One of the most important aspects of retirement planning is preparing for the possibility of needing long term care (LTC) or extended care. Yet, findings from The MassMutual Long Term Care in America Study show that few people believe they will need long term care or prepare for it.1

MassMutual recently commissioned the study of consumers to better understand how they view long-term care, particularly the financial and emotional aspects. The study probes the need for LTC and the dynamics of why many people simply avoid addressing the likelihood of needing care in retirement. We hope the study’s findings help you understand the consumer’s view of extended care and help you better prepare for the possibility as part of your retirement planning.

As way of background, LTC is typically defined as a variety of services and support to help people with everyday tasks, also called Activities of Daily Living (ADLs) over an extended period of time.

ADLs include:

- Bathing

- Dressing

- Eating

- Using the toilet

- Caring for incontinence

- Transferring

The need for long term care can be a life-changing event, impacting the financial, emotional and physical well being of both you and possibly even your caregiver, who is often an immediate family member or members.

And new challenges create even greater pressure on seniors today. The changing makeup of families, such as being smaller and more geographically dispersed, means there may be fewer familial resources to fall back on.2, 3, 4

In many people’s minds, long term care is something that only happens to someone else. MassMutual’s research found that merely 15 percent of those surveyed believe suffering an LTC issue is extremely or very likely. The reality is that 70 percent of adults who live to age 65 will need long term care in the future, the U.S. Department of Health and Human Services reports.5

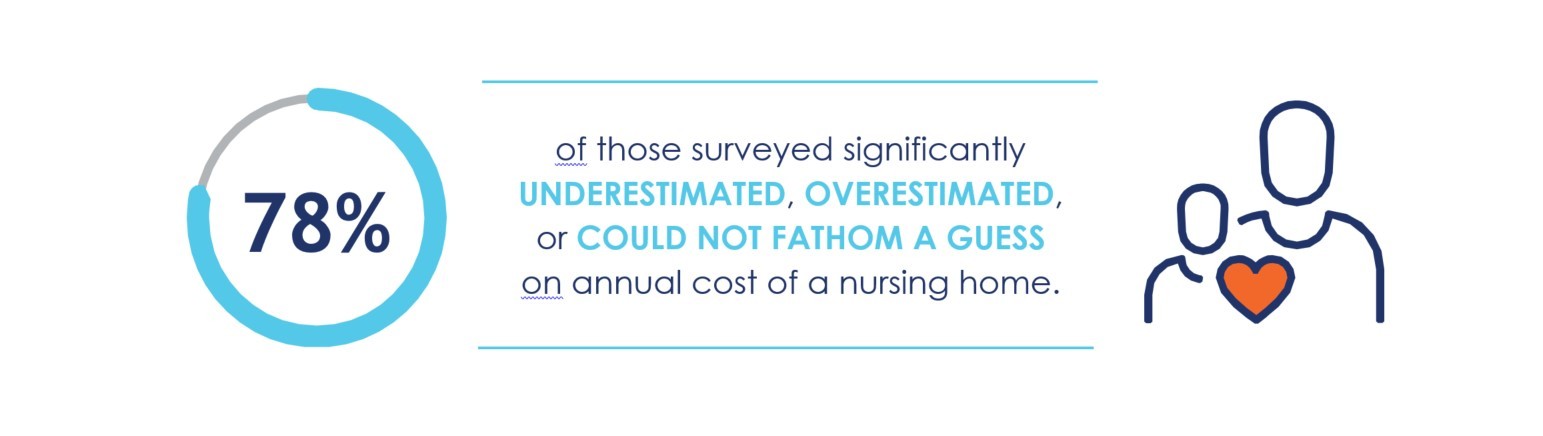

And we also see that even fewer people understand the costs of extended care. Nearly four in five (78 percent) of survey respondents underestimate, overestimate or cannot guess the annual cost of nursing home care, according to the study. This knowledge gap leads to a lack of confidence in the ability to pay for extended care.

Be sure to ask your financial professional questions about the risk of needing extended care and the impact to your retirement savings, the costs for care in your area, and what options you may have to help cover those costs. Each person’s situation is different, typically influenced by variables such as relative health, age, personal finances, desired retirement age, family situation and many other planning questions. A knowledgeable financial professional can also help take the emotion out of the decision and explain why the likelihood of living a long life may require the need for extended care.

You have worked and saved for an enjoyable retirement, for your well-being and the well-being of your loved ones, be prepared to protect your retirement savings with a plan to protect you from potential extended care costs. Please take the time to discuss extended care with your financial professional.

Discover more from MassMutual ...

6 types of people who dismiss LTC, but shouldn't

Keeping caregiver costs contained

Planning for diminished mental capacity as you age

____________________________________

1 MassMutual Long Term Care in America Study. Study Conducted by Greenwald & Associates. November 2019.

2 Genworth, “Cost of Care Survey 2004-2019.”

3 U.S. Census Bureau, “Current Population Survey: March and Annual Social and Economic Supplements.” Published 2019.

4 AARP, “Valuing the Invaluable: 2019 Update.”