After rising for seven straight months, U.S. equities suffered a “September swoon” as the S&P 500 declined 4.8 percent during the month. The positive sentiment governing much of 2021 that was driven by easy financial conditions, strong earnings growth, resilient profit margins, and pent-up demand was dented by concerns of peak growth, COVID variants, tighter monetary and fiscal policy, and unrelenting price pressures. Chinese property developer Evergrande’s debt debacle dominated headlines but has remained a contained event so far.

The Federal Reserve is inching towards less accommodative policy by likely reducing its monthly asset purchases in the fourth quarter, leading to a rise in Treasury yields. Congress has kept us all on our toes as the debt ceiling deadline approaches, and gridlock within the Democratic party is making the passage of an infrastructure and broader spending bill a real challenge. As we approach the two-year anniversary of the COVID-19 outbreak, we are still experiencing its fallout and its far-reaching impacts on supply chains, consumer behavior, and labor markets. Looking to the remainder of 2021 and into 2022, such COVID disruptions will likely remain with us in some form, continuing to create a challenging environment for both investors and policymakers.

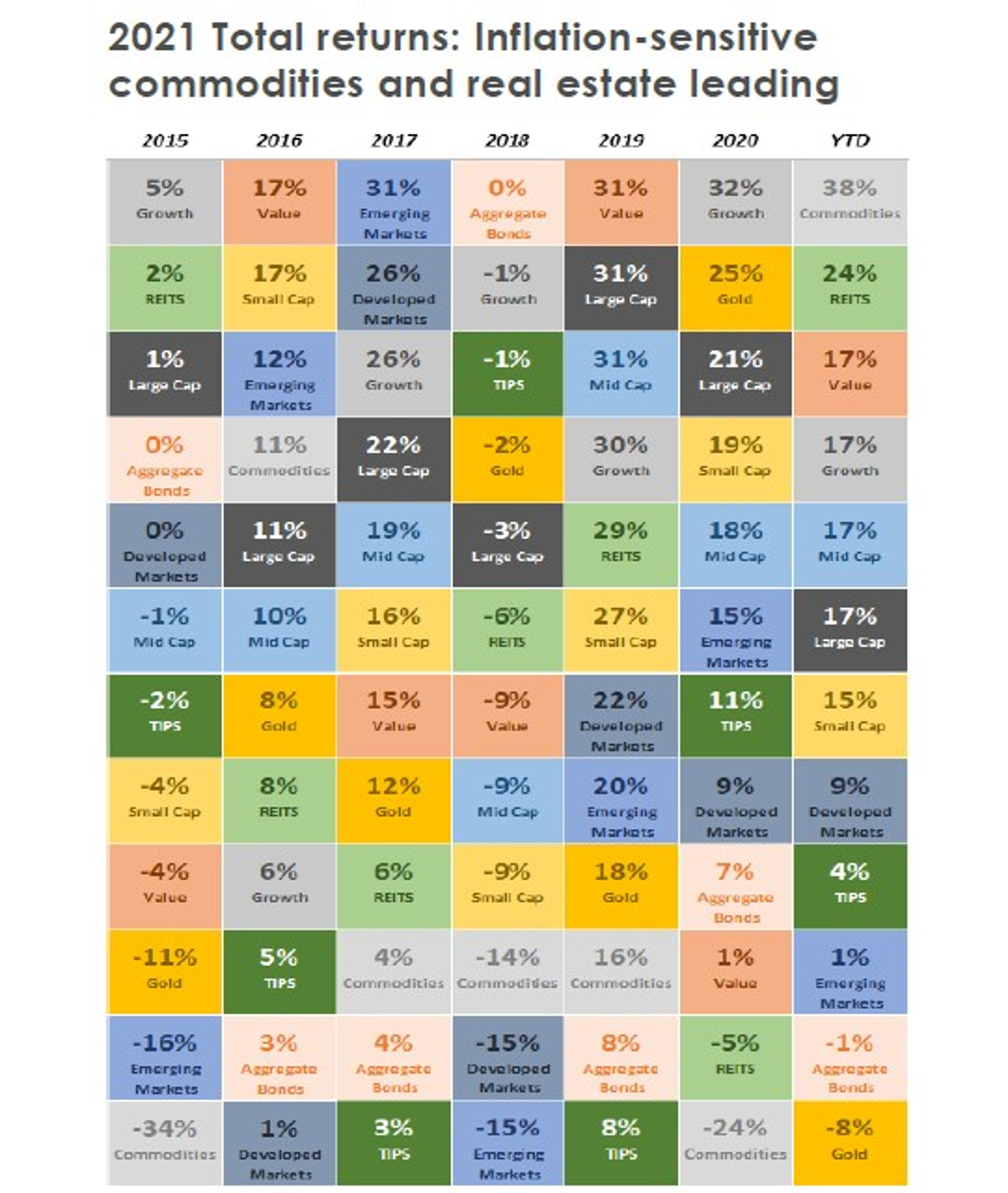

Source: Source: Cornerstone Macro as of Sept. 30 20211

U.S. economic recovery continues despite Delta disruption

After growing at a rapid 6.7 percent pace in the second quarter, the U.S. economy hit a speed bump in the third quarter as spread of the COVID-19 Delta variant led to renewed restrictions and consumer caution. Third quarter U.S. GDP growth is expected to moderate to 5 percent, down from expectations for growth of 7 percent earlier in the summer. Much of this economic growth is due to unsustainable deficit-financed government spending. The good news is that the recent Delta wave appears to have peaked, but like last year, there could be a seasonal spike in cases as the weather cools.

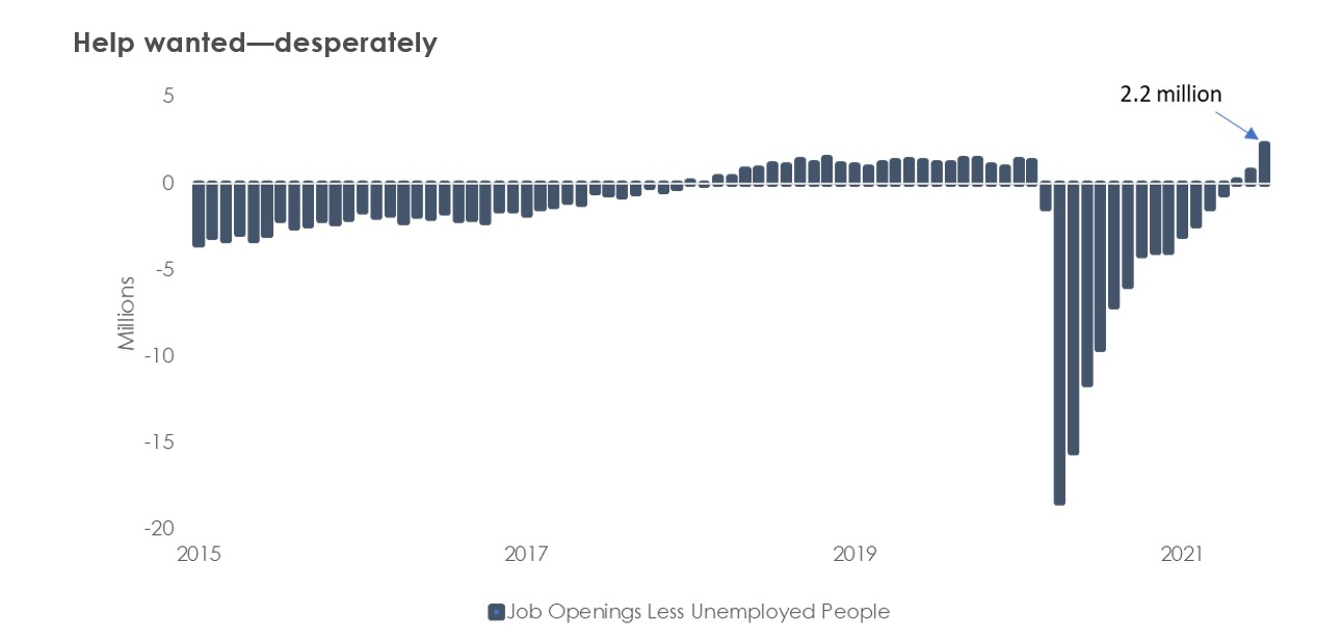

Although U.S. GDP has surged past pre-pandemic levels, employment growth has lagged. Total employment is still over five million jobs short of its pre-COVID peak, and August payroll numbers were disappointing. Labor force participation remains depressed, and the gap between job openings and unemployed people is at its widest level in decades with two million more job openings than there are unemployed people looking for jobs. There have been many factors at play here beyond enhanced unemployment benefits, but the bottom line is that the supply of labor is tight. With many individuals retiring and COVID creating permanent dislocations in the economy, it may be several years until we return to pre-COVID levels of labor force participation and employment.

Supply chain disruptions persist; commodity prices spike

Worker shortages and renewed lockdowns in Asia due to COVID outbreaks have exacerbated supply chain bottlenecks, which are persisting much longer than anticipated. Companies from FedEx to DR Horton continue to cite headwinds from supply constraints and have warned of higher prices due to input cost pressures. Transitory or not, companies and especially consumers are feeling the impacts of inflation. Unfortunately, the cure for higher prices is higher prices.

Although the U.S. CPI moderated in August due to volatile categories such as used car prices easing, it remains near multi-year highs, and other categories such as rents are accelerating. A Zillow index based on the mean of listed rents rose 11.5 percent in August from a year earlier with certain regions seeing rent increases of more than 25 percent. Turning to commodity markets, natural gas and oil prices are also on the rise, with the former spiking at an alarming pace and doubling since the beginning of the year due to supply constraints.

Source: Bloomberg as of Sept. 30, 2021

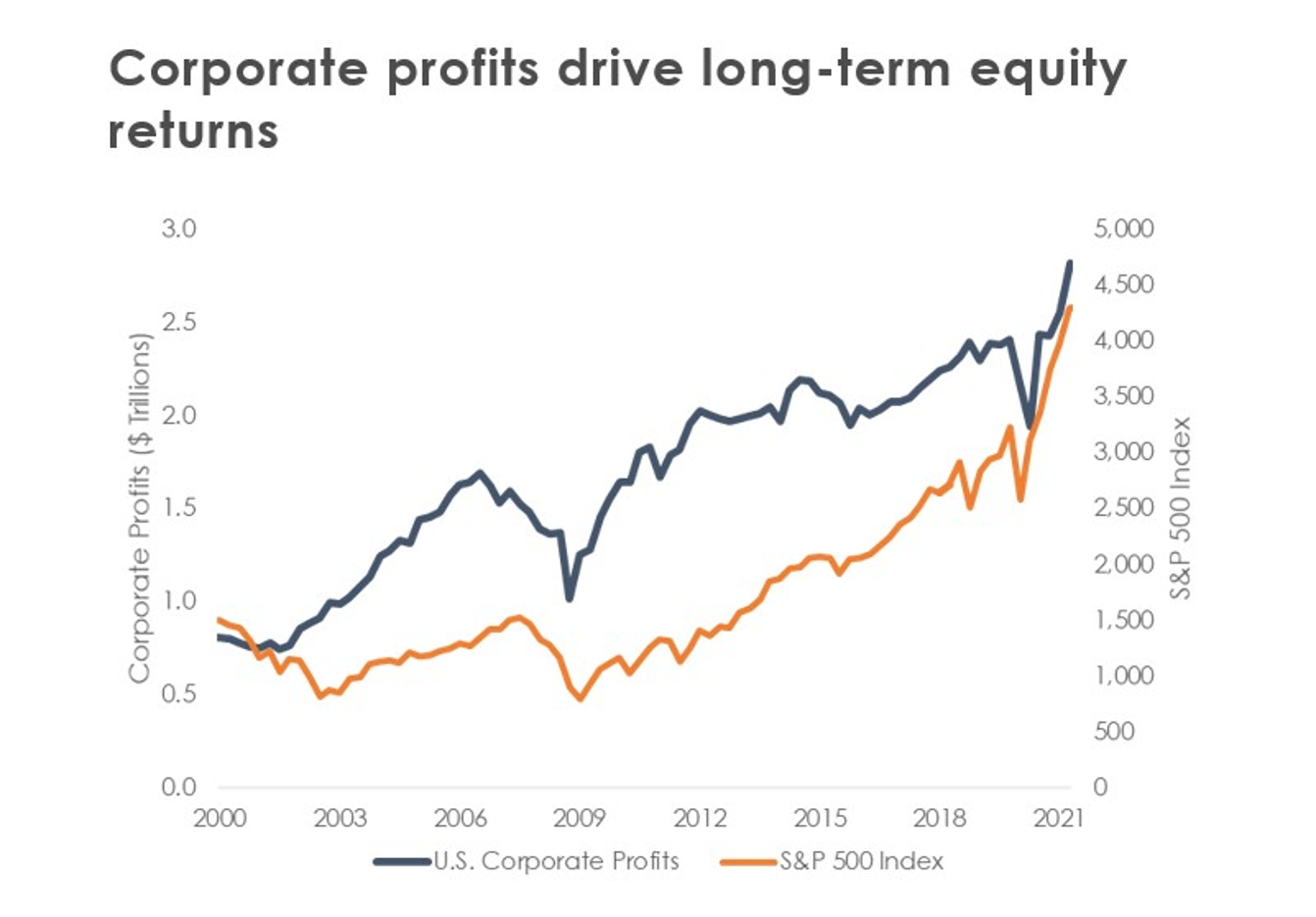

Corporate profit growth peaked in the second quarter

S&P 500 second quarter earnings per share grew at nearly 90 percent over last year, driving equity market momentum throughout the summer. Companies have impressively been able to achieve record high margins despite rising input and labor costs. Equity market returns continue to be driven by interest rates and earnings. A rapid rise in the former led to higher equity market volatility in September. We remind investors that the pace of and reason for rising interest rates is important. Equity markets generally perform well in environments where interest rates are steadily rising due to improved economic growth expectations. Less ideal for equities are environments where interest rates rise rapidly and are rising due to increased inflation expectations or restrictive monetary policy.

Source: Bloomberg as of June 30, 2021

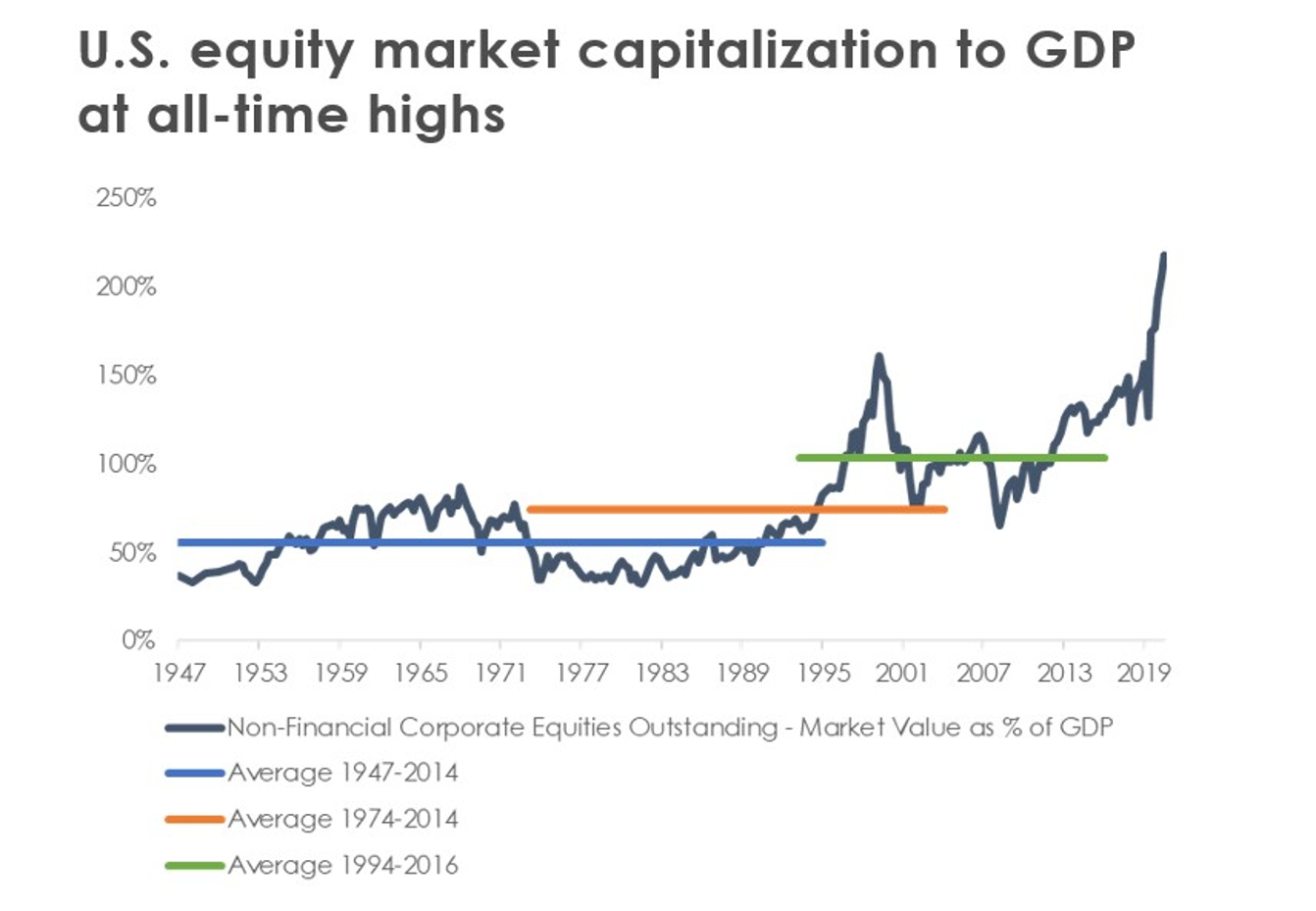

On the earnings front, S&P 500 earnings per share are expected to grow over 40 percent in 2021; however, consensus expects earnings growth to decelerate to 10 percent in 2022. With valuations at record highs, interest rates rising, and earnings growth moderating, 2022 equity returns may not be as strong as those generated in 2020 or 2021. In this environment, we expect companies with pricing power and above-average earnings growth to outperform.

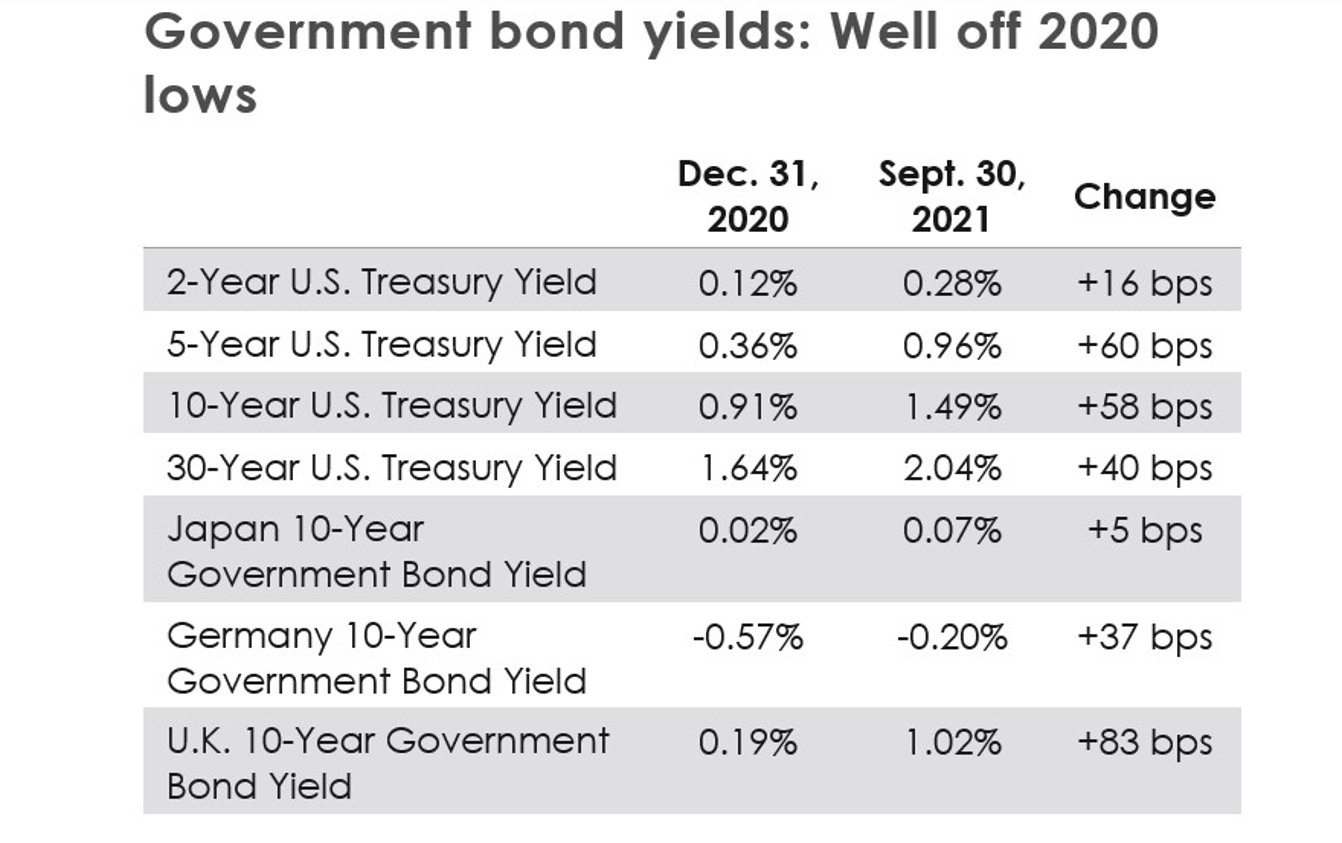

Treasury yields awakened by Fed taper progress

Since the height of the COVID-19 emergency, the Federal Reserve has been buying $120 billion of Treasurys and Mortgage-Backed Securities per month, supporting liquidity and contributing to low interest rates. At its September meeting, the Fed communicated that it could begin reducing—or tapering—the amount of its monthly purchases this November.

The tapering guidance was followed by a sharp back-up in Treasury yields. The Fed has said that tapering should be viewed as independent of future interest rate hikes. The Fed’s most recent dot plot showed that six Fed members see one 25 basis points interest rate increase next year while three members see two such hikes, leaving investors to contemplate tighter monetary policy in 2022.

Entering the final stretch of 2021

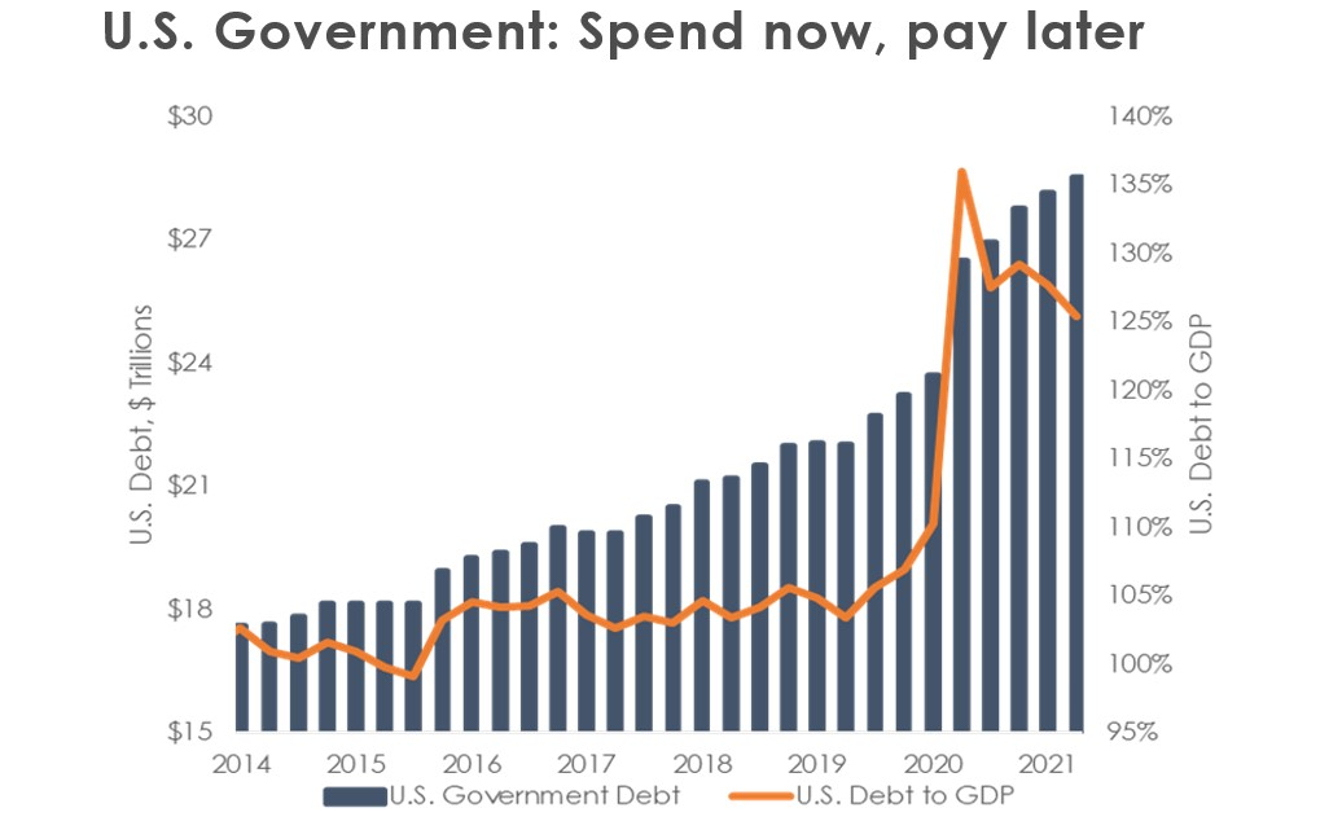

On Oct. 18, the U.S. government will hit the proverbial “debt ceiling” set by Congress, who must raise the debt ceiling so that the U.S. can continue to borrow and pay its bills. The debt ceiling has been raised many times throughout the past several years, leading to U.S. government debt of almost $29 trillion or 125 percent of GDP. Fortunately, Congress appears to be nearing a compromise in raising the debt ceiling, which would avoid a potentially adverse event for the economy and markets.

Source: Bloomberg as of Sept. 30, 2021

The debt ceiling is not the only spending measure that has been tangled up on Capitol Hill. Congress is also debating broader spending and infrastructure packages where success is not quite certain due to divisions within the Democratic Party. There is still a good chance of higher corporate tax rates in 2022, which we view as a potential headwind for equity markets.

As we look ahead, corporate earnings and economic output are increasing at a healthy, but moderating pace. We believe consumers have elevated savings cushions, and effective vaccines are protecting us from COVID-19. Nevertheless, the emergency monetary and fiscal policy that supercharged growth and asset returns over the past several months is turning less accommodative. Inflationary pressures have yet to abate and are weighing especially on low- and middle-income households. As we enter a more challenging stage of the recovery for investors, we encourage a focus on key fundamental drivers: interest rates, earnings, and valuations. See you in 2022.

Discover more from MassMutual …

What should investors do about inflation

Life insurance, annuity investing alternatives

3 ways to manage capital gains tax bites

_____________________

1 Commodities = S&P Goldman Sachs Commodity Index; REITS = Vanguard Real Estate ETF; Value = iShares Core S&P U.S. Value ETF; Mid Cap = Vanguard Mid-Cap ETF; Large Cap = Vanguard Mega Cap ETF; Growth = iShares Core S&P U.S. Growth ETF; Small Cap = Vanguard Small Cap ETF; Developed Markets = Vanguard FTSE Developed ETF; TIPS = iShares TIPS Bond ET; Emerging Markets = Vanguard FTSE Emerging Markets ETF; Aggregate Bonds = iShares Core Aggregate Bonds ETF; Gold = SPDR Gold Shares.