| ||||||||||||

It’s tempting to begin claiming Social Security benefits at the earliest opportunity — age 62 — and many Americans do just that. But is it wise?

Taking benefits before you reach your full retirement age can have a negative impact on you, your spouse, and on survivors benefits later on because it permanently reduces the size of your monthly benefit.

Yet, if your savings account is lacking or your health status is vulnerable, it might make sense to start taking benefits as soon as possible. Indeed, determining when you should file for Social Security benefits all depends on your unique financial picture.

“It is hard to make ‘one-rule fits all’ generalizations about taking your Social Security benefits,” said David Freitag, a financial planning consultant for MassMutual. ”Because we are all different, each Social Security decision could and should be custom made, like a fine suit or custom dress.”

To make an informed decision, he said, it’s important to understand how Social Security benefits work.

It’s also important to plan ahead so you don’t outlive your savings. If you hope to delay claiming benefits, for example, you will need sufficient assets and a safe withdrawal strategy from resources such as your IRA, taxable brokerage accounts, pensions, and annuities to cover your living expenses until Social Security kicks in.

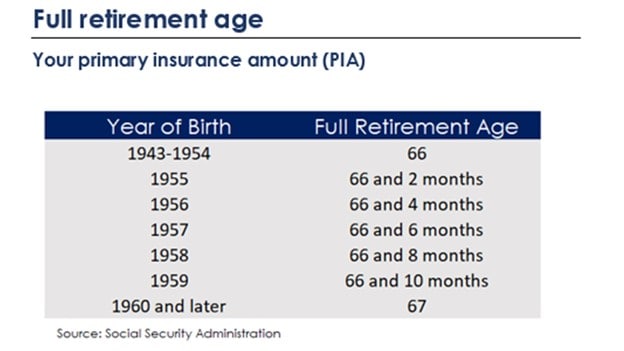

When can I file for Social Security?

You can start by determining your full retirement age, the age at which you are entitled to receive full (or unreduced) Social Security retirement benefits if you have earned enough credits during your working years. Your full retirement age is based on the year you were born. (Learn more: What to do with your RMD? 5 possibilities)

If you begin collecting Social Security before your full retirement age, your benefit amount will be reduced by a percentage that reflects the number of months until your full retirement age. That can seriously undermine one of your most significant sources of guaranteed retirement income.

For example, if you were born in 1960, your full retirement age is 67. You can opt to begin collecting Social Security benefits at age 62, but your monthly benefit will be reduced by 30 percent because you might be collecting benefits for an additional five years. If you start collecting at age 65, your benefit will be reduced by 13.3 percent.1

Conversely, your benefit will increase by a fixed percentage for each year you delay claiming Social Security beyond your full retirement age.

For example, if you were born in 1943 or later, your benefit would increase by 8 percent per year for each year you delay claiming benefits beyond your full retirement age until you turn 70, when the benefit of delaying any further disappears.

Delaying Social Security, if you can afford to wait, is one of the most effective ways to boost your guaranteed retirement income, which is especially important if you have under saved.

It can also potentially benefit your spouse, especially if he or she earned less than you (or nothing at all) in the workplace. How? Your spouse is entitled to spousal Social Security benefits while you are alive based on either his or her own earnings history or 50 percent of your Social Security benefit — whichever is greater. By waiting to claim benefits until beyond your full retirement age, you help to increase the size of the Social Security check your spouse may one day receive. (Related: Understanding Social Security benefits for spouses)

Such a strategy also protects the surviving spouse in the event of death. By waiting to start benefits beyond your full retirement age, you can potentially position your spouse to receive a bigger survivors benefit than he or she would have received had you filed earlier.

A recent MassMutual Social Security Pulse Check survey found that many who file for Social Security retirement benefits early or even at their full retirement age later regret not holding out for a bigger benefit. About 30 percent of respondents filed at age 62 or younger, and nearly four out of 10 (38 percent) of them wished they had waited.

Some indicated that they filed when they did because they had under saved and could not afford to wait, while others needed the monthly income to cover medical bills, a loss of employment, or other unforeseen expense.

Longevity is a wild card

As you ask yourself ‘when do I apply for Social Security,’ however, be aware that there are certain scenarios in which it might make sense to claim benefits early. For example, retirees who lost their job or experience a financial hardship may be forced to collect benefits at the earliest opportunity. Financial professionals typically recommend that older adults work a few extra years to increase their savings and delay claiming Social Security benefits, but that isn’t always possible. (Related: What's your plan for living longer?)

Those who are otherwise financially secure, said Freitag, may also wish to take benefits early to divert that income into legacy giving programs for children, grandchildren, or charities. “There are powerful ways to leverage Social Security income to create new capital,” he said. “This new capital can then be used to really change the quality of life for those in need.”

Indeed, the most important point about filing for benefits is to be deliberate.

“Wise Social Security drawing strategies can make a big difference,” said Mark Wilson, a financial professional with MILE Wealth Management in Irvine, California, in an email interview. “Most folks are simply claiming as soon as they can and this might cost them tens of thousands of dollars over their lifetimes. Unfortunately, these strategies are not straightforward and usually involve ‘running the numbers.’”

The other big variable where Social Security claiming strategies are concerned is longevity. Although it’s impossible to predict for sure how long you will live, your current health and family history can provide general guidance. So, too, can government data.

According to the Social Security Administration:

- A man reaching age 65 today can expect to live, on average, until age 78.1. A woman turning age 65 today can expect to live, on average, until age 80.9. 2

- And those are just averages. About one out of every four 65 year-olds today will live past age 90, and one out of 10 will live past age 95.

The Social Security Administration life expectancy calculator provides estimates based on age and gender assumptions. Just remember those estimates reflect “averages.” Your own lifespan may be longer or shorter than average.

Those with a medical condition that may shorten their life expectancy may collect more in Social Security if they claim benefits before their full retirement age.

Life expectancy

For perspective and perhaps inspiration, it helps to calculate your break-even point, which is effectively the age at which you will have collected more in Social Security by delaying benefits than you would have collected had you started claiming early. The AARP’s Social Security Benefits Calculator can help.

Remember, however, that such calculations are imperfect. More importantly, they fail to account for the time value of money. If you don’t need your Social Security checks to live on, you could potentially invest those dollars and generate earnings.

Social Security provides one of the only sources of inflation-protected retirement income for retirees. As such, it is too important for guesswork.

“Social Security is the foundation of retirement security, offering protection against longevity risk and inflation risk,” said Marguerita Cheng, a financial professional with Blue Ocean Global Wealth in Potomac, Maryland.

As you plan ahead, take the time to set up your own “My Social Security” page on www.socialsecurity.gov. This is an easy and secure way to view your estimated benefits and earnings history. The Social Security Administration will use this information when it calculates your benefit, so be sure that it accurately reflects your work history. (Related: Why you need Social Security’s Blue Bar Report)

The age you are when you apply for Social Security benefits has a big impact on the size of your future benefit for yourself and your household.

To determine a strategy that’s right for you, carefully consider your personal savings, spouse’s retirement income needs, health, and family medical history. And, as always, talk with a financial professional who can help you make the right decision.

Discover more from MassMutual…

What people don’t know about Social Security, but should

Rebuilding retirement savingsNeed a financial professional? Find one here

This article was originally published in April 2018. It has been updated.

__________________________________________

1 Social Security Administration, “Starting Your Retirement Benefits Early.”

2 Social Security Administration, "Period Life Expectancy – 2022 OASDI Trustees Report.”