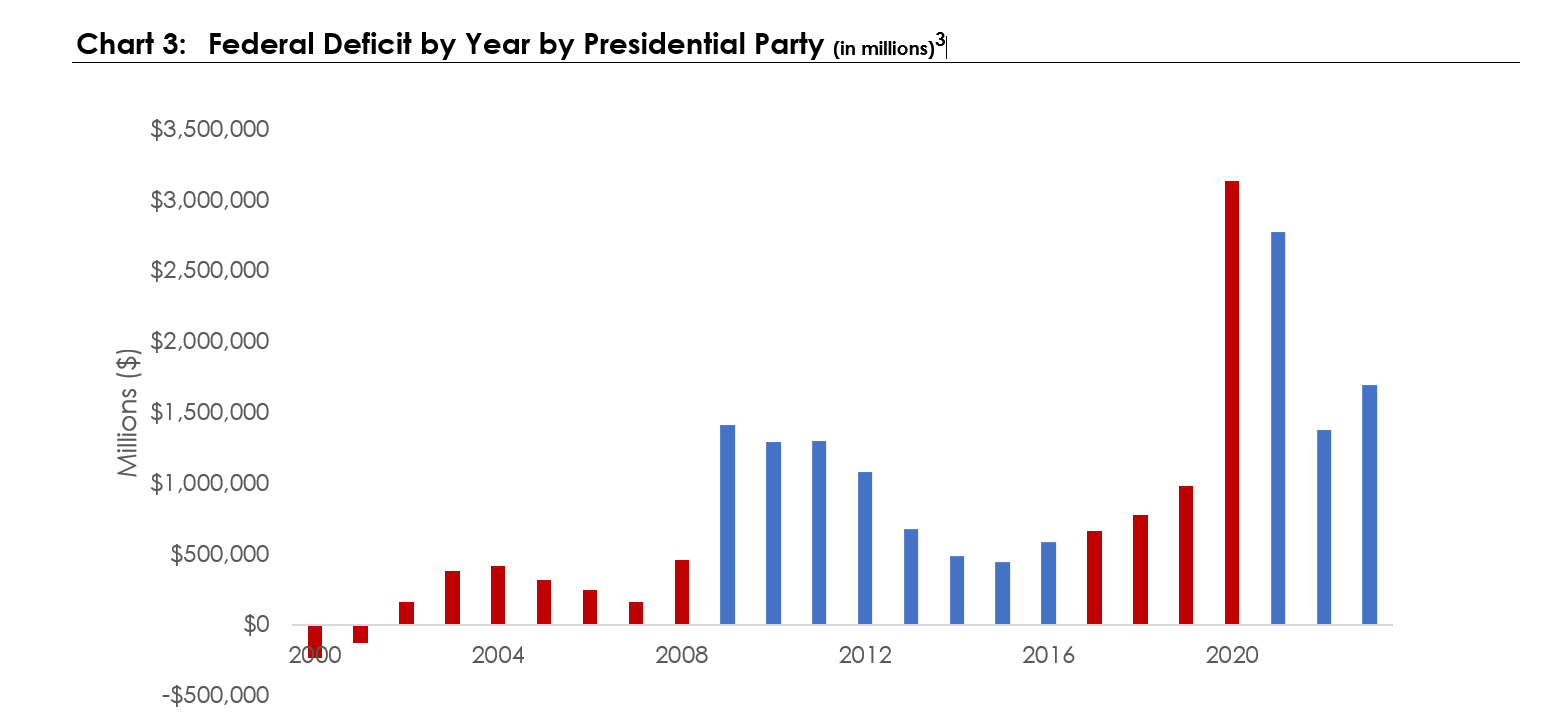

Fact or Fiction No. 3: One party spends, the other saves

Ahh, this is a fun one.

Ladies and gentlemen, before we explore the data, let me ask a question: What is the business model of the United States? Yes, it’s a bit obvious perhaps, and a bit strange, I’ll concede … but the business model of the United States is essentially exporting bonds and importing goods.

At the government level, we:

- Receive revenue in the form of taxes,

- Spend that revenue (and more) in the form of services (military, social services, roads, and the like)

- Finance that extra spending by borrowing money in the bond market.

That’s pretty much it.

Which brings me to Chart 3.

First, let me explain. This shows the United States federal deficit (e.g., how much we receive vs. how much we spend) by year in millions of dollars. So, for example, in 2009, we spent roughly $1.4 trillion more than we received. We then color code those years with red for Republicans and blue for Democrats.

What do we notice? Other than a very quick surplus in 2000, we run a deficit each year, one of similar magnitude regardless of which party sits in the Oval Office.

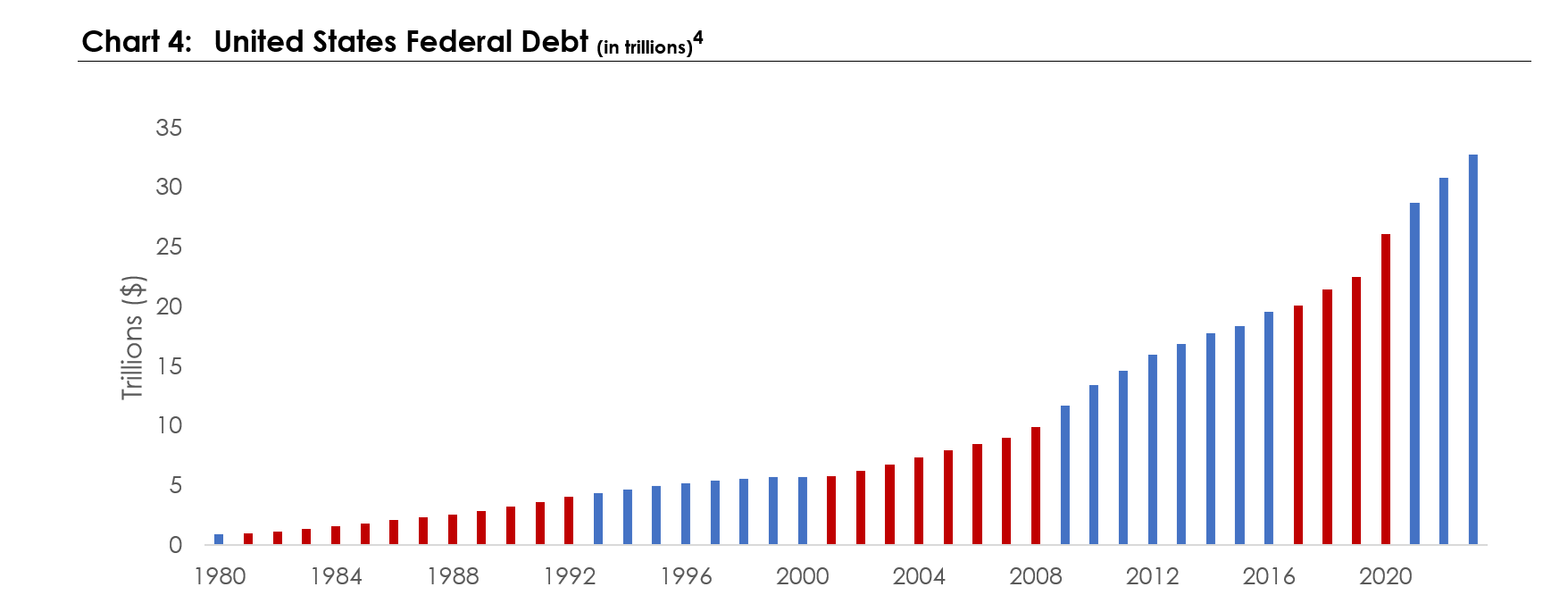

Fact or Fiction No. 4: One party borrows, the other doesn’t

Said another way, we, as a country, borrow money to finance our spending, and we’re pretty reliable on that approach.

Which brings us to our last chart.

So, if we borrow money every year … that, of course, then means the amount we are borrowing keeps climbing, and Chart 4 shows that picture (in trillions of dollars). This is the total amount of money we have borrowed and how quickly it continues to climb. We then color code those years (as we have in previous charts), and the storyline is pretty clear.

As a comparison, the entire U.S. economy (as measured by gross domestic product) is around $27 trillion; our total debt is now over $33 trillion.

Again, blurring our collective eyes (apparently my favorite mode of analysis) shows very little difference between how fast the debt grows when a Republican or Democrat is in the White House.

Conclusion

So, where does this all leave us?

Well, at a minimum, I draw the following conclusion:

The United States is a massive economy that is:

- Complex.

- Driven by incentives.

- Incredibly competitive.

No single person (particularly given the checks and balances of our political system) has much of an ability to change those dynamics, and they certainly don’t change our expectations for how capital markets will perform.

In short, focus on the long term and try to ignore the short term. Turn down the volume on your political news source of choice the next time scare-mongering begins and remember that there are generally larger, and more reliable, forces at play.

Discover more from MassMutual …

3 ways to financially prepare when elections loom

Markets: Inflation and the money supply

Markets: 2023 lessons for the coming year … in 5 charts

___________________________

1 Source: WMIT Research, Bloomberg

2 Source: WMIT Research, Bloomberg

3 Source: WMIT Research, Bloomberg, U.S. Treasury

4 Source: WMIT Research, U.S. Treasury, St. Louis Federal Reserve