| ||||||||||||

You seek investment growth but take steps to manage risk. Your portfolio is well-diversified. And you rarely engage in active trading.

You are a moderate investor.

Identifying your investor profile — be it conservative, moderate, or aggressive — is an important step in helping you craft an asset allocation that aligns with your financial objectives, tolerance for risk, and time horizon to retirement.

Note that your portfolio preferences may straddle the line between two profiles as you assume either more or less risk depending on your goals. Your investor profile isn’t static either. It will likely change over time, in some cases becoming more conservative as you approach retirement.

“Understanding your investor profile or risk profile is crucial,” said Armando Sallavanti, a Certified Financial Planner™ professional with MassMutual Greater Philadelphia. “It’s the foundation of your financial strategy. Your risk profile dictates how much volatility you can stomach, which directly impacts your asset allocation. Think of it as knowing your speed limit before hitting the highway — it keeps you from driving too fast or too slow.”

With that, let’s look closer at what it means to be a moderate investor.

The goal of a moderate investor

The primary goal of a moderate investment strategy is capital appreciation, but income generation may also be a priority.

Moderate investors typically maintain a diversified asset allocation that consists of both stocks and bonds. A diversified portfolio may not outperform the broader stock market, but should at least aim to outperform inflation, said Sallavanti.

A financial professional can provide personalized insights that may help you determine if a moderate asset allocation is right for you.

“I am a firm believer that there is no such thing as a one-size-fits-all investment strategy,” said Dan Drabinski, a financial professional with Bluecrest Wealth Management in Dallas, Texas. “Rather, the most appropriate investment style for you is the one which allows you to accomplish your goals without sacrificing additional risks.” Related: Why a balanced asset allocation isn’t one and done)

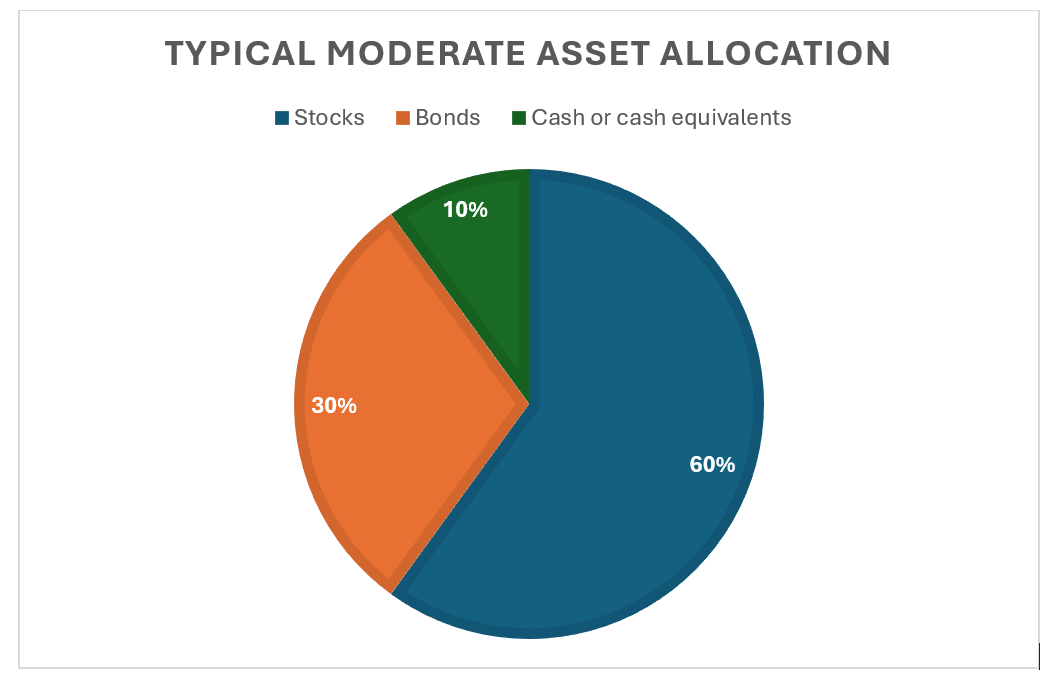

Typical asset allocation for a moderate investment portfolio

A moderate asset allocation is typically weighted more heavily toward stocks and mutual funds than to bonds or cash. Historically, stocks have offered greater upside potential in exchange for higher risk.

Always remember, however, that past performance is never a guarantee of future returns.

A balanced investor may have anywhere from 50 to 60 percent of their portfolio allocated to stocks, and from 50 to 40 percent earmarked for bonds (fixed income) and cash or cash equivalents, such as money market funds and certificates of deposit.

Based on MassMutual’s independent research, a typical moderate asset allocation might look like this:

The stocks within a moderate portfolio may include a diversified mix of securities that could potentially help to stabilize long-term returns, including:

- Large-capitalization stocks -- from larger, more established publicly held companies.

- Mid-capitalization stocks — from medium-sized publicly held companies with a market valuation that falls between large-cap and small-cap stocks. Historically, small-cap stocks have been more volatile than large-cap and mid-cap stocks, although past performance does not guarantee future returns.

- Index funds — a mutual fund or exchange-traded fund that seeks to mimic the performance of a specific market benchmark, such as the S&P 500 Index.

- Domestic stocks — from publicly held companies that are based within the U.S.

- International stocks — from publicly held companies that are based outside the U.S.

- Defensive stocks — from sectors that have, in some cases, performed better (or lost less) during periods of economic decline. Those may include utilities, consumer staples, and health care.

Because you seek more stability than an aggressive investor, your fixed income allocation may also include a blend of:

- Treasurys — bonds issued and backed by the U.S. Department of Treasury with differing maturity dates.

- Investment-grade corporate bonds — considered by some credit rating agencies to be higher quality because their risk of default may be lower. (Calculator: How much should I save for retirement?)

Past performance of a typical moderate investment portfolio

Your asset allocation will determine your rate of return.

According to data provided to MassMutual by market research firm Morningstar Direct, the average annual total return for Morningstar’s moderate asset allocation was 7.59 percent between 2003 and 2023.

During that period, the best-performing year (2009) was 24.13 percent, and the worst-performing year (2008) saw a loss of 28 percent.

Note that Morningstar Direct’s moderate allocation data is based on the constituent U.S. mutual funds in that category. As such, the performance data may differ from the returns and losses that would be generated by MassMutual’s typical moderate asset allocation. (Learn more: Understanding asset allocation and diversification)

Which investors are most likely be moderate?

A moderate investment strategy may be appropriate for middle-age investors who require growth to reach their retirement savings goals and have the time horizon to ride out market downturns.

Moderate investors must be comfortable with a reasonable degree of risk in the pursuit of building wealth. But many opt for more passive investments in their retirement plan, such as target date funds that automatically become more conservative as they age.

“This risk profile is ideal for investors seeking a balance between growth and risk,” said Sallavanti. “This includes middle-aged investors or those with a medium-term horizon to retirement who wish to grow their portfolio while managing volatility.” (Learn more: The three keys to choosing your investments)

Older investors and retirees may also opt for a balanced asset allocation to continue building wealth and preserve purchasing power in the face of inflation, especially if they are concerned about outliving their savings. Protection products that provide a guaranteed income stream, including certain annuities, could potentially help reduce longevity risk.

Some financial professionals recommend that retired investors with exposure to market risk maintain at least a year’s worth of cash reserves from which to draw during periods of market decline, giving their investments time to recover.

“A variety of factors come into play when contemplating investment style,” said Drabinski. “Learning to visualize a retirement lifestyle helps make saving easier.”

Armed with insight about the core objectives, average returns, and potential volatility of a moderate investor profile, you may be positioned to make better choices about the type of investment strategy that might be right for you. But you need not go it alone. A trusted financial professional can offer valuable guidance that may help you reach your goals.

Discover more from MassMutual…

Understanding the basics of investing

Three keys to choosing your investments

Need a financial professional? Find one here

_________________________