| ||||||||||||

Summer is the perfect time for barbeques and beach parties, but it’s also a good opportunity to take the pulse of your saving and spending plan with a midyear financial checkup.

With the first half of the year in the rearview mirror, a quick look at your monthly budget can yield valuable insight into whether you are still on track to meet your yearly savings goals. It can also help identify areas of waste and provide motivation to set new goals. (Learn more: Setting savings goals)

“It is always a good idea to evaluate your financial situation at certain intervals,” said Greg Hammer, a financial professional with Hammer Financial in Schererville, Indiana, in an interview. “If you haven’t met with your financial professional since January, it’s good to check in midyear and take a deeper dive so we can assess whether your investments are still in line with your objectives.”

The midyear checkup serves another important function, as well: “If you’re in tune with your investments and in touch with your financial professional, you are less likely to panic when the market starts to correct,” said Hammer. “You are less likely to make emotional decisions that can negatively impact your returns.”

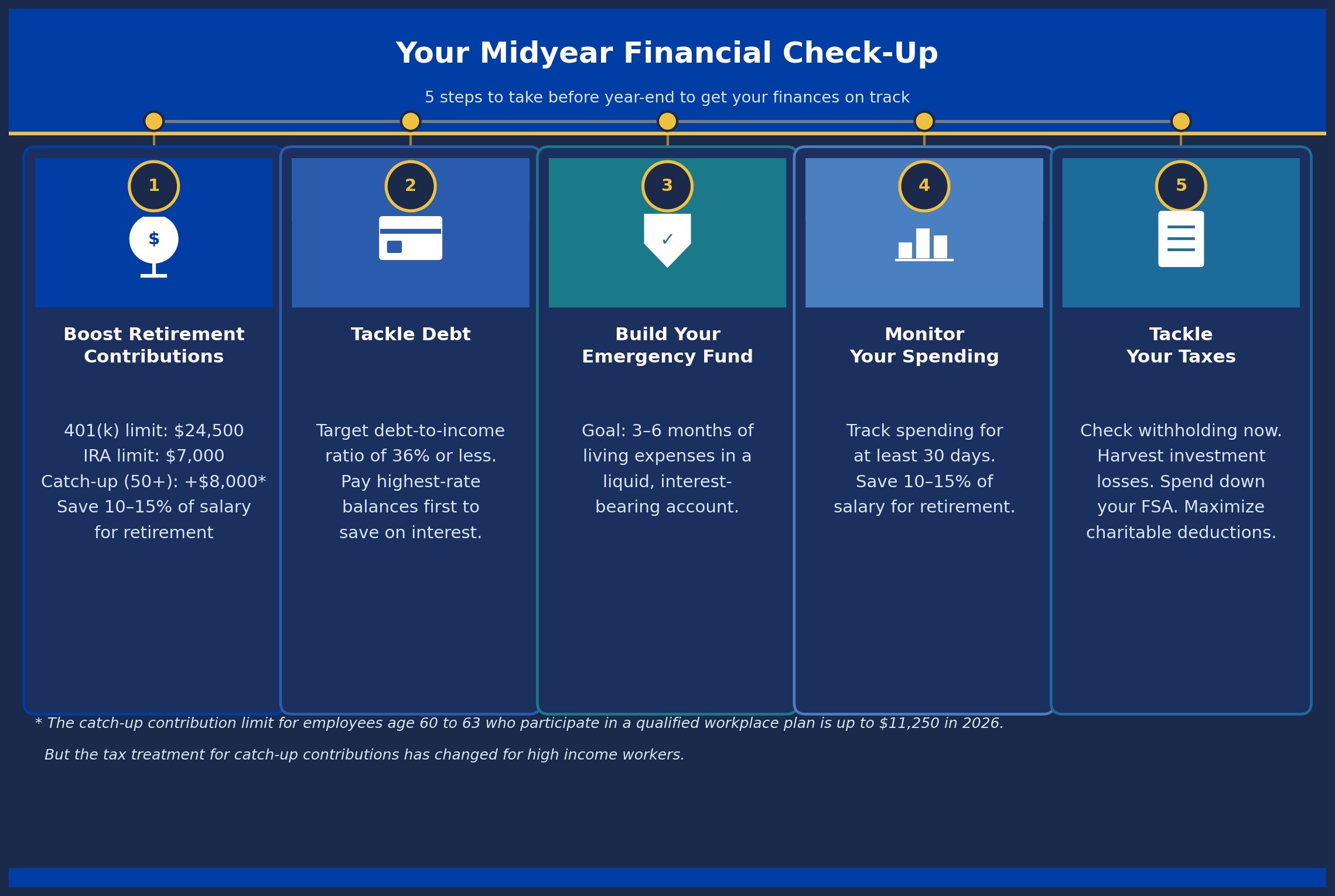

1. Check your retirement contributions: Should you max out your 401(k)?

Hammer suggests savers start by taking stock of their retirement plan contributions.

Savers should, at minimum, contribute enough to collect any employer match to which they are entitled, he said. Not doing so leaves free money on the table.

Ideally, you should aim to max out your tax-favored retirement plans, such as a 401(k) plan, 403(b), or traditional IRA, said Hammer, which not only helps to build your future nest egg, but also yields a valuable current-year tax deduction. Take note that Roth IRA contributions provide no tax break for contributions, but your earnings and withdrawals in retirement are generally tax-free.

Related:

The annual contribution limit for 401(k), 457(b), and 403(b) plans is $24,500 for tax year 2026, Those 50 and older may make an additional catch-up contribution of $8,000 in 2026...

Under a change made in recent legislation, however, employees aged 60 to 63 who participate in these plans can potentially make a higher annual catch-up contributions of up to $11,250 to a workplace plan in 2026. Be aware, however, that the tax treatment for catch-up contributions will change for certain workers in 2026. (Learn more: High earner 401(k) catch-up changes: What to know)

The total annual contribution limit for traditional and Roth IRAs in 2026 is $7,500.1 The catch-up contribution limit for IRAs isis $1,100.

If you don’t have the resources to meet the max, financial professionals often suggest looking for ways to reduce your current expenses. You can also potentially allocate any bonuses or raises you get going forward to your retirement account. Or, some financial professionals suggest increasing your contributions gradually by 1 percent of your salary per year until you reach your desired goal.

Even $200 per month starting at age 30 can amount to roughly $454,000 more in retirement savings by the time you reach age 65, assuming a 7 percent annual return.

2. Tackle debt

“The best way to save is by getting rid of debt,” Hammer said. “Is your debt level going up, declining, or unchanged from the start of the year? If it’s on the rise, you need to understand what’s happening with your financial situation and correct your spending pattern.”

Some debt, said Hammer, including student loans and home mortgages, are common and necessary, but credit card balances with double digit interest rates can cripple your budget, especially in a rising interest rate environment. Indeed, most credit cards have a variable rate, which means the percentage they charge consumers who carry a balance is tied directly to the Federal Reserve’s benchmark rate. (Related: Good debt vs bad debt)

“Debt is the worst possible thing to carry in a rising interest rate environment,” said Hammer, noting that paying down your debt will also help you improve your credit score which may reduce future borrowing costs. (Learn more: Handling debt)

Like many professionals, he suggests consumers with multiple credit card balances tackle the one with the highest interest rate first, while continuing to make minimum monthly payments on any others to avoid late fees. Once that debt is paid, move on to the next highest rate card until you are debt-free. Just be sure you don’t pay for any new purchases with plastic while you’re paying down your debt, he said.

Your debt level is an important metric in determining your “creditworthiness.”

For instance, the Consumer Financial Protection Bureau recommends maintaining a debt-to-income ratio of 36 percent or less for homeowners to qualify for favorable mortgage interest rates, although it acknowledges that some lenders will go up to 43 percent or more. For renters, the bureau suggests a debt-to-income ratio of 15-20 percent or less.2

To calculate your ratio, add up your monthly debt payments and divide that figure by your gross monthly income.

Connect with a MassMutual financial professional

3. How’s your emergency fund?

The mid-year check-up is also an opportune time to be sure your emergency fund is up to snuff, said Willie Schuette, a financial professional with JL Smith Group in Avon, Ohio, in an interview.

Many financial professionals recommend having three to six month's worth of living expenses set aside in a liquid, interest bearing account, such as a money market fund or savings account, for life’s little emergencies, but you may need up to a year’s worth of expenses socked away if you are self-employed, your job security is tenuous, or your family is dependent upon a single breadwinner, he said.

If you don’t have an emergency fund, or haven’t saved enough, no sweat. Set an attainable goal and start contributing monthly, while continuing to fund your retirement and pay down debt, until you reach your goal.

Here’s a closer look at how to build an emergency fund.

Depending on your circumstances, you might also consider using these sultry summer days to score a few income-earning gigs, such as housesitting, dog walking, helping people move, painting houses, having a garage sale, or selling bottled water (as permitted by local laws) at outdoor events. With a little creativity and hard work, you could potentially have a fully funded rainy day account before the cooler temperatures descend this fall. (Learn more: 6 summer gig ideas to make extra money)

4. Monitor your spending

If your debt level has been stagnant since January or you’re finding it tough to meet your savings goals, put the next lazy day to good use and get your budget under control.

The National Foundation for Credit Counseling suggests consumers, regardless of their financial position, track their spending for at least 30 days to get a better sense of where their money is going, highlight areas of waste, and establish better saving habits.3

“Write down every cent you spend, and then put your spending into categories,” the NFCC suggested in its guidelines on mid-year financial planning. “At this point you can make conscious decisions regarding how you want to spend moving forward.” (Related: Budget basics)

Look for opportunities to liberate cash flow by halting memberships in clubs you don’t use, slashing your cable bill, and swapping one trip per year for a staycation.

Remember, too, that your disposable income (or spending money) is what’s left over after you fund your long-term financial goals, such as saving for a down payment on a house and saving for retirement.

Many financial professionals recommend saving 10 to 15 percent of your annual salary for retirement. That’s easiest done by “paying yourself first” through automated deferrals at work.

If you are consistently unable to save what you need to secure your future, you may be living beyond your means, which means more drastic measures may be in order, including downsizing to less expensive housing.

5. Tackle your taxes

Most of us only pay attention to taxes in December, when it’s too late to implement many of the most effective tax-saving strategies. If you meet with your tax professional now, however, you can potentially still maximize deductions and prevent future penalties. (Related: Understanding tax diversification)

Specifically, financial experts and tax professionals routinely suggest taxpayers check their withholding to be sure they’re on track to pay what they owe and nothing more. Withhold too much and you’ll get a refund when you file your return next year, but you will also miss out on an opportunity to invest that money for compounded growth or use it to reduce your debt. By overpaying monthly, you effectively give the government an interest-free loan.

By contrast, if you owed money in prior years, financial professionals commonly suggest that you should consider reducing your withholding allowances now, which will result in a lower monthly paycheck but may result in either a slight refund or zero tax liability next spring. Ask your human resources department for a new W-4 form to facilitate the change.

Online calculators and tax preparation firms offer basic guidance on how many withholding allowances you may want to take to maximize your tax refund, or your take-home pay, but a tax or financial professional can provide personalized expertise.

Look, too, for opportunities to maximize charitable deductions, begin harvesting investment losses to offset current year capital gains, and spend down your Flexible Spending Account (FSA). FSAs are funded with pre-tax dollars and can be used to help pay for qualified medical and dependent care expenses, but any money not used by year-end gets forfeited. (Learn more: Saving for medical costs: FSA, HSA or both?)

“It’s a use it or lose it account so if you’re not about halfway through your account at this point in the year start looking for ways to ramp up your eligible spending by scheduling doctor’s visits and making vision appointments,” said Schuette.

Similarly, to avoid a current year penalty, self-employed individuals should be sure they’re making their required estimated quarterly tax payments, and are on track to pay either 90 percent of what they will owe for this year or at least as much as they owed last year, whichever is less.4

Conclusion

The year is still young for retirement savers, borrowers, and taxpayers who are serious about getting their financial house in order. By examining your finances or working closely with a financial professional, you can potentially use the remaining months of the year to maximize your 2023 tax deductions, eliminate debt, and develop a saving and spending plan that will help you meet both your short- and long-term financial goals.

_______________________________________

Frequently Asked Questions (FAQ) about mid-year financial checkups

Q: What is a mid-year financial checkup?

A: A mid-year financial checkup is a comprehensive review of your finances conducted halfway through the year. It involves assessing your budget, retirement contributions, debt levels, emergency fund, and tax strategies to ensure you remain on track to meet your annual financial goals.

Q: How much should I contribute to my 401(k) in 2026?

A: For 2026, the IRS contribution limit for a 401(k) is $24,500. If you are 50 or older, you can make an additional catch-up contribution of $8,000. Employees aged 60 to 63 are eligible for a higher catch-up contribution of $11,250.

Q: Why is it important to check my tax withholding mid-year?

A: Reviewing your tax withholding mid-year helps prevent surprises during tax season. If you are withholding too much, you are essentially giving the government an interest-free loan. If you are withholding too little, you may face unexpected tax bills or penalties. Adjusting your W-4 now ensures your withholding aligns with your actual tax liability.

Discover more from MassMutual…

Time to step on the insurance ‘ladder’?

Need a financial professional? Find one here

This article was originally published in June 2018. It has been updated.

__________________________________________

1 Internal Revenue Service, “401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500,” Nov. 14, 2025.

2 Consumer Financial Protection Bureau, “What is a debt-to-income ratio?” June 8, 2022.

3 National Foundation for Credit Counseling, “Time for a Mid-Year Financial Check-Up.”

4 Internal Revenue Service, “Topic No. 306 – Penalty for Underpayment of Estimated Tax,” March 31, 2026.