2020 was an unimaginable and extraordinary year that will be studied for decades to come. Humanity was rocked by a devastating and novel virus that we all know as COVID-19. The COVID-19 pandemic brought the longest U.S. economic expansion on record to a screeching halt and drove unprecedented policy action by governments and central banks. The Federal Reserve’s balance sheet grew by over $3 trillion to $7.4 trillion. U.S. Treasury yields dropped to all-time lows as the Fed aggressively reduced interest rates. U.S. fiscal stimulus of $3.6 trillion (17 percent of GDP) led to the largest deficit-to-GDP ratio since WWII and drove total U.S. government debt to over $27 trillion. U.S. GDP fell by the most on record during the second quarter. Oil prices actually went negative in April. As if a global pandemic and lockdowns were not enough for investors to process, the year concluded with a contentious U.S. presidential election, and the U.S. is experiencing a disturbing level of political division. Perhaps most astounding for some market observers is that in such a catastrophic and uncertain year for the world at large, global equities posted annual double-digit returns with the NASDAQ returning over 45 percent.

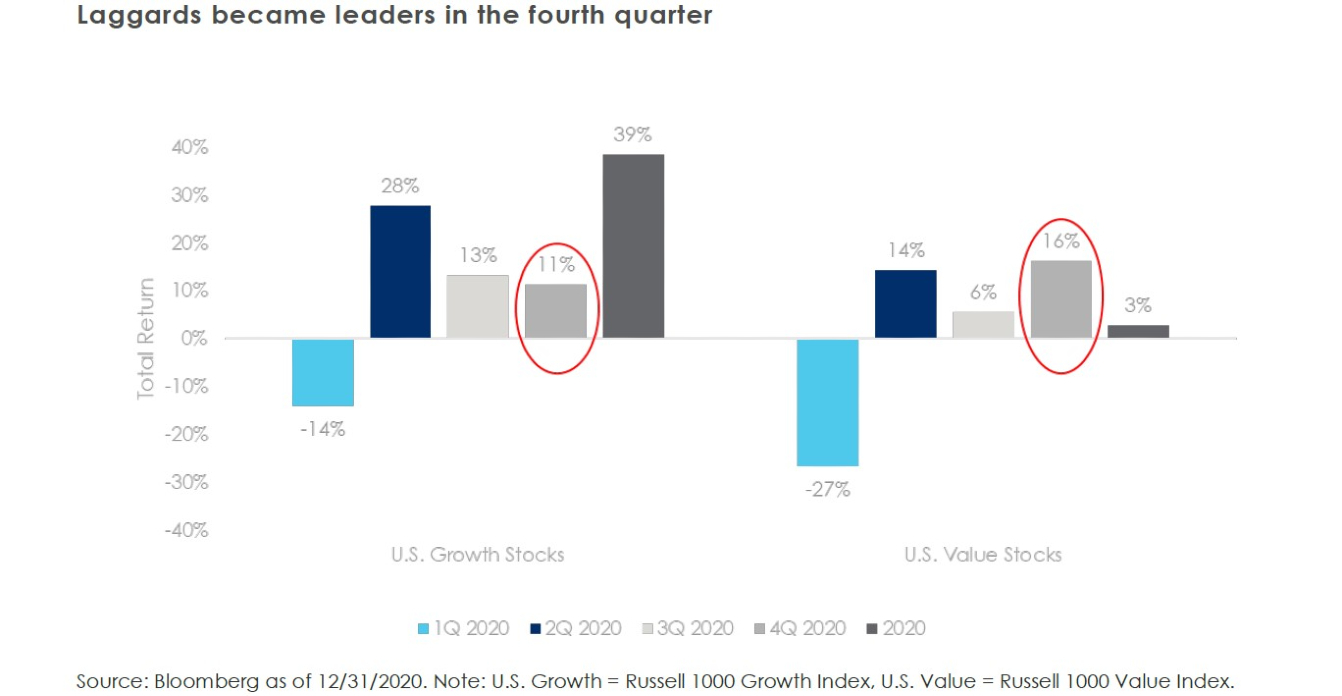

The mood in financial markets as we enter 2021 is much different than the fear and anxiety experienced in March 2020. Troubling trends in COVID-19 cases have been mostly overshadowed by the approval and distribution of two vaccines with more on the way. Positive vaccine developments catapulted the previously unloved value stocks to outperform growth stocks in the fourth quarter in one of the sharpest rotations in history. The Pfizer/BioNTech vaccine announcement in early November led small cap U.S. equities to their best month on record, returning over 18 percent. Fueling further optimism for 2021, Congress finally agreed on a $900 billion stimulus package, delivering stimulus checks of $600 to eligible recipients.

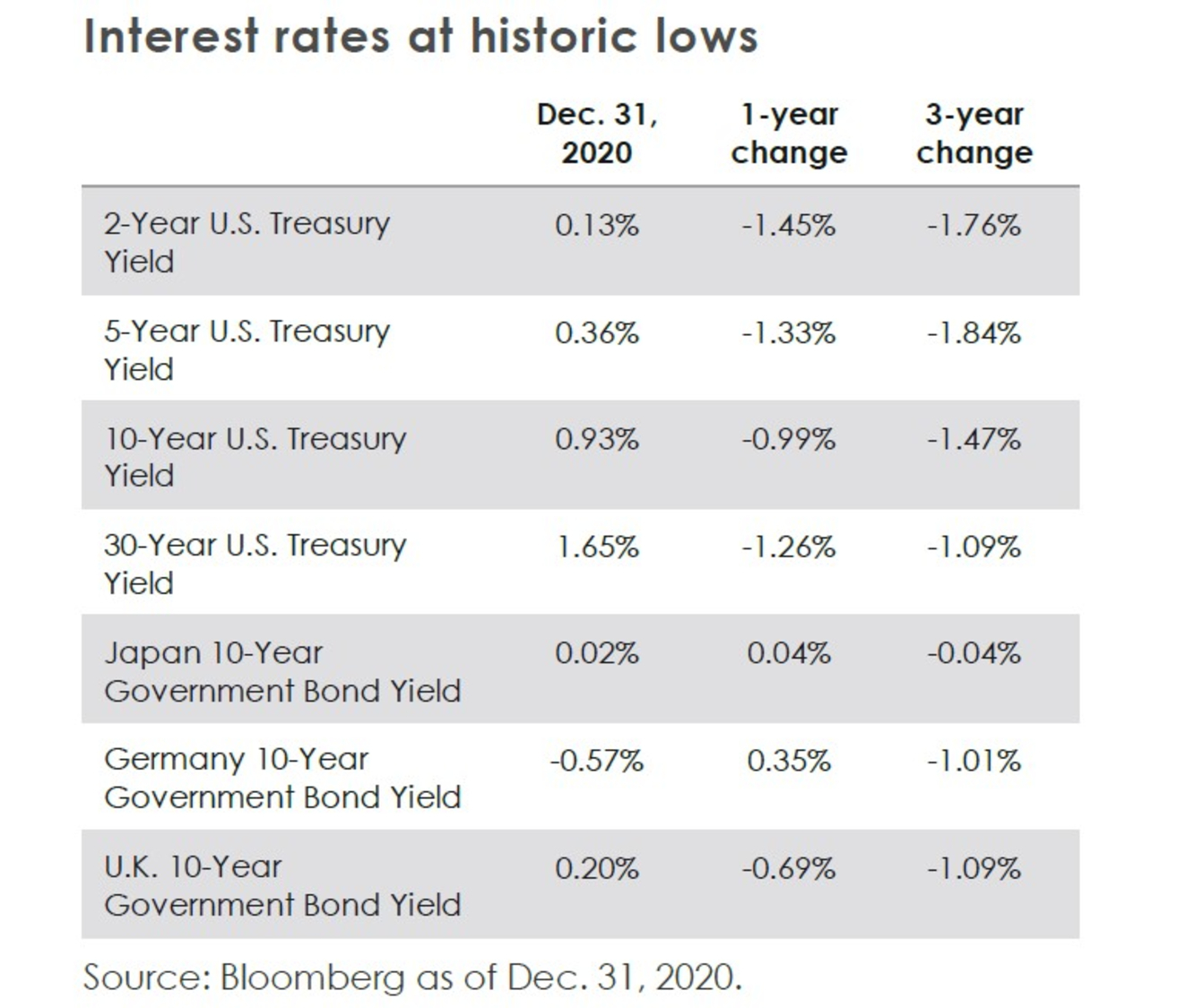

With a Democratic administration taking over the White House and a razor-thin Democratic majority in the Senate (with the Vice President as the tiebreaker), major tax policy overhauls are unlikely until 2022. However, there is a better chance of further stimulus and other spending initiatives in 2021, which are positive for economic growth. Last, but certainly not least, the Fed remains committed to its asset purchase program and expects to maintain short-term interest rates at zero for the next two to three years. Turning the page to 2021, investors are focused on the path to a full economic restart and most importantly, the implications of a post-COVID world for interest rates, which are near historic lows, and equity prices, which are at all-time highs.

Vaccine + pent-up demand = 2021 growth rebound

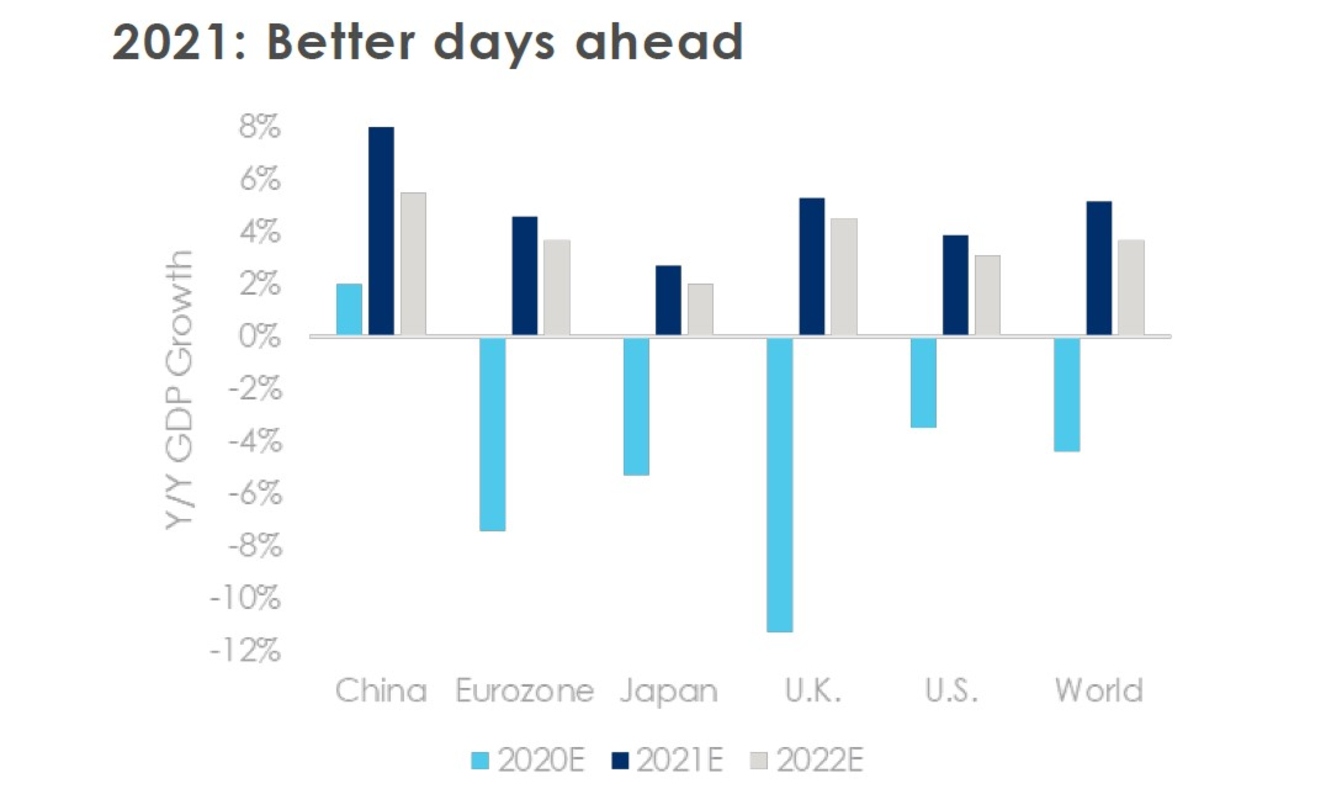

The global economy is expected to grow 5.2 percent in 2021 after contracting an estimated 4.4 percent in 2020, led by emerging markets, and driven by a “return to normal”. U.S. economic growth is forecasted to improve to 3.9 percent in 2021 after estimated growth of -3.5 percent this past year. Economists’ forecasts reflect strong economic growth momentum, particularly in the second half of 2021, as vaccines are more widely distributed and the hardest hit sectors by COVID-19, such as travel and leisure, finally recover. The economic rebound since the second quarter of 2020 has been led by goods-producing sectors and manufacturing as consumption has shifted to goods over services. In the U.S., the housing market has been exceptionally strong, supported by record-low interest rates. In fact, 2020 was the best year on record for lumber, whose price rose by more than 200 percent.

Source: Bloomberg as of Dec. 31, 2020.

Although growth is expected to decelerate from the fourth quarter of 2020 to the first quarter of 2021, recently enacted fiscal stimulus should act as a stabilizer. As we move to a post-COVID world, considerable pent-up demand for out-of-the-house experiences combined with record levels of personal savings are likely to lead to another shift in consumption trends and a more broad-based recovery by the end of 2021. Our economic outlook is constructive.

2020: Low interest rates and strong equity returns

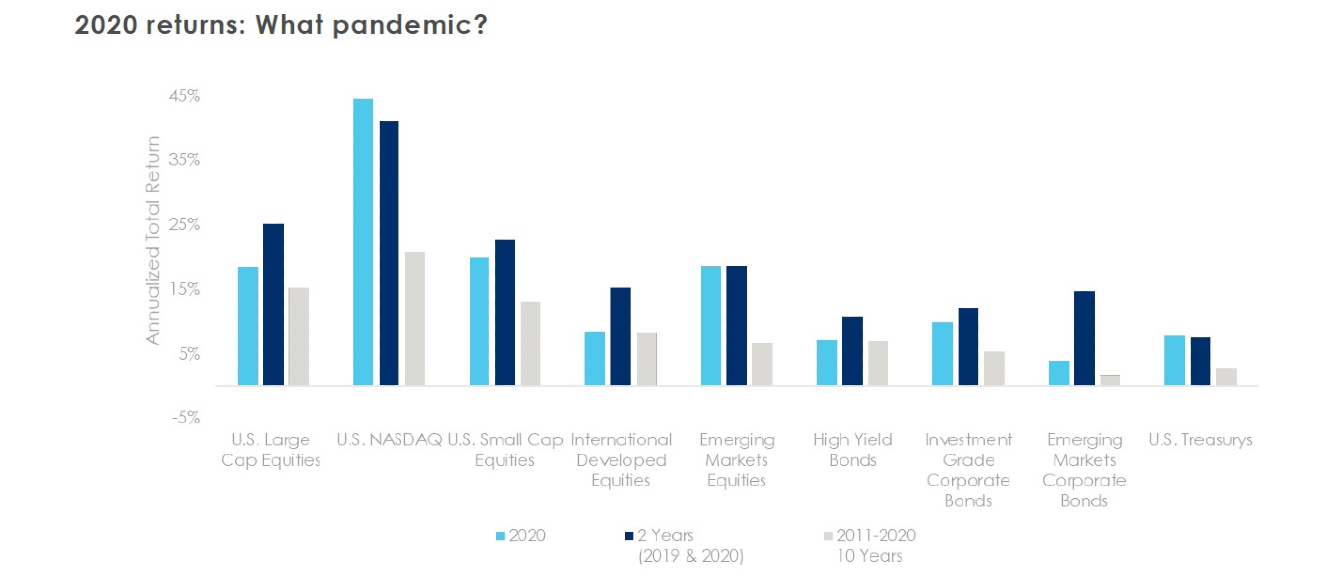

Turning to financial markets, the key question for investors is: Given strong returns in 2020, how much of the economic recovery is already priced in? Returns have not only been strong over the past two years, but over the past decade, despite tepid post-Global Financial Crisis economic growth. 2020 was a continuance of U.S. equity outperformance (though emerging markets equities had a strong year) with significant appreciation in the share prices of names like Apple, Amazon, Microsoft, and Google. Technology dominance was intensified by the pandemic which made Amazon Prime and Netflix must-haves for all of us stuck at home, and which was the demise for many brick and mortar retailers already under significant stress.

Source: Bloomberg as of Dec. 31, 2020.

Note: U.S. Large Cap Equities - S&P 500, U.S. Small Cap Equities – Russell 2000, International Equities - MSCI EAFE Index, Emerging Markets Equities, MSCI EM Index, High Yield Bonds - Barclays High Yield Index, Investment Grade Bonds - Barclays Investment Grade Corporate Index, Emerging Markets Government Bonds - JPM GB-EM, U.S. Treasurys - Barclays Government and Treasury Index.

We have previously noted the impact of low interest rates and central bank liquidity on equity prices and believe that the expansion in valuation multiples over the past decade was largely driven by these two factors. The rebound in equity markets in 2020 likely would not have been nearly as strong without extraordinary monetary and fiscal policy support. We continue to believe that recent returns will be difficult to sustain given the level of interest rates and valuations. Some of the returns reflecting the projected economic recovery of 2021 were likely “pulled forward” to 2020, leading to a surprisingly strong year in 2020. Nevertheless, the economic backdrop for equities is favorable in 2021 as earnings rebound alongside economic growth. We expect cyclical sectors of the market in particular to benefit from the post-pandemic recovery.

2020 trends: Retail participation, IPO, and SPAC activity

The past year was marked by several fascinating trends including significant participation from retail investors in equity markets and relatedly, a record-setting year for IPOs and Special Purpose Acquisition Companies (SPACs). According to Bloomberg, retail investors made up a fifth of U.S. stock trading volume this year, more than double the share a decade ago and behind only market makers and high-frequency traders in terms of volume.1 Also according to Bloomberg, retail investors exacerbated momentum trading in 2020 as investors reacted to price action and not fundamentals. In addition to stay-at-home orders, we believe “FOMO” or fear of missing out has been a driver of increased retail investor participation.

Retail participation was also fueled by a record year for IPOs with more than 450 offerings raising $179 billion in 2020. The biggest segment of the IPO market was SPACs, which raised $79 billion in the U.S., according to Bloomberg, exceeding the combined total in all previous years. SPACs have been described as “shell” or “blank check” companies. They raise investor money through an IPO before investors actually know the underlying company in which they are investing, and then the management team of a SPAC identifies a company of interest to acquire, saving the target company a lot of time and effort on disclosures had it gone public directly.

Retail investors have also sought higher returns in concentrated stock positions, options trading and through leveraged ETFs, according to the Wall Street Journal, with the amount that investors have borrowed against their investment portfolios recently reaching new record highs.2 Similar to what we wrote in our second quarter report, we stress that there is a clear distinction between trading and investing. The former has a much higher risk profile and lower likelihood of a favorable outcome while the latter, if exercised under the principles of diversification and a long-term perspective, has a greater potential for financial success and long-term wealth. It’s very important to point out that while leveraged investment positions such as options can lead to higher returns, they can also amplify downside.

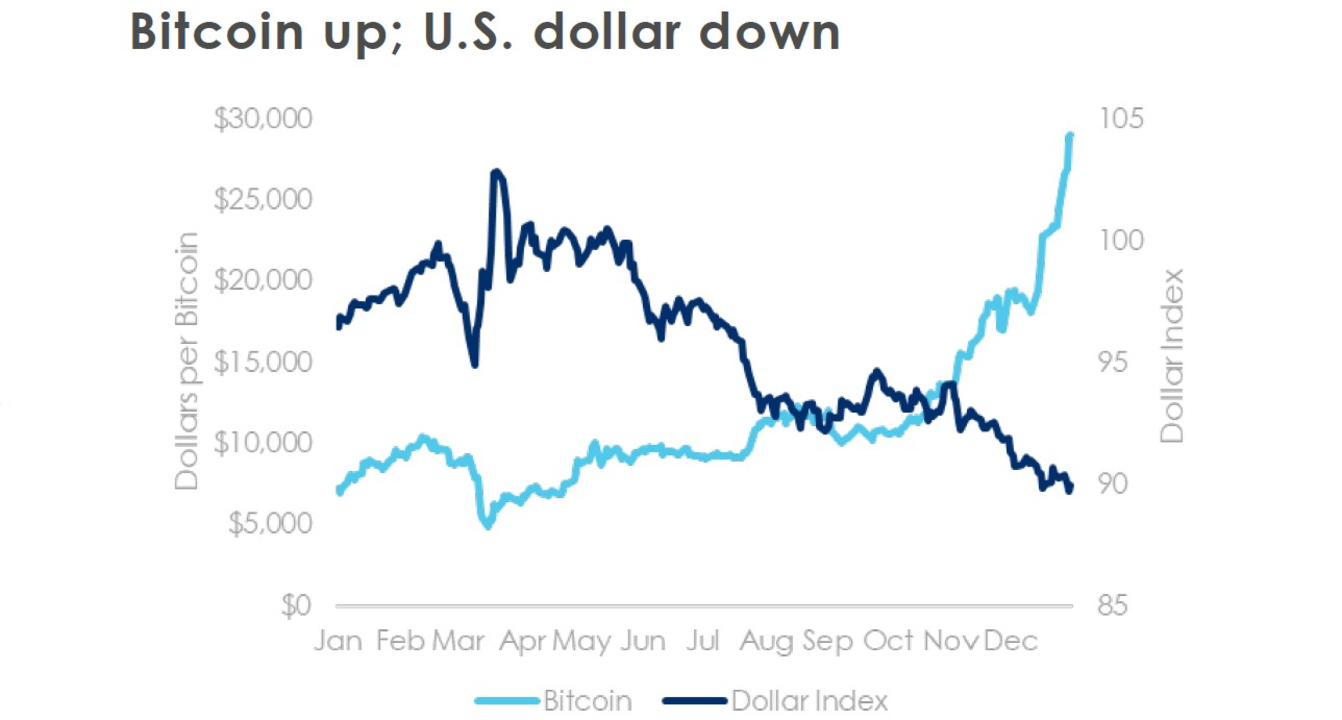

The U.S. dollar, inflation, and Bitcoin

The end of 2020 saw continued depreciation of the U.S. dollar and another record-setting rally in cryptocurrency Bitcoin, which rose over 300 percent in 2020 on heightened interest from institutional investors and large corporations. Concerns of continued U.S. dollar depreciation, exacerbated by the tremendous policy response to the COVID-19 pandemic, have also played a role in investors flocking to Bitcoin. The U.S. government debt-to-GDP ratio is at a record 130 percent, and the U.S. money supply is growing at a record pace of 25 percent year-over-year, which compares to growth of around 10 percent post the Global Financial Crisis.

Source: Bloomberg as of 12/31/2020; Dollar Index = DXY Dollar Index.

Bitcoin has also been discussed as a potential inflation hedge similar to gold. Inflation remains a key debate for 2021 and beyond, given the amount of stimulus that has been enacted and as growth rebounds. Adding to inflation concerns is the Fed’s pledge to allow inflation to temporarily overshoot its target in order to prioritize recovery of the labor market. Inflation expectations as measured by Treasury inflation protected securities (TIPS) have risen to two-year highs with ten-year inflation expectations recently rising above 2 percent.

2021 outlook

We enter 2021 with an optimistic economic outlook and expect a global synchronized recovery in the second half of the year. The first quarter could be bumpy for the economy and markets with high valuations, a continued surge in COVID-19 cases, and ongoing restrictions, but the environment should improve as the year and vaccine distribution progresses. A rebound in corporate earnings and low interest rates are positive tailwinds for equity markets; however, this is tempered by elevated valuations, particularly in the technology sector which makes up a significant portion of the U.S. equity market. We believe corporate debt and equity markets are fully or near-fully valued and that equity returns will likely follow earnings and interest rates. Although we expect synchronization in the economic recovery, we also believe financial market returns could be more disperse across regions and sectors in 2021 as we emerge from the pandemic and the laggards of 2020 catch up in 2021, similar to what we observed in the fourth quarter.

The Federal Reserve is widely expected to maintain its accommodative policy stance, underpinning the economic recovery and risk assets. A faster-than-expected acceleration in inflation is a risk and could result in a move higher in interest rates, prompting market volatility and investors to revisit expectations for monetary policy normalization. We continue to keep an eye on the growing U.S. fiscal deficit and debt, which as mentioned above, are dollar negative and could contribute to higher inflation. Under a Biden administration and with a small Democratic majority in the Senate, the current tax regime is unlikely to change drastically in 2021, but we do expect additional stimulus, more predictable trade policy, and a greater focus on the environment and inequality under this new government. 2020 was a year of unprecedented proportions with a market recovery that far exceeded expectations. With the worst hopefully behind us, we wish you all the best in 2021 and look forward to recapping the first quarter with you in a few months.

Learn more from MassMutual …

Markets and COVID: What’s happened — and what might be ahead

____________________________

1 Day Traders Put Stamp on Market with Unprecedented Stock Frenzy 12/31/2020; Reidy, Mookerjee, Ponczek, Barnert; Bloomberg News.

2 Investors Double Down on Stocks, Pushing Margin Debt to Record; 12/27/2020; Wursthorn; The Wall Street Journal.