| ||||||||||||

Well, that’s a wrap, folks. 2023 is officially over and done. The holly has crinkled, the Christmas trees have withered, and the menorahs have been lovingly wrapped and boxed for next year. And what a year it was … we set records on the upside, the downside, and the strange side (did you know the record for the most magic tricks ever completed under water was beaten in 2023?!).

It was a year of surprises, of tragedy, and of humanity. A year of growth, of failure, of greed, and of fear.

And yet, here we are again. Despite the gyrations and the travails, progress has been made, and we must take stock of where we are, and what we have experienced, so we can, with any luck, make better decisions about the future that we face (however uncertain that may be).

So, for today, we will try to accomplish two objectives:

1. Look back.

2. Look forward.

With that, let us begin…

Looking Back: Market surprises

A year of surprises is probably the most apt description for 2023. If, for example, you were to peruse the predictions of our Wall Street brethren at the end of 2022 for stock market performance, you would notice one very strong similarity: they were all categorically and completely wrong.

Most called for weak equity markets and a possible recession, but what we experienced was a very strong equity market and a reduced likelihood of recession.

We set a four-decade high for how expensive home affordability became, while also seeing three of the four largest bank bankruptcies in history.

Inflation fell, while unemployment remained remarkably low. Mortgage rates hit several decade highs, and student loan repayments resumed after a three-year hiatus.

In short, it was a year of unexpected changes, and yet, in many ways, similar to just about every other year in human history. What, you say?! But you just said…

Well, yes, but … and stay with me here … chaos and uncertainty are, in many ways, the human experience. At least from my vantage point, there has not been a single year that has been, or will be, not surprising. It is what makes investing so confusing in some ways and yet so simple in others. If we stare at the gyrations, particularly in the short term, they are impossible to predict, noisy, and in many ways, irrational. Yet if we zoom out and focus on the broad moves … particularly those that are driven by incentives … investing becomes relatively straightforward.

As the primary example, let us turn to the stock market performance in 2023.

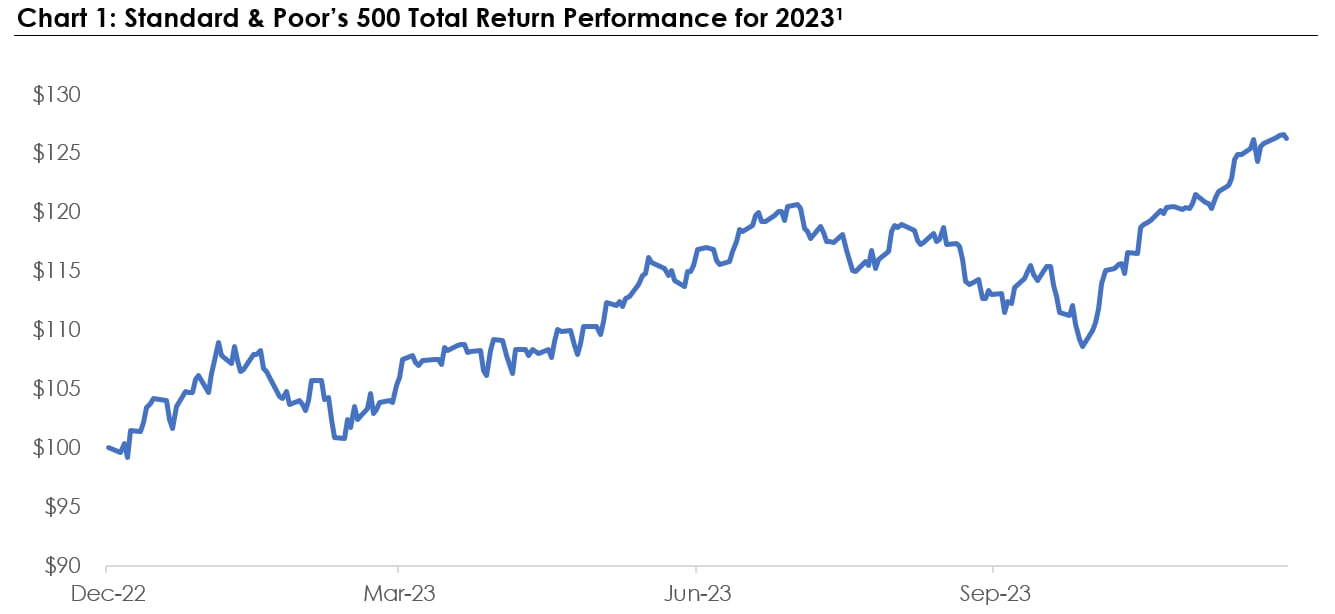

If you had started with $100 on Dec. 31, 2022, and invested solely in the S&P 500, you would have had nearly $127 by the end of 2023. Strong performance indeed. While attribution is always difficult, markets clearly benefited from inflation expectations falling, which resulted in the cost of money falling as well. As we have discussed ad nauseum, the massive spike in inflation in 2021 and 2022 was largely self-inflicted and, as policy makers began to reverse course, inflation followed suit.

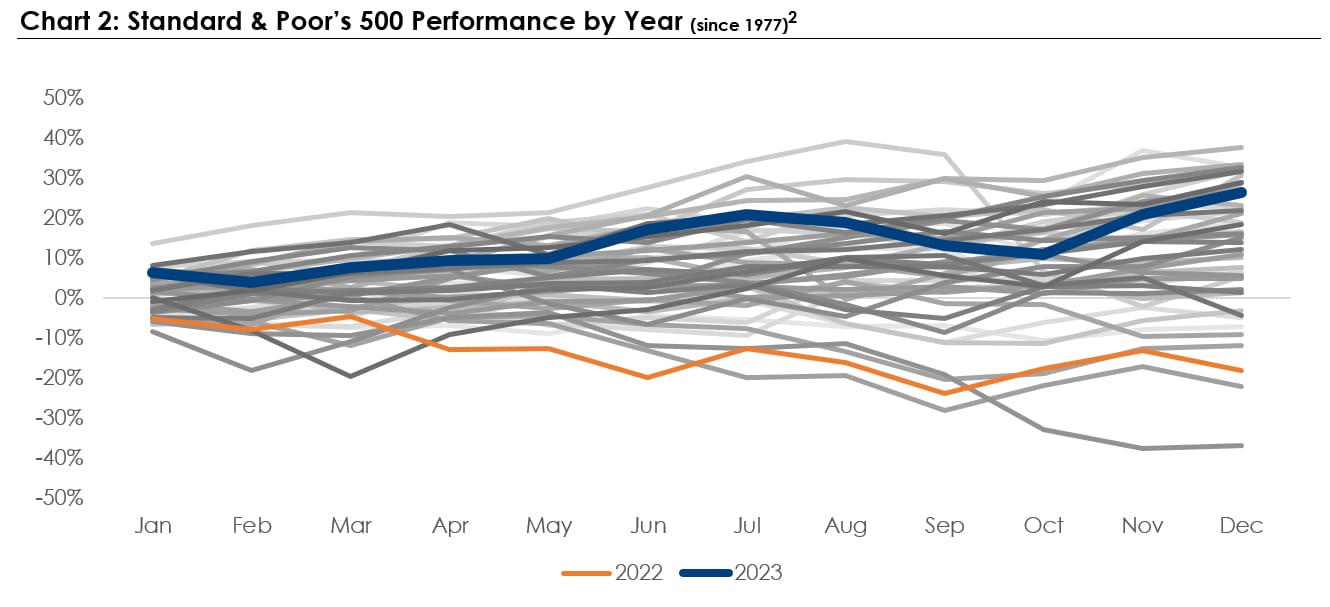

For historical context, we turn to Chart 2.

This chart takes every single year (beginning with 1977) and puts them on the same chart so we can compare how strong 2023 was (the blue line), and how challenging 2022 was (the orange line). 2023 was certainly near the top of the past 50 years, although not extraordinary in any sense.

This chart takes every single year (beginning with 1977) and puts them on the same chart so we can compare how strong 2023 was (the blue line), and how challenging 2022 was (the orange line). 2023 was certainly near the top of the past 50 years, although not extraordinary in any sense.

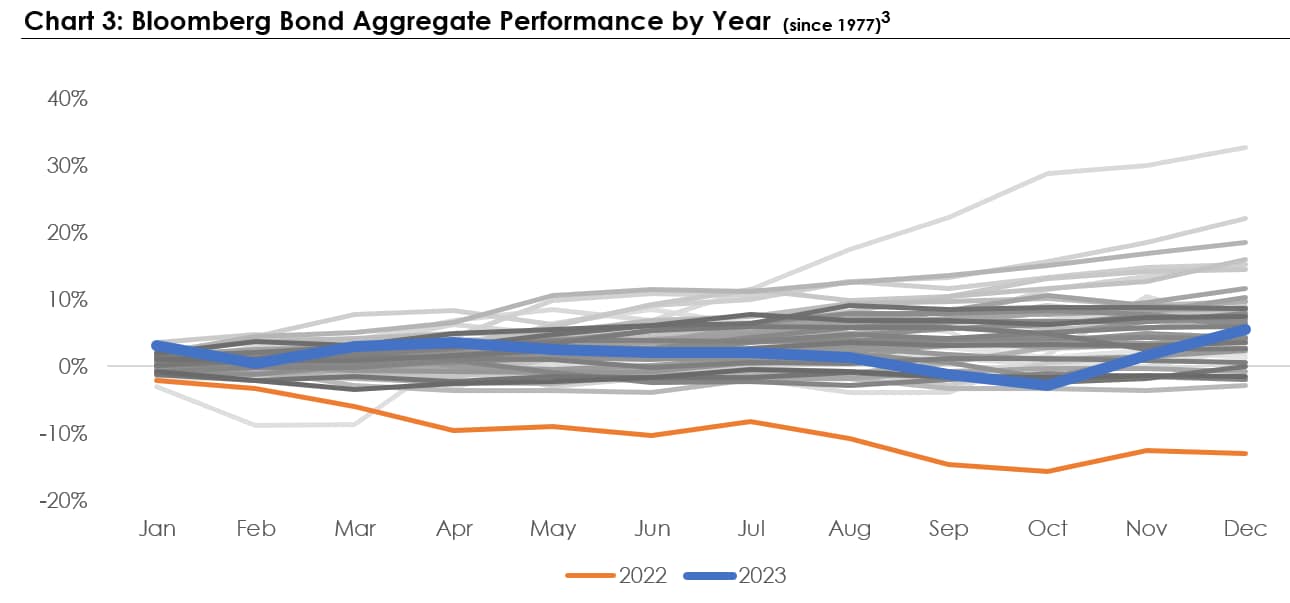

In short, 2022 (orange line) was a terrible year for bonds, while 2023 (blue line) was modestly positive.

So, one might ask, therefore what? Does it matter? Should we do anything differently now that we have the historical context for what happened in 2023?

First, let’s take stock of what happened in this latest cycle:

- An unexpected event (COVID) occurred that caused the U.S. consumer to stop spending and U.S. businesses to receive far less revenue. This slowed the economy and pushed the United States (and many other countries) into a recession.

- The government (particularly the Federal Reserve and the U.S. Treasury) created unprecedented amounts of stimulus that strongly: a) encouraged spending, and b) encouraged borrowing.

- At the same time, three major influences converged: a) supply chains were disrupted worldwide, b) demand increased (momentarily) as U.S. consumers began to spend and borrow due to large levels of cash, and c) the value of our dollars had declined as the U.S. government essentially created many more of them.

- Therefore, inflation increased quickly as the prices of goods went higher, while the value of our dollars went lower.

- Because inflation causes uncertainty, the U.S. government (primarily the Federal Reserve) then reversed course, and quickly began removing liquidity through its various means (raising rates being one of them).

- Higher rates discouraged spending and borrowing and, therefore, put downward pressure on prices…thus slowing, and eventually reversing, the increase in prices.

Which leads us to today: inflation is now back to more reasonable levels, unemployment is still very low, the U.S. economy is still growing at a reasonable clip, and both stock and bond markets had a good year.

Looking forward

Does that mean there is no risk? Does that mean markets are going down? Does that mean markets are going up?

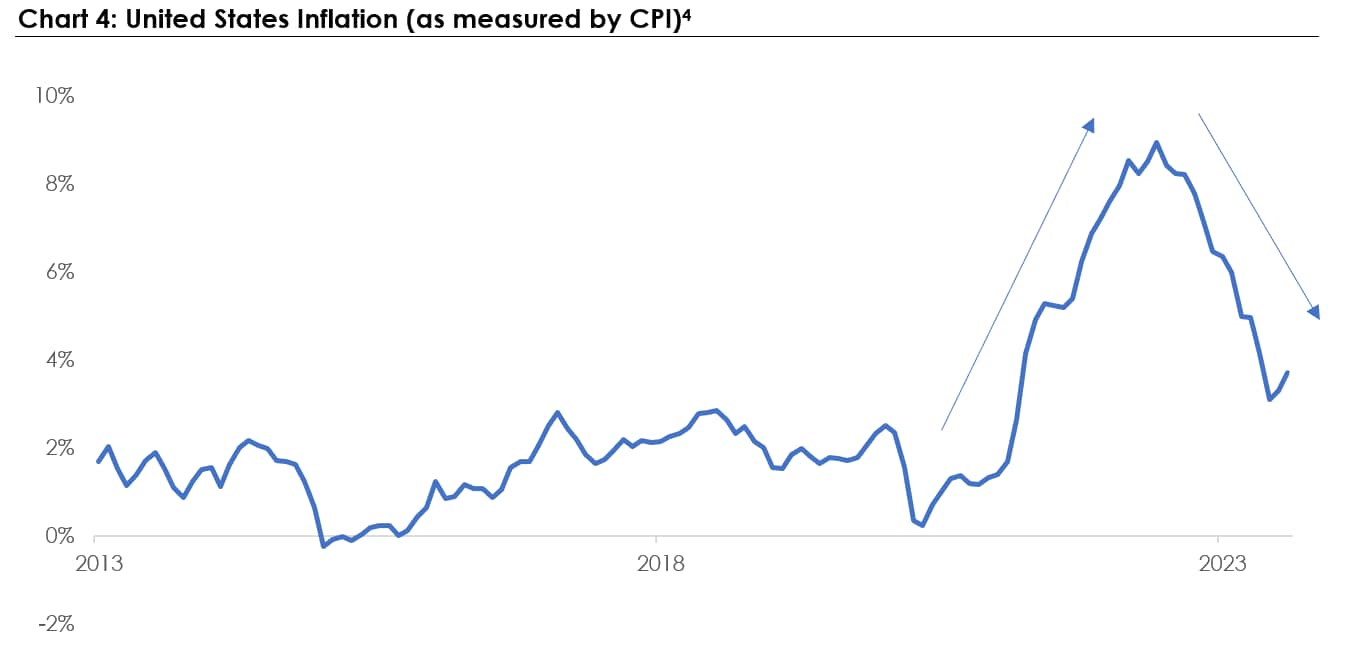

Again, let us turn to history … and Chart 4 helps us tell that story.

The chart above is essentially a tale of two stories:

- Inflation went up and heavily influenced spending (including capital investing) and borrowing.

- Inflation has now come down and will likely remain stubbornly above its historic range for a bit.

This inflation turnaround has come from the Fed raising rates very aggressively, and, at least as of right now, has resulted in inflation no longer being the sole topic du jour.

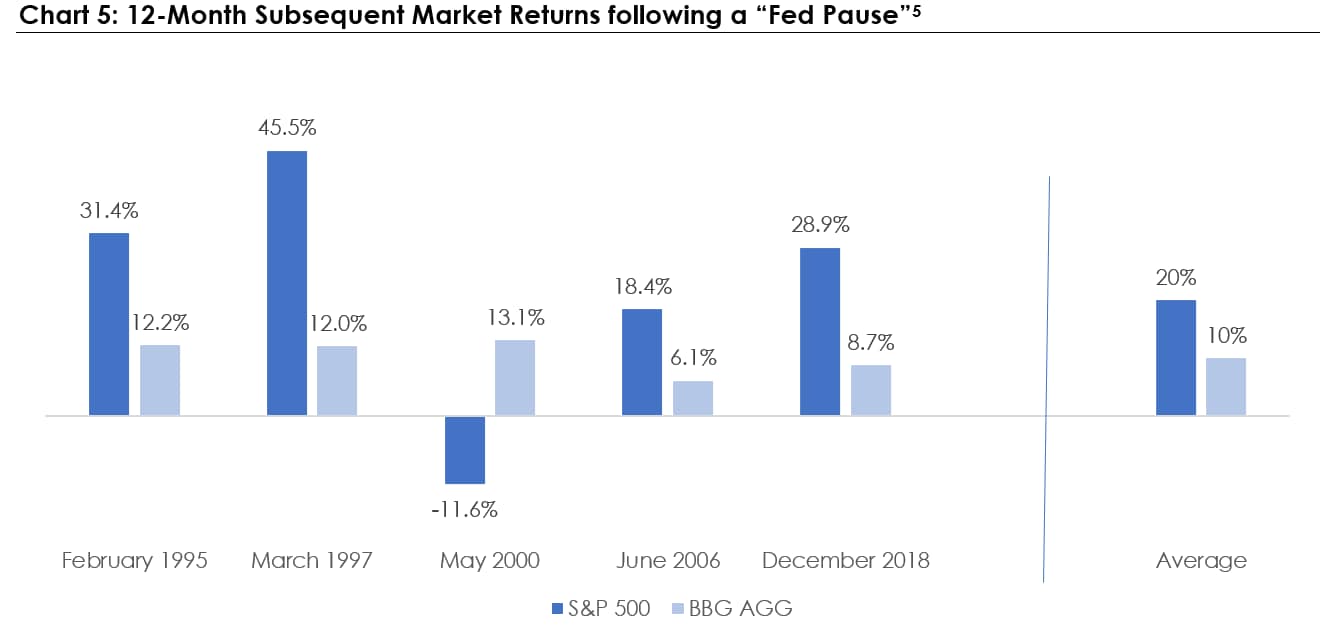

Which raises an important question: what has happened historically when the Fed paused raising rates?

We look again, to history, to provide perspective in Chart 5.

Let me explain. Over the past 30 years, there have been five instances where the Federal Reserve had been raising rates and paused. We then calculated the 12-month returns following each of those rate pauses, plotted them accordingly, and then averaged those returns.

While each situation was different among nearly every dimension imaginable, there was some consistency in that markets tended to be higher following those pauses. To make this clearer, following the pause in February 1995, for example, the S&P 500 was up 31.4 percent over the subsequent 12 months and bonds performed similarly strongly. We saw similar trends for subsequent three-year and five-year returns as well.

And yet, as my dear readers know, never trust a chart without understanding the concept first.

How could this be?

While attribution is always difficult, one plausible explanation is that a pause in raising rates changes the future expectations of borrowing and the cost of capital. If you run a factory, for example, and need to borrow capital to expand, the cost of borrowing will strongly influence your decision on when, and if, to expand that factory. If banks believe rates will continue to rise, they will likely charge you more than if banks believe rates will likely fall.

Said another way, when the Fed pauses raising rates, it is signaling that the inflation pressures have begun to abate, which essentially decreases the likelihood of raising rates and increases the likelihood of lowering rates. This is oftentimes enough to, at the margin, decrease rates and begin the stimulative cycle once again.

Aha, you say – so the market is definitely going up?! Well, not necessarily…and this is the key.

The market is influenced by an inordinate number of variables, many of which are changed the minute they are observed. If we pull on one string to create one perspective, we can think of 10 more threads to pull on that create equally thoughtful perspectives, and, as we have seen over and over again, predicting or conceptualizing how those perspectives aggregate up to an accurate market forecast is, well, futile.

Yet what we CAN do well is to understand that capital markets are simply reflections of capitalism, and capitalism, while not perfect, is driven by incentives. If we understand the incentives, candidly … investing becomes much more straightforward and leads to some fairly obvious conclusions: the primary amongst them is to simply get the big things right.

The power of compounding is so great thatinvesting well often just requires staying in the market while avoiding poor behavioral decisions and minimizing unnecessary costs and taxes. 2023 was a great example of the market rewarding those who remained invested (despite the challenges of 2022), while those that sold at the end of 2022 unfortunately did not receive the same benefits.

In closing, try as much as possible to ignore the short-term zigs and zags. Focus on the long term, try and remain invested, have a plan in place…and above all, try and stick to that plan.

Discover more from MassMutual …

Markets and perspective: Lessons from the past

When markets dive, keep your strategic calm

Need a financial professional? Find one here

____________________________________

1 Source: St. Louis Federal Reserve (FRED), WMIT Research

2 Source: Bloomberg, WMIT Research; as of December 31, 2023

3 Source: Bloomberg, WMIT Research, as of December 31, 2023

4 Source: St. Louis Federal Reserve (FRED), WMIT Research, as of Jan. 15, 2024

5 Source: Bloomberg, WMIT Research, as of Jan. 15, 2024