Everything continued to go right for the U.S. economy and markets in the second quarter of 2021. More than half of the eligible population is now fully vaccinated, and nearly all COVID-19 restrictions were lifted even in the most previously restrictive states. Equity markets maintained their upward trajectory as the S&P 500 posted its fifth straight quarterly gain, bringing year-to-date total returns to 15 percent, the index’s second-best first half performance since 1998. U.S. Treasury yields remained stubbornly range bound and have recently moved lower despite consumer price index readings in April and May of 4.2 percent and 5.0 percent, respectively.

While concerns about the COVID-19 Delta variant may have delayed reopening plans in certain regions, the bullish narrative has prevailed on supportive monetary and fiscal policy, vaccine progress, reopening momentum, strong corporate profit growth, and robust equity inflows. Although inflation continues to garner a lot of attention, market indicators suggest a consensus view consistent with the Federal Reserve’s: That inflation pressures are transitory and will not pose downside risks. The White House reached a tentative bipartisan infrastructure deal, which includes $579 billion of new spending, but is not funded by higher taxes. We enter the second half of 2021 on the back of historically strong economic and earnings growth, an exceptionally favorable policy backdrop, and as President Biden stated, “closer than ever to declaring our independence from a deadly virus”. As great as this all sounds, investors should be cognizant of risks to the outlook. Equity and bond valuations are stretched, and there is no guarantee that inflation pressures will fade just because the Fed says so.

Source: Bloomberg as of June 30, 2021.

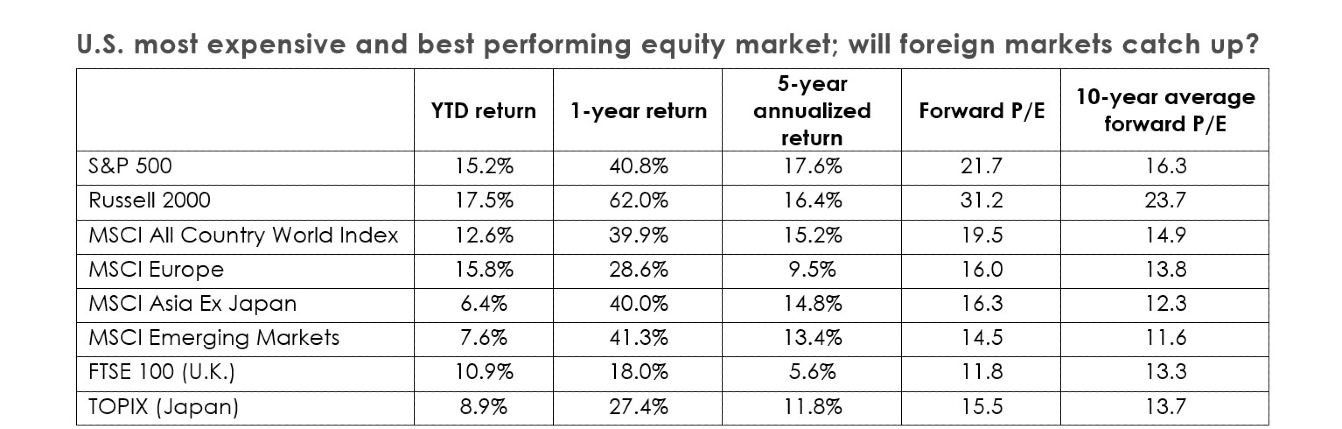

Equities see strong first half in 2021

Global equity markets continued onward and upward in the second quarter, led by the U.S. With price-to-earnings (P/E) multiples at historical highs, returns have been entirely driven by earnings growth and positive earnings revisions. S&P 500 first quarter earnings per share grew 52 percent year-over-year, up from 24 percent expected at the beginning of the quarter; full year 2021 earnings per share are expected to be up an incredible 36 percent over 2020. Companies have posted strong earnings growth and expanded profit margins despite input and wage cost pressures due to pricing power and productivity initiatives.

While many companies announced wage increases throughout the second quarter, many also announced hikes in the prices of their products and have been able to reach pre-pandemic levels of output with much fewer workers. U.S. growth stocks outperformed value in the second quarter following several months of value outperformance, supported by the decline in long-dated Treasury yields and easing inflation concerns.

Source: Neuberger Berman as of June 30, 2021.

A reasonable question is: How much upside is there from here for U.S. equities? We do not expect the second half to be nearly as strong at current valuations with earnings and economic growth moderating, albeit from very high levels. The Fed and incoming economic data are also likely to continue to introduce volatility as investors eye Fed tapering of asset purchases and an eventual first interest rate hike.

Reopening drives surge in U.S. economic growth

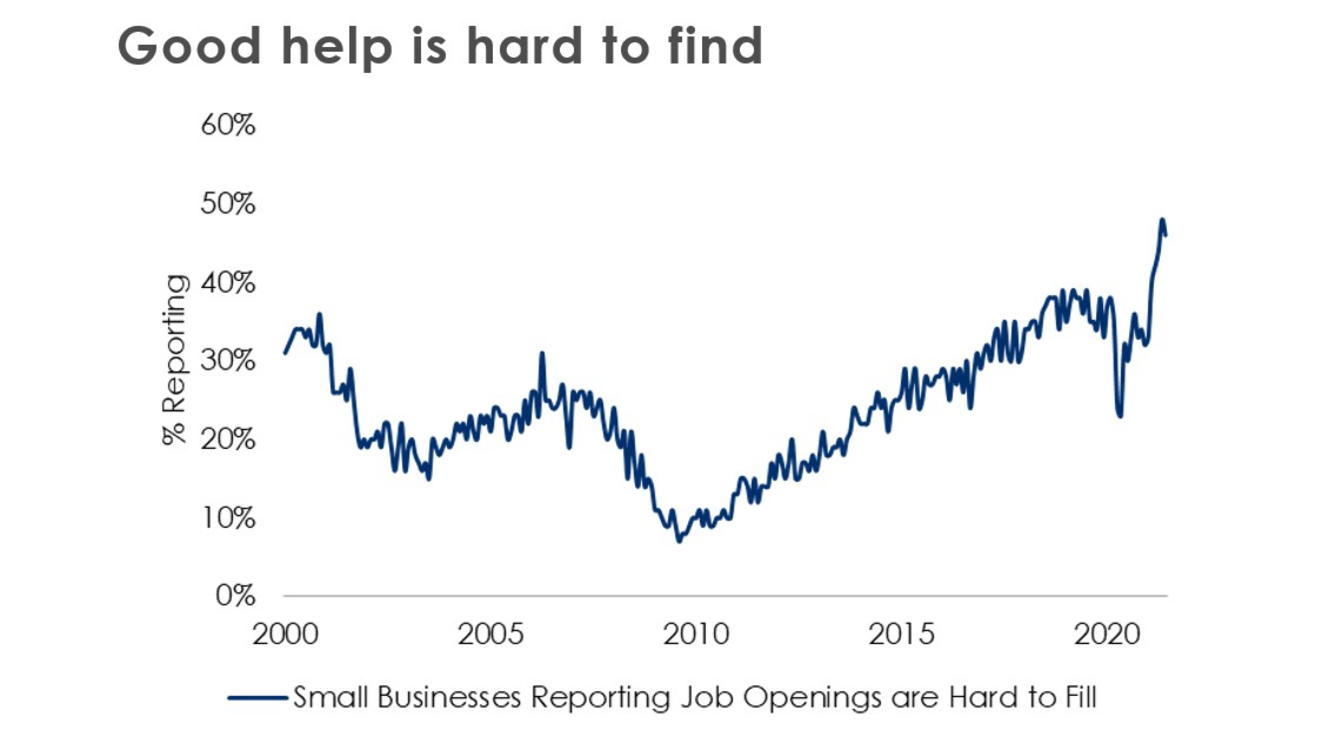

The U.S. economy grew 6.4 percent in the first quarter, and consensus expects growth accelerated to 9 percent in the second quarter as the reopening ramped up. Economic growth, driven by deficit-financed government spending, has exceeded expectations, but the job market recovery is lagging with the unemployment rate still at recessionary levels, total employees on payrolls still seven million below pre-COVID levels, and labor force participation at its lowest level since the 1970s. According to the NFIB small business survey, small businesses have never had more difficulty in filling open positions. Many reasons have been cited for the labor shortage, but the important question as with many factors right now is whether the supply/demand mismatch will persist, driving up wages and contributing to inflation pressures.

Source: Bloomberg as of June 30, 2021

Speaking of inflation, strained supply chains and reopening demand have led to a surge in prices for many goods and services, resulting in some of the strongest inflation readings in decades. Inflation in many categories, such as used cars and trucks, is very likely temporary as supply chains catch up and demand normalizes. However, as the initial “reopening” effects fade, investors should pay close attention to wages and rent or the cost of shelter as these categories could contribute to more sustained inflation pressures. Wage information is very “noisy” right now due to job growth being highly skewed to lower wage sectors, and measures of rent growth have yet to pick up despite housing prices reaching all-time highs. More persistent and higher inflation than the Fed or investors expect continues to represent a risk to the economic and market outlook.

Spiking inflation, but lower Treasury yields?

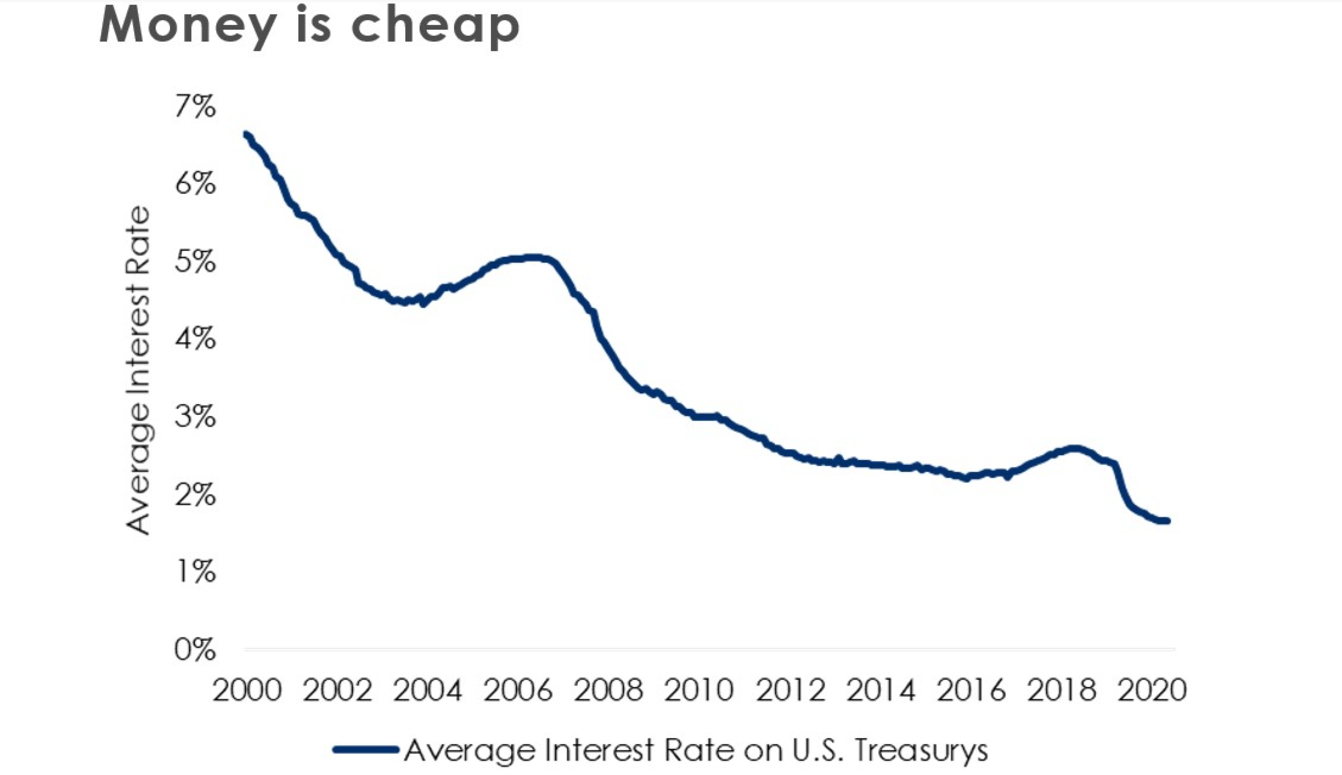

Defying consensus expectations for yields to move higher throughout 2021, long dated Treasury yields peaked at the end of the first quarter and have been declining throughout the spring and into the summer. Is this a technical phenomenon, a reflection of concerns over the Delta variant particularly from international investors, or is the Treasury market trying to tell us that growth and inflation have peaked? We do not know, but believe that U.S. Treasury yields seem low considering the enormous size of U.S. government debt ($28.5 trillion), second quarter GDP growth at 9 percent, and inflation at 5 percent.

Source: Bloomberg as of June 30, 2021

At its June meeting the Fed pulled forward its median forecast for its first interest rate hike into 2023 versus prior expectations for liftoff to occur in 2024 or later, leading to some concerns the Fed could potentially pull back support too soon and hamper long-term growth prospects, another possible contributor to the decline in long-term Treasury yields. In addition to future interest rate hikes, the main question on the market’s mind right now is when the Fed will announce and eventually taper its monthly purchases of $120 billion of Treasurys and mortgage-backed securities. We estimate the Fed could announce its plans for tapering sometime in the third or fourth quarter of this year.

Ultra-low borrowing costs

The U.S. government – despite carrying a debt load of over $28 trillion that is growing at an alarming rate – continues to enjoy historically low borrowing costs courtesy of the Fed keeping interest rates artificially low. In addition to a bipartisan infrastructure bill, the Senate has plans to pass a separate package via reconciliation that includes spending surrounding climate change and social programs. At the same time, it is unlikely for the corporate tax rate to rise much above 25 percent, so we expect the theme of debt-financed government spending to continue.

Source: Bloomberg as of June 30, 2021.

Source: Bloomberg as of June 30, 2021.

Therefore, the Fed raising short-term interest rates has significant consequences for federal spending; in fact, every 25-basis point interest rate hike adds about $10 billion to interest payments annually for the U.S. government. Could this impact the Fed’s future policy decisions? Perhaps. We continue to draw attention to the growing size of U.S. government debt for investors because of its potential long-term implications for the U.S. dollar, Treasury yields, and tax rates.

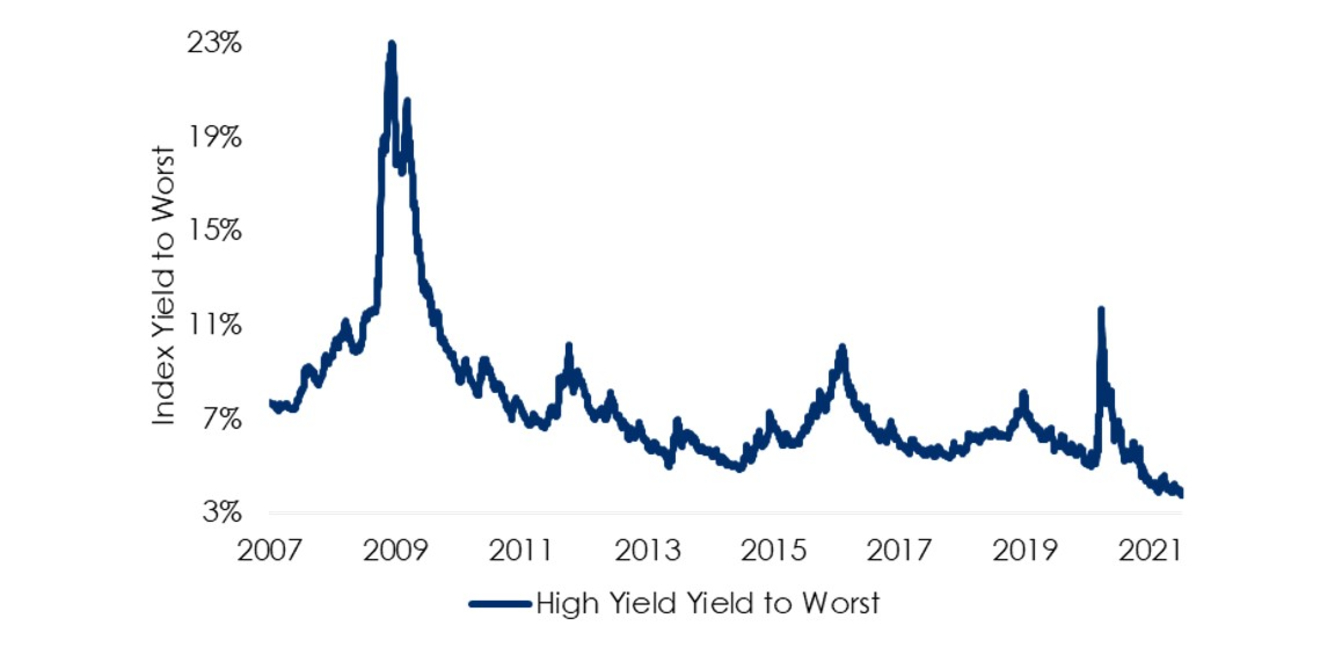

The U.S. government is benefitting from exceptionally low borrowing costs, and so are corporate issuers. Yields on high yield corporate debt fell to all-time lows during the second quarter as government bond yields declined and investors demanded less compensation or “spread” for default risk. Corporate debt issuers are enjoying ideal conditions with strong economic growth and a low cost of funds driven by supportive monetary policy and investor appetite for yield investments.

Second half outlook

Simply put, government debt-financed U.S. economic growth of 5-10 percent is not sustainable, and we expect economic and earnings growth to moderate over the next several quarters. Elevated pent-up savings is a tailwind to consumer spending, but not enough to sustain such high growth rates. As we enter the second half of 2021, market participants will increasingly focus on 2022 U.S. economic growth, corporate earnings, fiscal policy, and monetary policy. The Biden administration is likely to continue to increase government spending with partial offset from higher individual and corporate tax rates.

Consensus expects the Fed to remain accommodative, err on the side of easy versus restrictive monetary policy, and telegraph well in advance its future policy intentions. One thing that could throw a wrench in this outlook is persistently higher inflation, which many view as a low probability. COVID-19 appears to be mostly behind us, but the Delta variant leaves lingering uncertainty. Equity and bond markets are priced for perfection, making investor asset allocation decisions exceptionally challenging. As we enjoy Summer 2021, which is thankfully much different from Summer 2020, we encourage investors to question the consensus view, consider the long-term implications of current extremes in fiscal and monetary policy, and avoid letting biases about past performance determine future decisions.

Discover more from MassMutual …

What should investors do about inflation

Life insurance, annuity investing alternatives

3 ways to manage capital gains tax bites

_____________________