| ||||||||||||

Knowing how to shop for a mortgage is an important skill. It will not only help you get the loan you need to buy or refinance a home, but also help you feel confident about getting the right deal for your circumstances.

Shopping for a mortgage can seem overwhelming. But by breaking down the process into several smaller steps, the task can be manageable and a home closing achievable.

Calculate what you can afford

If you apply for a mortgage without analyzing your finances, you might get in over your head. Lenders don’t try to approve loans borrowers can’t afford, but they also don’t understand your personal finances as well as you do.

“Before you even begin shopping for a mortgage, it's important to set a home-purchase budget,” said Andrea Woroch, a nationally recognized consumer finance expert. “Figure out what you can comfortably afford to spend every month based on your monthly budget. Aim to spend no more than 25 to 30 percent of your take-home pay on housing.” (Related: How to put together a budget)

Learn your credit score

Credit reporting mistakes can lower your score through no fault of your own. And mistakes can hurt your chances of qualifying for a mortgage or getting the best rates.

“Pull copies of your credit reports from all three credit bureaus at annualcreditreport.com to make sure everything is accurate,” said Greg McBride, senior vice president and chief financial analyst at Bankrate.

Follow the credit bureau’s dispute resolution process if you find an error. In some cases, you might need to contact your creditors for help.

As for your scores, you’ll want to turn to another source to avoid paying for them. You can get your scores from all three credit bureaus through various free services, such as Credit Karma and WalletHub. These scores might be different from the scores mortgage lenders use, but you’ll get a general idea, at least.

If your score is lower than 740, which is considered very good, take steps to improve it. Try paying down credit card balances and ensuring you make every payment on time. Amounts borrowed and on-time payment history are two of the biggest components of your credit score. (Related: Improving your credit score: It pays off)

“The better your credit, the more likely you are to get approved for a mortgage with the best loan terms and lowest interest rate,” Woroch said. (Learn more: How interest rates work)

Research mortgage types

Different mortgage types are best suited to different borrowers, often depending on their credit score and how much of a down payment they can muster. (Related: How to put together a house down payment)

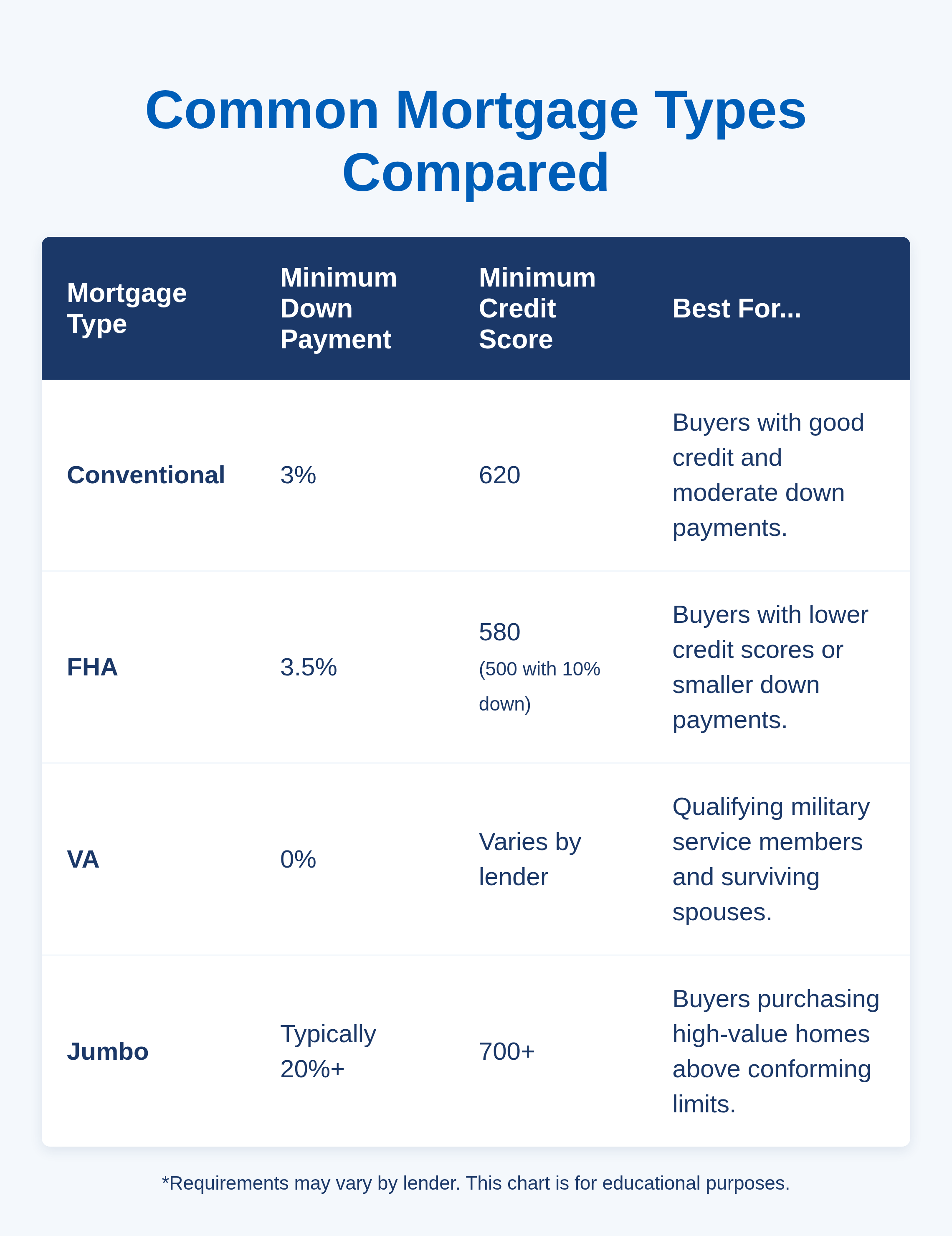

Here are the main categories:

Here’s more about each category

- Conventional: This is a popular mortgage type available to homebuyers who can put down at least 3 percent, have a credit score of at least 620, and have a debt-to-income ratio of no higher than 50 percent. Borrowers with less than 20 percent down often have to pay private mortgage insurance premiums.

- FHA: This is a government-backed mortgage for homebuyers with a credit score of at least 500 and 10 percent down or a credit score of at least 580 and 3.5 percent down. FHA mortgage insurance can make these loans pricey.

- VA: This is a government-backed mortgage for qualifying military service members and surviving spouses. These loans require nothing down and have a VA funding fee but no mortgage insurance.

- Jumbo: A loan for well-qualified buyers who want to borrow more than $832,750 in most locations and more than $1,249,125 in high-cost areas. These are the conforming loan limits for 2026, as outlined by the Federal Housing Finance Agency.

“While there are plenty of low-down-payment and homebuyer assistance programs for homebuyers, these are limited to conforming loan amounts and sometimes even low- and moderate-income buyers,” McBride said. “Homebuyers looking at larger jumbo loans will need to make a more significant down payment — oftentimes, 20 percent or more — to secure the best terms and will need a similar equity cushion if refinancing.” (Learn more: How to refinance your mortgage)

Evaluate mortgage loan terms and lengths

You have different options for how long you can take to repay your loan, and each has its pros and cons.

- 30-year fixed rate: You’ll pay the same interest rate for 30 years. Your monthly payment might be lower than other types of mortgages, like adjustable rate mortgages (ARMs), but the interest rate could also be higher than other types of mortgages, and you’ll spend more on interest in the long run.

- 15-year fixed rate: You’ll pay the same interest rate for 15 years. Your monthly payment will be higher than, say, a 30-year mortgage, but your interest rate will be lower, and you’ll save a lot on interest in the long run.

- 5/1 ARM: You’ll pay the same interest rate for five years. That rate will usually be lower than the 30-year fixed rate, but higher than the 15-year fixed rate. After the first five years, your interest rate will adjust up or down once a year for the next 25 years. The adjustment will bring your rate in line with prevailing rates in the mortgage market. So, if interest rates go up substantially, you could end up paying a rate higher than what you could have locked in with a fixed-rate mortgage. (Learn more: Pros and cons of an adjustable-rate mortgage

The 30-year fixed is the most popular mortgage. If you’re on the fence, it’s a solid choice because your monthly payment will typically be lower, giving you more breathing room in your budget.

A borrower can also cut interest costs by paying down a mortgage loan balance faster.

Get quotes from several lenders

“When taking out a home loan, it's important to shop around to find the lender with the best mortgage loan terms and lowest interest rates,” Woroch said. “Interest rates can vary by as much as 1 percentage point between lenders, and that's a lot of money if you miss out on a lower rate.”

Getting quotes from at least five lenders could, in fact, save you thousands of dollars.

You might be wondering if applying for a mortgage over and over will hurt your credit score. Normally, applying for loans and credit cards does lower your score by a few points. But all the home loans you apply for within a 45-day period will count as a single loan inquiry on your credit report and will barely affect your score.

“Not shopping around is the most common mistake among homebuyers and refinancers alike, oftentimes, just going with the recommendation of their real estate agent, a friend, or sticking with their current lender,” McBride said. “This mistake can cost thousands of dollars over time.”

With thousands of lenders in the United States, you probably have more options than you think. They include mortgage bankers, retail banks, mortgage brokers, direct lenders, and more.

“If you have unique circumstances that prevent approval under traditional mortgage programs, cast a wider net — including credit unions, local community banks — and even your asset management firm or your financial planner may have recommendations,” McBride said. “A portfolio lender that holds the loans they make rather than selling them to investors will have more flexibility to tailor a solution to your needs.”

Connect with a MassMutual financial professional

Compare mortgage loan estimates

A loan estimate is a three-page form that mortgage lenders must use to show you the interest rate and fees they’ll charge you for a mortgage. Loan estimates make it easy for borrowers to compare one lender’s terms to another. Besides the interest rate, you’ll want to look at the closing costs, especially the ones you cannot shop for. Closing costs typically range from 2 percent to 5 percent of the loan amount.

You’ll get the most accurate comparisons if you apply for the same type of loan with each lender.

At this point, you may want to consider the additional cost of life insurance, particularly if you are buying a house with a spouse or partner. Life insurance can help cover financial obligations, like a mortgage, if a major breadwinner unexpectedly passes away. If you are young, like most first-time homebuyers, life insurance costs can be relatively low. (Related: 4 times term insurance may be the answer)

Choose your mortgage lender

Interest rates and fees will play a big role in selecting which lender to work with. Also, take a look at mortgage insurance costs, the lender’s reputation, and the customer service you’ve received so far. And ask the lender what their turnaround time is to close a mortgage, especially if you’re close to buying. Once you find the home you want to purchase, it can be a major inconvenience to both you and the seller if the loan isn’t finalized within your planned time frame.

Lock your mortgage rate in

Once you’ve chosen a lender, you’ll need to decide when to lock your interest rate. Locking your rate means solidifying what your monthly payment will be. It also means that any increase in rates before you close won’t disqualify you or force you to increase your down payment. Once you’ve locked, you’ve usually lost the possibility of paying a lower rate, but at some point, you have to take what you can get and be comfortable with it.

Getting a formal mortgage preapproval gives you a realistic budget and shows sellers you are a serious buyer.

Conclusion

By calculating what you can afford, learning about the different mortgages, and getting quotes from several lenders, you’ll be in a strong position to help get the best loan for you.

It’s an important decision, but one you’re capable of making with a little research and effort.

________________

Frequently Asked Questions about shopping for a mortgage

Q. What are typical mortgage closing costs?

A. Closing costs generally range from 2 percent to 5 percent of your total loan amount. These fees cover appraisals, title searches, origination fees, and other administrative expenses.

Q. What credit score is needed to buy a house?

A. You typically need a minimum credit score of 620 for a conventional mortgage, though FHA loans may accept scores as low as 500 with a larger down payment. A score of 740 or higher will generally secure the best interest rates and loan terms.

Q. Should I get a 15-year or 30-year mortgage?

A. A 30-year fixed-rate mortgage offers lower monthly payments, giving you more budget flexibility. A 15-year mortgage has higher monthly payments but a lower interest rate, saving you thousands in interest over the life of the loan.

____________________

Discover more from MassMutual…

Budgeting and building your financial pyramid

Buying a house: What millennial homebuyers want

__________________