| ||||||||||||

After a huge market downturn and a major loss of value in your investment portfolio, the temptation to do something — anything — may be hard to resist.

But in many ways, the best action may be to take no action. Why? An investment plan is a long-term project and making changes to it based on short-term considerations is often ill-advised. That’s why financial professionals encourage people to stay calm during market sell-offs and think about long-term objectives.

“It is a tough and scary time, and not locking in losses by panic selling is critical,” said J. Todd Gentry, a financial professional with Synergy Wealth Solutions in Chesterfield, Missouri.

But even if you did resist the initial impulse to flee during a market retreat, you still need to keep some discipline about your portfolio as you wait for a market recovery.

Here are some traps to avoid.

Chasing investment returns

Selling off your holdings in a market decline is the surest way to lock in losses. A solid investment that was doing well before an unforeseen setback — like a pandemic, war, natural disaster, or financial crisis — can still make a comeback. But if you sell at the bottom, you miss the chance at recovery.

And trading that solid investment for something that appears “hot” can also be unwise, as you might be buying after it has already made its significant gain.

“Don’t chase returns,” said John Ocwieja, a family business specialist with WestPoint Financial Group in Chicago. “And never sell your holdings on a downswing in the market when you are invested for the long term.”

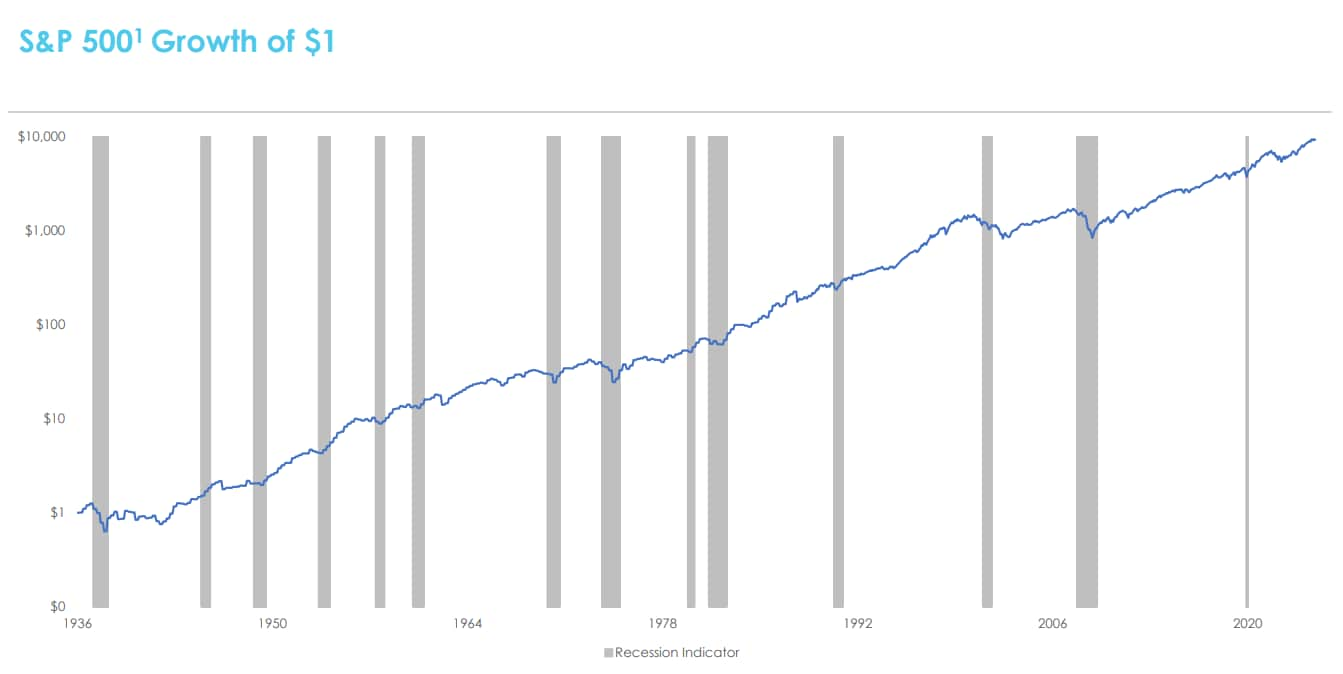

That’s particularly essential for holdings that are generally tied to overall market performance, like index funds. Markets, as a whole, have historically bounced back from downturns with time, as the following chart (showing the growth in $1 invested in a broad market index like the S&P 500) illustrates.

This isn’t to say that portfolios and investment holdings shouldn’t be periodically reviewed. But such reviews should be conducted with long-term objectives and asset allocation in mind. Often average investors, who don’t have the time or training to study individual investments in depth, consult a financial professional to help guide decisions.

Connect with a MassMutual financial professional

Market timing

Many people also try to time their buying and selling decisions based on predictions about market movements: buying right before they think the market will move higher and selling just before they suspect a market may move down.

This practice also can lead to unfortunate results, especially for the average investor. Professional stock traders and investment professionals often use in-depth research and statistical models to predict market movements, and yet still have inconsistent results. Indeed numerous studies, like this one, have found that attempts at market timing generally fall short.

For average investors, financial professionals typically recommend the opposite strategy, buy and hold. This is where an investor selects investments that are consistent with their risk profile and long-term objectives and keep their holdings for a number of years. Such a strategy can produce steady returns over time. Again, many people opt to consult a financial professional for help in selecting the appropriate investments. (Related: Preparing for volatility)

Fees, not earnings

Often, switching investments or changing holdings in your portfolio will result in an administrative fee or sales charge, which lowers your investment return.

Additionally, there may be specific fees for mutual fund investors, depending on the fund. Some mutual funds have early redemption fees in place to discourage short-term investing. Others may have what’s called back-end loads — essentially deferred sales charges to the fund’s broker.

The impact of such fees or transaction costs will depend on the level of activity and the size of the portfolio. For some investors, they could be inconsequential, while for others it may add substantially to investment costs. But all investors should consider them when contemplating changes to their investment mix. Needless or spur-of-the-moment changes could add to costs, possibly without adding much in the way of returns.

Additionally, there is the opportunity cost to consider. Money spent on fees is not earning a return as part of investment principal.

Conclusion

In the end, financial professionals will advise most people that investment moves should be thought out and made in conjunction with an overall financial plan. That includes planning for the future, as well as funds for the short term.

“I have been assuring people we are here and willing to discuss whatever they may need to consider to access liquid dollars to make it through any challenges,” said Gentry.

Discover more from MassMutual …

Understanding the basics of investing

The three keys to choosing your investments

This article was originally published in March 2020. It has been updated.

____________________________