| ||||||||||||

You’re on a mission to build wealth. You’re willing to accept higher risk for higher potential returns. And you don’t let market volatility slow you down.

You are an aggressive investor.

Identifying your investor profile — be it conservative, moderate, or aggressive — is an important step in helping you craft an asset allocation that aligns with your financial objectives, tolerance for risk, and time horizon to retirement.

Note that your portfolio preferences may straddle the line between two profiles as you assume either more or less risk depending on your goals. Your investor profile isn’t static either. It will likely change over time, in some cases becoming more conservative as you approach retirement.

“Understanding your investor profile or risk profile is crucial,” said Armando Sallavanti, a CERTIFIED FINANCIAL PLANNER™ with MassMutual Greater Philadelphia. “It’s the foundation of your financial strategy. Your risk profile dictates how much volatility you can stomach, which directly impacts your asset allocation. Think of it as knowing your speed limit before hitting the highway — it keeps you from driving too fast or too slow.”

With that, let’s look closer at what it means to be an aggressive investor.

The goal of an aggressive investor

As an aggressive investor, your primary goal is to maximize returns. Generating an income stream from your portfolio is generally a low priority.

Using active trading, tactical investment strategies, and analyst insights, you are likely aiming to outperform both the broader market and your buy-and-hold (passive) investor peers.

As such, your portfolio will likely be dominated by stocks, which historically have offered higher reward potential in exchange for higher risk. Although past performance is no guarantee of future returns. (Related: Why a balanced asset allocation isn’t one and done)

A financial professional can provide personalized insights that may help you determine if an aggressive asset allocation is right for you.

“I am a firm believer that there is no such thing as a one-size-fits-all investment strategy,” said Dan Drabinski, a financial professional with Bluecrest Wealth Management in Dallas, Texas. “Rather, the most appropriate investment style for you is the one which allows you to accomplish your goals without sacrificing additional risks.”

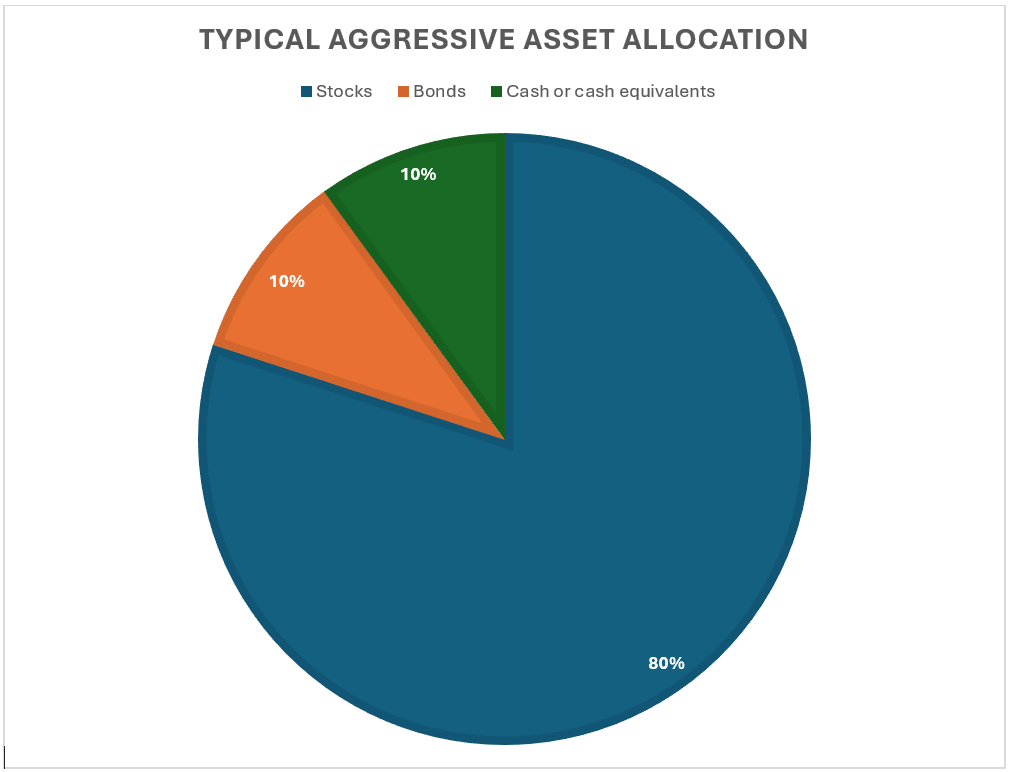

Typical asset allocation for an aggressive investment portfolio

An aggressive investment strategy can take many forms.

A portfolio that consists of 80 percent stocks or more is generally considered to be aggressive. But that may include a diversified mix of professionally managed mutual funds or even low-cost exchange-traded funds that track a market index, such as the S&P 500 index for large capitalization stocks or the Russell 2000 Index for small-cap stocks.

“Regardless of investment strategy, diversification is key,” said Sallavanti. “Spread your investments across different asset classes to balance risk and reward.” (Calculator: How much should I save for retirement?)

Based on MassMutual’s independent research, a typical aggressive investment portfolio might be allocated like this:

Depending on their unique goals and appetite for risk, as an aggressive investor might favor:

- Growth stocks — that are expected to outperform the market average.

- Value stocks — that appear to be trading for less than they are worth based on fundamentals.

- High-yield investments — typically, corporate bonds that offer higher interest rates because they come with a higher risk of default.

Additionally, investors on the highest end of the risk spectrum might opt for a combination of stocks, mutual funds, and alternative investments, including:

- Real estate

- Commodities

- Venture capital

- Hedge funds

- Derivatives (futures and options contracts)

Alternative investments can potentially help improve diversification because they tend to have a lower correlation with traditional asset classes, meaning their performance does not necessarily move in lockstep with stocks and bonds. But they may also be less liquid and lack price transparency, which may equate to higher risk. Before adding alternative investments to your portfolio mix, it is wise to consult a financial professional who can help highlight the pros and cons.

Past performance of a typical aggressive investment portfolio

Your asset allocation will determine your rate of return.

According to data provided to MassMutual by market research firm Morningstar Direct, the average annual total return for Morningstar’s aggressive asset allocation was 9.77 percent between 2003 and 2023.

During that time, the best performing year (in 2003) was a return of 30.32 percent, and the worst performing year (2008) was a loss of 38.64 percent. (Learn more: Understanding asset allocation and diversification)

Note that Morningstar Direct’s aggressive allocation data is based on the constituent U.S. mutual funds in that category. As such, the performance data may differ from the returns and losses that would be generated by MassMutual’s typical aggressive asset allocation.

Due to the volatility you may experience with an aggressive portfolio, you may find it necessary to rebalance your asset allocation more frequently to bring your target allocation back in line. That can lead to higher fees that might eat into your investment returns.

Taxes may also reduce your returns, especially for aggressive investors who trade frequently. Financial professionals caution that certain investments may carry tax advantages or disadvantages. A tax professional can help you make informed investment decisions.

Which investors are most likely be aggressive?

Investors with an aggressive asset allocation are typically younger or middle-aged — those with a longer time horizon until retirement and a bigger appetite for risk.

Investors of any age with ample assets may also feel comfortable taking above-average risk to reach for growth.

“No two investors are the same, and thus no two plans are exactly the same,” said Drabinski. “An investor with a substantial net worth and minimal lifestyle expenses can afford to take excess risk, particularly if they have already addressed their basic lifestyle expenses.”

In general, he said, the larger the pool of assets you have, the greater the risk you can assume.

“However, retirement income goals and special expenses are often the biggest driver of your ability to take on risk,” said Drabinski. “Determining the trade-offs you are willing to make during retirement often dictates the amount of risk you can take leading up to retirement.”

Armed with insight about the core objectives, average returns, and potential volatility of an aggressive investor profile, you may be positioned to make better choices about the type of investment strategy that is right for you. But you need not go it alone. A trusted financial professional can offer valuable guidance that may help you reach your goals.

Discover more from MassMutual…

Understanding the basics of investing

Three keys to choosing your investments

Need a financial professional? Find one here

________________________________________