As we conclude the third quarter of 2024, the economy continues to grow steadily, yet the balance of risks is shifting. Small cracks have begun to emerge in consumer sentiment, manufacturing, and within the labor market. Employment has now overtaken inflation as the Federal Reserve’s primary concern within its dual mandate as progress on disinflation has been satisfactory, thus paving the way for the Federal Reserve to join the global monetary easing cycle.

Despite some bumps along the way, the 2024 equity market rally remains intact. The healthy broadening out of the market beyond the mega-cap “Magnificent Seven” and “Fabulous Four” companies, has thankfully materialized. Risk assets were broadly supported by ten-year U.S. Treasury yields falling firmly below 4 percent, although interest rate volatility reached some of the highest levels of the year.

It was a quarter of tail-risk events: There were two assassination attempts on former president Donald Trump, Japanese stocks had the worst crash since 1987, before promptly rebounding, military conflict continued to escalate in the Middle East, and Hurricane Helene ravaged the Southeast, as one of the deadliest hurricanes to make landfall on the U.S. mainland in recent history. With the election around the corner in November, we anticipate elevated volatility persisting into the foreseeable future.

Source: Bloomberg as of Sept. 30, 2024.1

Economy

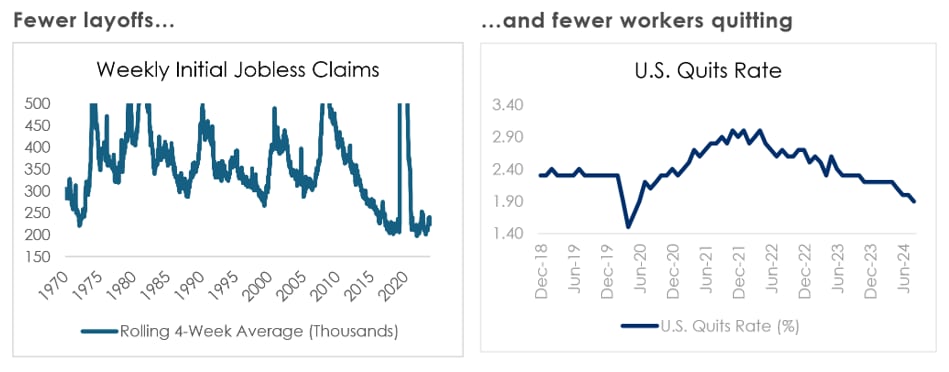

Unemployment has drifted higher in recent months, to 4.2 percent in August, versus the cycle low of 3.4 percent just over a year ago. Although there is no widespread discussion about layoffs, the labor market's advantage for workers has weakened, and the U.S. continues to produce fewer new jobs. Nonfarm payrolls increased by 142,000 jobs in August after a downwardly revised 89,000 rise in July, which was the smallest gain since an outright decline in December 2020. Additionally, the nature of the new jobs raises concerns, as government positions account for one in every five jobs created so far this year.

A general sense of unease has grown in the labor market, with a palpable tension between the old versus the new post-pandemic economy. The quits rate, or the percentage of people who voluntarily leave their jobs, was 1.9 percent in August, the lowest since June 2020. There is notable resistance to automation, with unions seeking to ban artificial intelligence (AI), leading to persistent strikes and upward pressure on wages. The International Longshoremen’s Association (ILA) brought the first large-scale eastern dockworker strike in 47 years, effectively halting the movement of between 43 percent-49 percent of all U.S. imports and billions of dollars in trade monthly through the U.S. East Coast and Gulf ports. In addition to a 77 percent pay hike over the six-year contract, the union’s primary demand concerns preventing certain automation at the ports. Notably, a survey conducted by Duke University this summer found that more than half (61 percent) of large U.S. firms plan to use AI within the next year to automate tasks previously done by employees.

Where we find comfort is in the overall growth rate of the U.S. economy, recently revised higher yet again to a 2.6 percent annualized GDP growth rate expected for full-year 2024. Headline inflation (as measured by CPI) has come within striking distance of the Federal Reserve’s target, now 2.5 percent. Similarly, we look to initial jobless claims, a leading economic indicator. Despite a prevailing sense of malaise among workers, initial jobless claims continue to decline, with the number of Americans filing new applications for unemployment benefits at a four-month low in September. At the same time, the observed rise in unemployment can be largely attributed to an increase in the labor supply, as we highlighted in our last update.

Source: Bloomberg as of Sept. 30, 2024.

Global equities

The S&P 500 finished the third quarter at yet another new all-time high. The corporate backdrop remained healthy, and S&P 500 companies saw 11.3 percent year-over-year earnings growth for the second quarter, the highest level since the final months of 2021. This performance might lead to beliefs that recessionary fears have been quelled, yet uncertainty still looms. Beyond the initial 50 basis point interest rate reduction in September, an additional eight 25 basis points cuts are expected by the end of 2025. A rapid easing cycle, typically a sign of economic weakness, feels at odds with predicted earnings growth of 15 percent for the S&P 500 in 2025, which would imply the highest earnings per share ever for the S&P 500 at roughly $280/share.

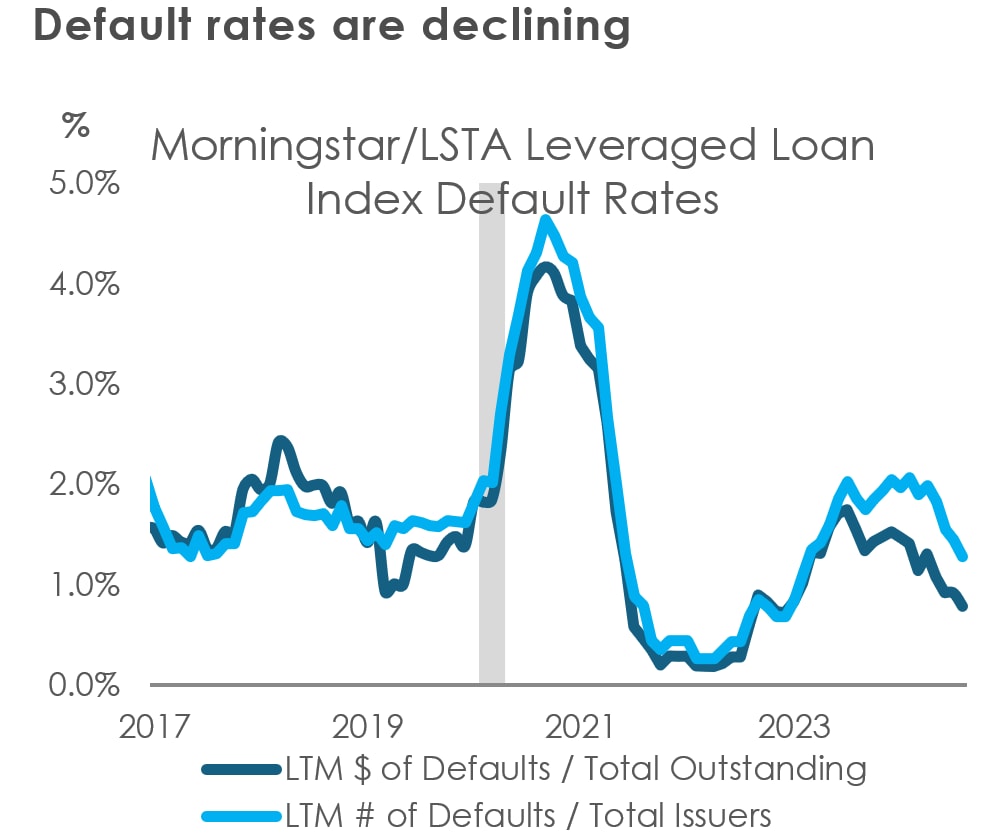

Amidst the conflicting narratives, something we like to keep in mind is the following: there have been five instances in the past forty years where the Federal Reserve eased monetary policy without an imminent recession following. In those cases, the average return in the 12 months following the first cut was 17 percent. Secondly, over 80 years, the stock market has a flawless track record: whenever it hits a new all-time high, the economy has never been in a recession. Fortunately, we made a new all-time high 47 times in the first three quarters of 2024 and 6 times in September alone. Similarly, history would suggest that if we were in a recession, default rates should be climbing. Yet the Morningstar Leveraged Loan Default Index suggests defaults are actually decreasing in 2024. In August, the default rate was 0.8 percent, down from about 1.5 percent at the start of the year, and it's the lowest since December 2022.

Source: Bloomberg as of Sept. 30, 2024.

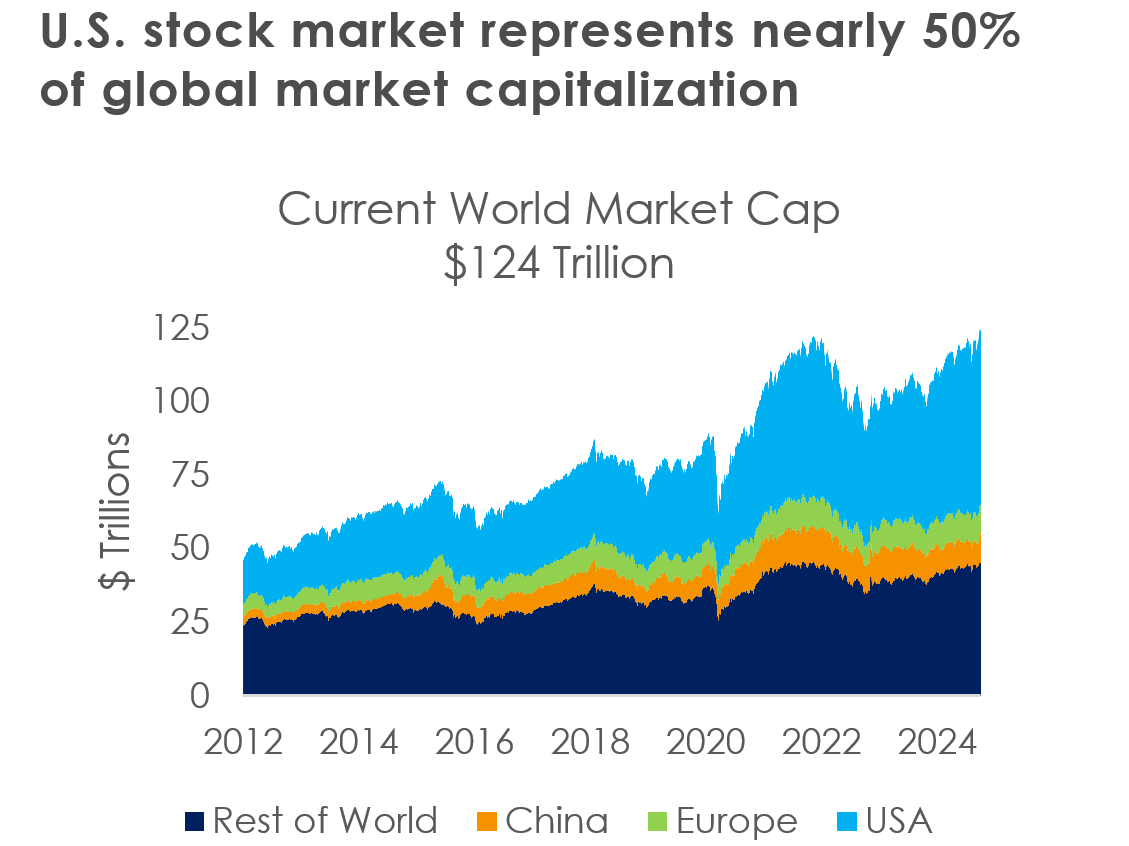

Looking globally, U.S. economic exceptionalism is forecasted to continue as seen in 15 percent earnings growth expectations. The U.S. is home to some of the most innovative companies in the world, and they defy expectations on a regular basis. Of the $124 trillion of global equity market cap, U.S. companies represent 48 percent, despite our population representing only 4 percent of the world population. Abroad, Europe remains in an era of secular stagnation. It faces numerous headwinds within the automotive sector, which represents nearly 7 percent of GDP, while also lacking the benefits of a booming technology sector. Farther east, following the unveiling of a massive stimulus package, Chinese equities, proxied by the CSI 300, gained 16 percent in the final week of the quarter—the biggest weekly gain since 2008. However, China's market volatility is significant, with the index showing an average annual intra-year correction of -30 percent and only a +1 percent annualized return since late 1992, compared to the S&P 500's 10.6 percent return. Furthermore, we find the opportunity less compelling due to a regulatory climate proven harsh to investors. We continue to prefer markets characterized by a high level of transparency and requirements for audited financial statements for public companies.

Source: Bloomberg as of Sept. 30, 2024.

The global easing cycle begins

Despite a strong economy in the U.S., an initial 50 basis point interest rate cut in September served as a “recalibration”, or a safeguard against potential downturns. Most economists and market participants alike pin estimates of the neutral rate about 150 basis points below the current policy, implying that policy is still quite restrictive. Elsewhere, the European Central Bank (ECB), cut interest rates for the second time in September. China unveiled a massive stimulus package in September to jumpstart its beaten down economy. The People’s Bank of China (PBoC) announced an unprecedented policy involving three simultaneous rate cuts: a 20-basis point policy interest rate cut, a 50-basis point reduction in banks' reserve requirements, and a 50-basis point cut in existing mortgage interest rates, further accompanied by a liquidity injection into the stock market.

Falling interest rates come as welcome relief to issuers of debt, namely the Treasury; U.S. national debt has surged to over $35 trillion and is increasing at a rate of about $1 trillion every 6 months. 2024 will witness nearly a $2 trillion deficit, despite record tax revenues. Interest payments alone will consume approximately 13 percent of the budget. Regardless of the outcome of the November election, what we know for certain is that neither candidate is running on a policy of austerity. Former President Donald Trump has pushed proposals to impose tariffs, cut taxes and restrict immigration, while Vice President Kamla Harris has proposed large tax increases and price-control measures. Outsized government spending is likely to continue under either administration.

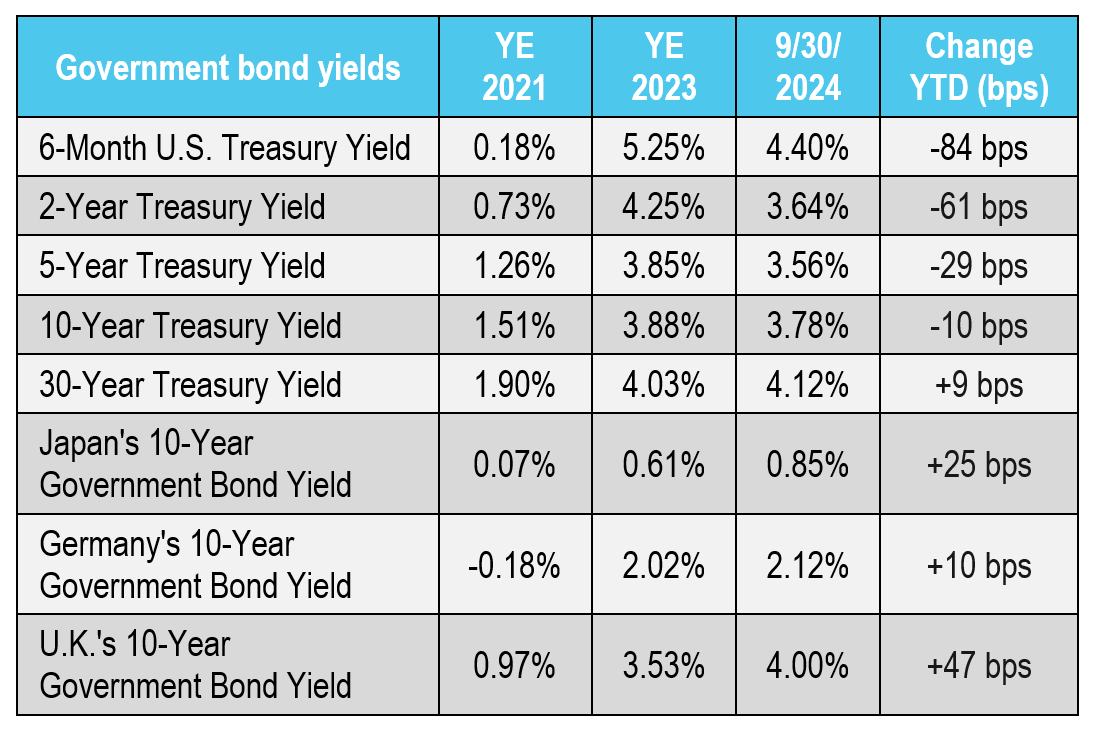

Bond markets are accepting this risk as they are not yet demanding compensation in the form of higher yields. In the third quarter, U.S. Treasury yields fell significantly across the board: two-year yields dropped by 115 basis points, five-year yields by 84 basis points, and ten-year yields by 62 basis points. Despite a brief uptick in August, credit spreads for Investment Grade and High Yield bonds remain well below their historical averages, standing at 95 basis points and 310 basis points, respectively, compared to the historical norms of 148 basis points and 520 basis points. Desire for credit compensation is low and fundamentals appear to be consistently healthy.

Source: Bloomberg as of Sept. 30, 2024.

Looking ahead

As we approach the final months of the year, we are on the cusp of resolving the most significant uncertainty that has affected the market in 2024. The divergent potential policy paths post-election suggest that some investors may adopt a cautious stance as November 5th nears. We find reassurance in the strength of the U.S. economy. U.S. companies continue to perform well, although valuations are stretched, with a forward 12-month price-to-earnings multiple for the S&P 500 at 21.6 times.

It is not clear that a slowdown or recession is the next phase, given that we are not in a typical economic cycle but are instead transitioning to a post-pandemic normal. The ongoing adjustments include significant supply shocks in the labor market and an immigration boom which has exerted downward pressure on wage inflation. With inflation decreasing, growth remaining stable, and central banks easing monetary policy globally, a soft landing appears to have been achieved.

_________________________________________