Despite the emergence of two fast-spreading COVID-19 variants, inflation that has proven more “sticky” than “transitory,” and central banks beginning to remove monetary accommodation, U.S. equities posted a third-straight year of strong double-digit gains with the S&P 500 returning approximately 27 percent in 2021. Treasury yields rose significantly but remain extremely low by historical standards. Commodities also had a record year as oil prices jumped sharply. Around nine billion vaccine doses have been administered, allowing global mobility to improve through this past year’s COVID waves. Unprecedented policy support together with record high corporate earnings helped to underpin bullish sentiment through much of the year. TINA (“there is no alternative” to stocks) and FOMO (“fear of missing out”) were widely cited as driving stretched valuations and more than $1 trillion of global equity inflows in 2021.

After President Biden signed a much-awaited $1 trillion infrastructure plan into law in the fourth quarter, the administration failed to garner enough support for its $1.7 trillion “Build Back Better” social spending plan. The Federal Reserve, no longer able to credibly label inflation at forty-year highs as “transitory,” announced in November it would taper its $120 billion per month asset purchase program by $15 billion per month before announcing it would double the pace to $30 billion per month at its December meeting. As we enter 2022, the S&P 500 sits near all-time highs, and the Fed’s balance sheet has more than doubled over the last three years. Supply chains and labor markets remain stretched, keeping inflation stubbornly high, and the Omicron variant is only making matters worse. We expect the global economic recovery to continue into 2022 but nevertheless see a more challenging year for investors as both the bull market and pandemic mature and monetary policy becomes less accommodative.

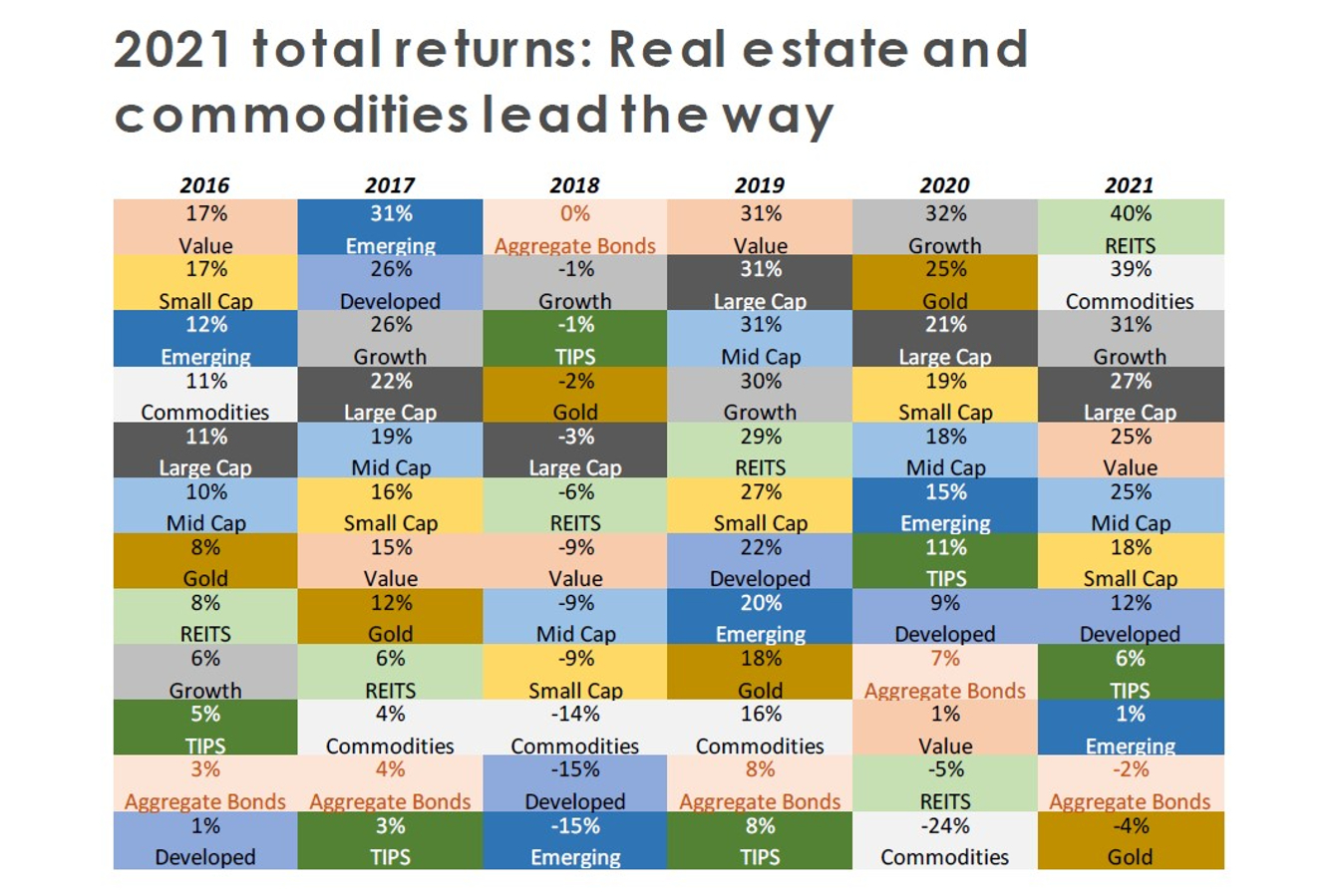

Source: Cornerstone Macro as of Dec. 31, 2021.

Global economy endures despite double blow from COVID variants in second half

The U.S. and world economy are projected to have grown 5.6 percent and 5.9 percent respectively in 2021, overcoming both the Delta and Omicron variants and extreme strains on supply chains and labor markets. Economies have adapted relatively well to living with COVID, helped by vaccines, human ingenuity, and automation. Although the goods sector has completely healed, service sector activity has yet to fully recover to pre-COVID levels. Service sector activity remains close to 4 percent below its pre-pandemic path as ongoing restrictions and consumer caution remain overhangs.

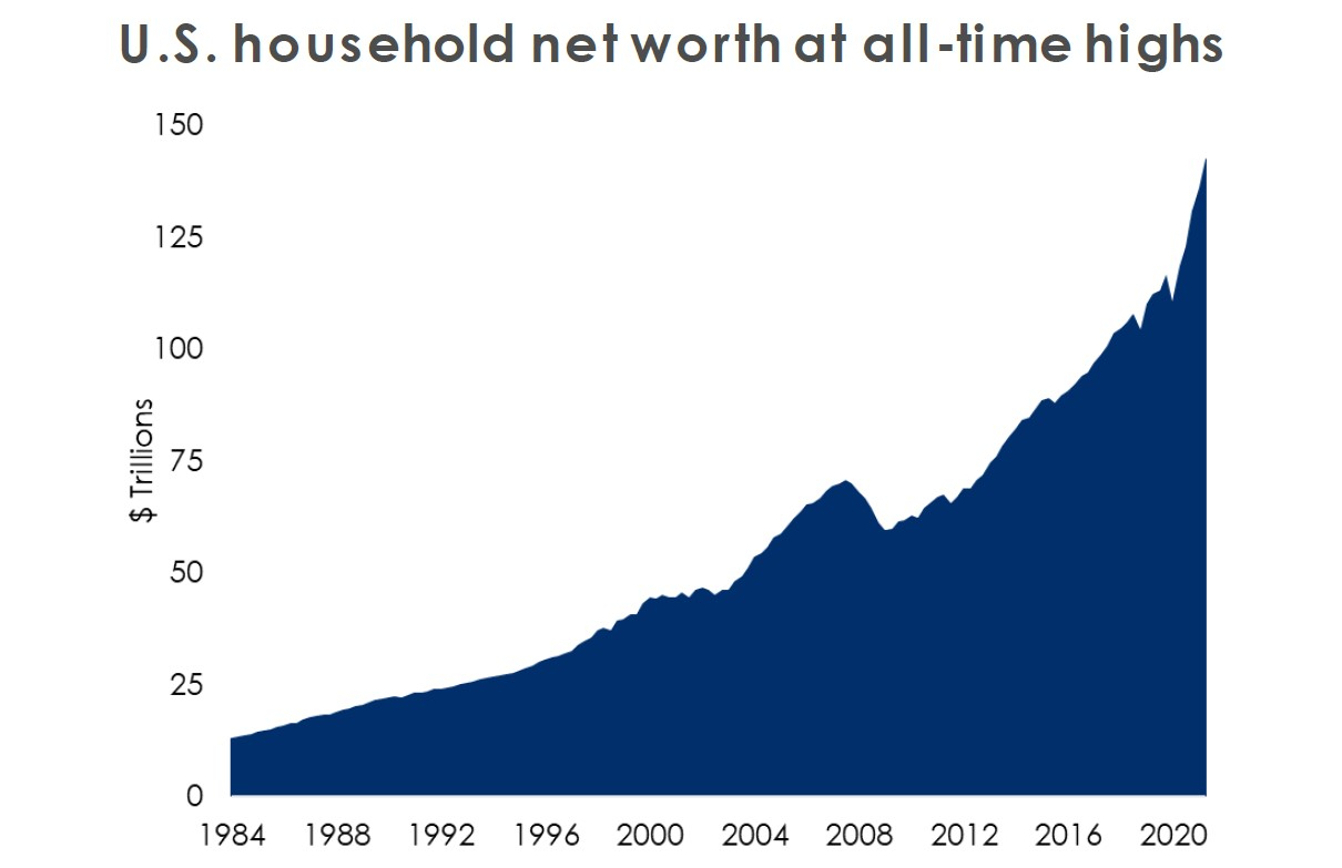

Source: Bloomberg as of Dec. 31, 2021

U.S. household balance sheets are also in a position of relative strength. While monthly household savings are now back at pre-pandemic levels ($100 billion/month versus a peak of $500 billion/month), the $2.6 trillion in excess savings during the pandemic will continue to support consumer spending growth over the coming quarters. In fact, household net worth has reached another all-time high due to elevated savings, record financial asset prices, and soaring home prices. While moderating, the demand side of the economy thus remains relatively robust despite extraordinary fiscal stimulus rolling off. We view the supply side as a greater source of risks to the fundamental outlook. Many supply-chain bottlenecks have yet to ease, and the longer imbalances last, the more likely we are to see sustained price increases and downside risks to profit margins.

U.S. equity markets see record three-year run despite COVID

According to Morgan Stanley, 2021 marked the third consecutive year in which U.S. equities posted an annual return above 15 percent, the only other such instance since 1929. 2021 also marks the 13th time out of the S&P 500’s 65-year history that returns in a single year have exceeded 25 percent. 2021 also marked yet another year of U.S. equity markets outperforming both developed and emerging foreign equity markets. Extraordinary U.S. equity returns were driven by extremely strong earnings growth and resilient profit margins; 2021 S&P earnings per share are expected to have grown approximately 47 percent relative to 2020. With this growth rate expected to slow sharply to around 8 percent this year and interest rates likely increasing, it is no surprise that strategists are rather divided on the outlook for U.S. equities in 2022. The range of strategists’ S&P 500 year-end 2022 price targets compiled by Bloomberg stretches from 4,400 to 5,300—a 20 percent spread that is the second widest in a decade.

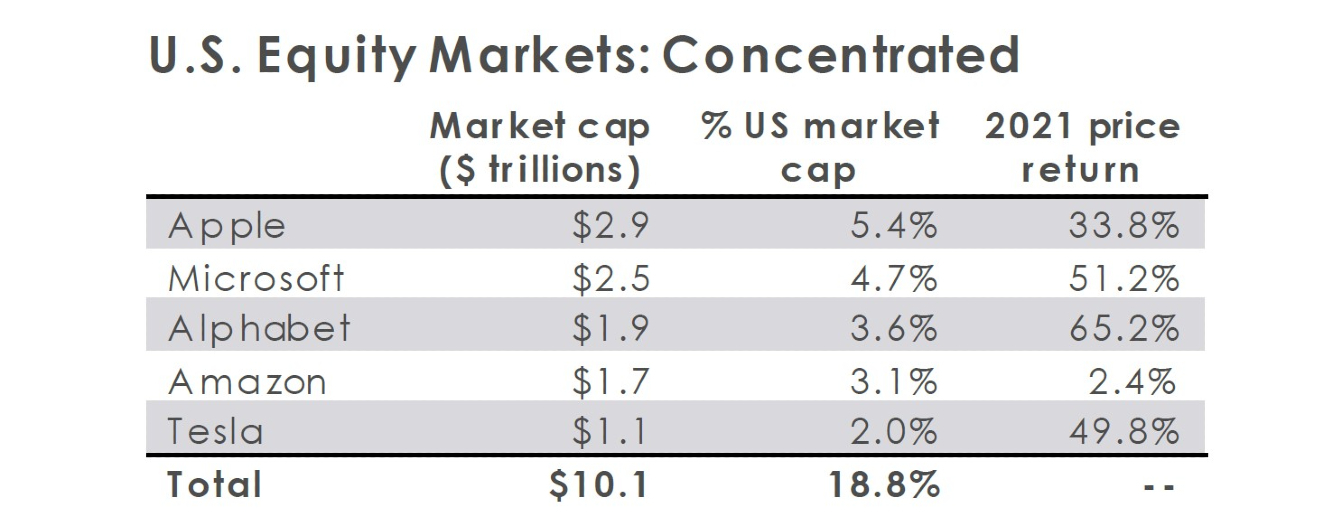

Despite value stocks having a very strong year, growth stocks were the winners in 2021, buoyed by soaring technology shares. Apple’s market capitalization recently surpassed $3 trillion, which is more than 10 percent of the $23 trillion U.S. economy! The top five stocks in the S&P 500, Apple, Microsoft, Alphabet (Google), Amazon, and Tesla make up approximately 19 percent of the total U.S. equity market capitalization, meaning that any investor who simply follows an index strategy has significant exposure to these behemoths. As we approach a Fed tightening cycle and potential rising interest rate environment, it is important for investors to remember that technology/growth companies tend to exhibit a higher sensitivity to interest rates. This has been most recently evidenced by the sell-off in higher-valued growth and technology shares as Treasury yields have risen sharply at the start of 2022.

Source: Bloomberg as of Dec. 31, 2021.

Fed taper underway; three interest rate hikes expected in 2022

In 2022, the macroeconomy and markets will likely begin a journey toward tighter financial conditions accompanied by protection from still abundant liquidity. After two years of the most aggressive easing ever enacted, expanding its balance sheet to around 40 percent of GDP, the Fed will likely slow and then conclude its asset purchase program. Developed market central banks added nearly $4 trillion in quantitative easing in 2021 after adding almost $8 trillion in 2020 and are still on track for nearly $1 trillion in purchases in 2022 despite the start of tapering, according to JP Morgan.

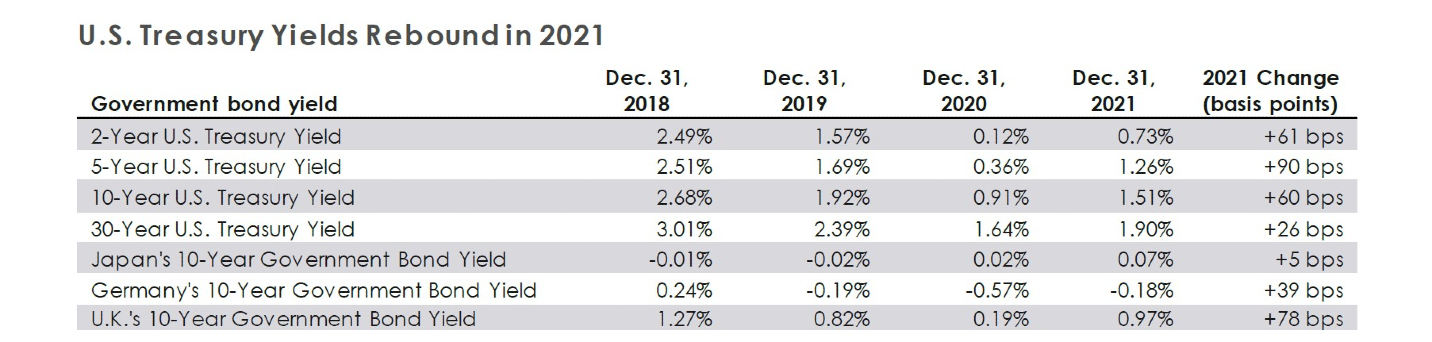

Source: Bloomberg as of Dec. 31, 2021.

After concluding its asset purchase program in the first quarter, the Fed’s dot plot shows three 25 basis point hikes expected in 2022 and an additional three hikes in 2023. With unemployment expected to drop below 4 percent in 2022, the Fed’s focus is likely to shift towards the goal of reaching price stability amidst record inflation. Alongside interest rate hikes, the Fed is also considering reducing the size of its balance sheet to tame inflation. In December, the Bank of England unexpectedly raised interest rates, making it the world's first major central bank to do so in the aftermath of the COVID pandemic. While U.S. Treasury yields have risen across the curve in 2021, the U.S. Treasury yield curve is noticeably flatter compared to year-end 2020. Real yields (nominal yields less inflation) have been driven lower throughout the duration of the pandemic and are largely negative across U.S. Treasurys and U.S. corporate bonds. U.S. bonds continue to offer significant yield pick-up relative to foreign bonds, limiting upward momentum in U.S. yields even as the Fed moves toward tighter policy. U.S. Treasury yields have made a meaningful move upward to start 2022 as expectations for a more aggressive Fed have ratcheted up.

Inflation made new record highs in the fourth quarter

Although inflation was not a major headwind for risk assets in 2021, it merits continued monitoring by investors and policymakers. A re-opening growth bounce following lockdowns was widely anticipated, but 2021’s inflation surge was a genuine surprise for many. Last April, economists thought inflation would currently be around 2.5 percent; instead, CPI inflation reached 6.8 percent in November, a 40-year high. Explanations for the overshoot are two-fold: excessive stimulus artificially boosted demand, while pandemic-battered supply chains faced widespread bottlenecks.

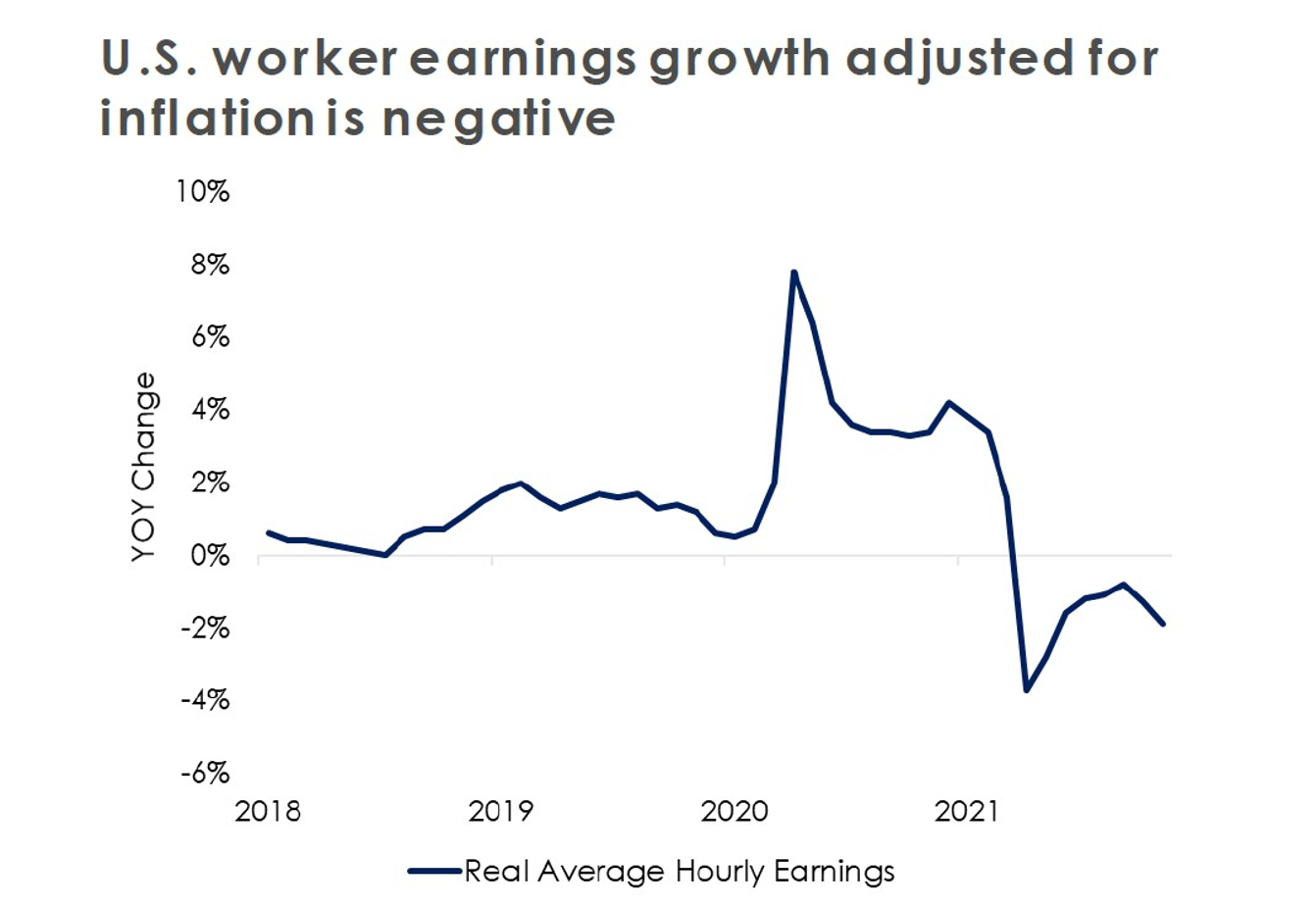

Source: Bloomberg as of Dec. 31, 2021.

Although 2021 brought significant wage increases to the lowest earners, they also shouldered the heaviest burden of inflation. The U.S. worker appears to be falling behind, with average real hourly earnings down 1.9 percent versus 2020. The labor market is currently the tightest it has been in decades, influenced by factors such as early retirement and a lingering reluctance to go back to the workforce having driven what is perhaps a permanently lower labor force participation rate. As many temporary contributors to the spike in inflation continue to fade, wage growth bears significant watching due to its ability to drive higher prices and negatively impact corporate profit margins. Rents, a significant component of CPI, also continue to climb reaching a post-pandemic high in November.

2022 outlook

2022 marks the next stage of the COVID recovery and a notable shift in policy support for the economy and financial markets. Omicron has caused some volatility, but like Delta, is proving to be more of a speed bump than a roadblock. It is certainly causing disruptions, but early indications that is it less severe and leading to fewer deaths and hospitalizations are encouraging. U.S. economic and corporate earnings growth are set to moderate at the same time the Fed begins tightening policy, which could create a challenging backdrop if there is any type of “growth scare” in 2022. Earnings and valuations will remain extremely important, especially as unprecedented support from the Fed and U.S. government fades.

Furthermore, the future of the Biden administration’s Build Back Better spending plan remains somewhat uncertain, and the U.S. will not see anywhere near the amount of fiscal stimulus it received during 2020 and 2021, which amounted to around 25 percent of GDP. Some stem from concerns over the growing U.S. deficit and debt. The U.S. budget deficit totaled $2.8 trillion in 2021, the second highest annual deficit on record, exceeded only by the $3.1 trillion deficit for 2020. Meanwhile, total U.S. national debt currently sits at $29.6 trillion or about 127 percent of U.S. GDP. Furthermore, with the U.S. remaining extremely divided politically, the 2022 mid-term elections will be a closely watched event and could impact the market to the extent the results influence future fiscal policy and corporate earnings.

Contrary to our initial expectations, we did not see changes to corporate tax rates passed in 2021, which likely played some role in boosting stock prices and equity markets in the fourth quarter. Lastly, we would not discount geopolitical risks as having the potential to disrupt markets in 2022. A potential invasion of Ukraine by Russia would be met with significant sanctions and potential risk-off in markets while China remains a source of uncertainty between threats to Taiwan, ongoing tensions with the U.S., and government intervention with certain companies and sectors. We look forward to continuing to support you in navigating complex and ever-changing markets in 2022.

Discover more from MassMutual …

Investing basics: What everyone should know

5 ways to prepare for an economic downturn

Income tax diversification defined

1 Commodities = S&P Goldman Sachs Commodity Index; REITS = Vanguard Real Estate ETF; Value = iShares Core S&P U.S. Value ETF; Mid Cap = Vanguard Mid-Cap ETF; Large Cap = Vanguard Mega Cap ETF; Growth = iShares Core S&P U.S. Growth ETF; Small Cap = Vanguard Small Cap ETF; Developed Markets = Vanguard FTSE Developed ETF; TIPS = iShares TIPS Bond ET; Emerging Markets = Vanguard FTSE Emerging Markets ETF; Aggregate Bonds = iShares Core Aggregate Bonds ETF; Gold = SPDR Gold Shares.