You may remember the late Senator Everett Dirksen (R, Illinois). He died in 1969 but made such a strong impression on the U.S. population (including winning a Grammy), that he continues to garner a reaction when his name is mentioned. He once stated, “A billion here, a billion there, pretty soon, you’re talking real money.”

Today, this update is with his spirit in mind…although we are going to add a handful of zeros.

What follows is an update on the coronavirus (COVID-19) outbreak, followed by a review of just how big the losses and relief packages have been. We hope to put some perspective around the size of the numbers. To prepare you a bit, let me offer that Senator Dirksen would perhaps not believe the magnitude of the numbers and likely question my math.

With that said, let’s begin…

As of the morning of May 5:1

- The novel coronavirus (COVID-19) has infected a bit more than 3.6 million people and killed more than 254,000 people worldwide.2

- In the United States, there are now a bit more than 1.2 million confirmed cases along with a little more than 71,000 deaths, with 25,000 deaths occurring in New York alone.3

- Italy, Spain, the U.K., and France all now have roughly 30,000 deaths each.2

Those numbers are both staggering and tragic. There is a reason they dominate the headlines and garner so much of our daily attention.

Yet, there are also some very positive changes taking place and, while it is too early to say we are in the clear, we are optimistic that perhaps the worst is behind us. The next several weeks are key as we watch the state-by-state numbers; particularly those states that are re-opening.

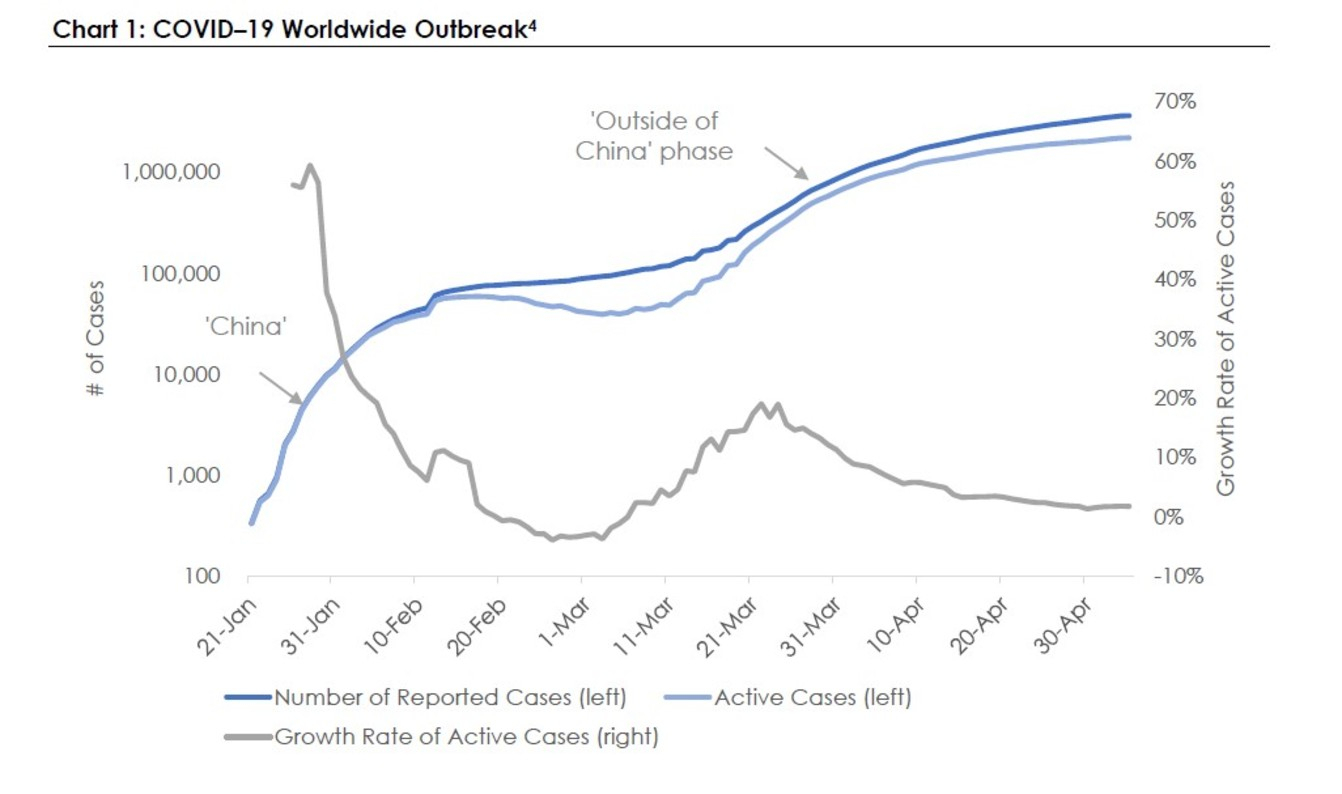

Chart 1 helps to demonstrate both the absolute numbers (which are frightening), and the changes (which are encouraging).

The blue lines demonstrate the total number of cases around the world. The grey line demonstrates how the number of cases is growing. On March 22, the growth rates were roughly 20 percent per day. Today, those growth rates are now consistently 2 percent per day.5 Frustratingly, the global growth rate has recently plateaued at around 1.7 percent (which means cases double every 40 days), and we are obviously hopeful that rate falls further.

Within the United States, the picture is perhaps even more dramatic. On March 21, the U.S. growth rate was 40 percent. As of May 5, it is now less than 2 percent.6 One month ago, the number of cases doubled every 1.8 days; today, the number of cases doubles every 27 days.

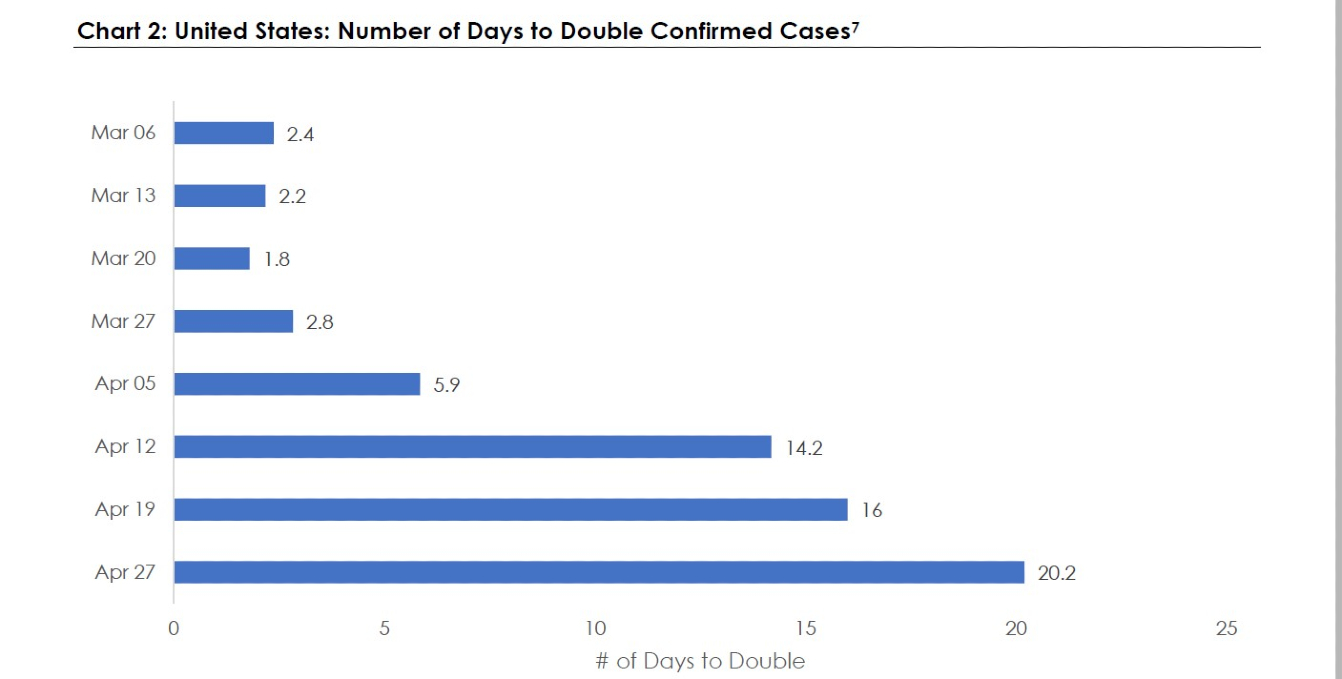

Chart 2 puts those growth numbers in context by showing the number of days to double, and how it has changed over time.

Clearly, this is great progress and saved thousands of lives. Cases were doubling every 1.8 days just six weeks ago, and they are now doubling every 27 days.

It is worth noting I am also currently studying the differences (and similarities) between New York (which has clearly slowed its growth curve recently), and other cities and states. As more states come online, this will be an important metric for how sustainable this re-opening will be.

Regardless, the cost of the lockdown has been, and will be, significant. We don’t yet know how large, but early indications are dramatic. Some recent numbers for context:

- Last week, 8 million more Americans filed for unemployment benefits.8 This brings the total to over 30 million Americans, which, if we assume there are roughly 157 million individuals in the U.S. workforce, is roughly a 19 percent unemployment rate.9 This is the highest since the Great Depression.

- U.S. first quarter Gross Domestic Product (GDP) was -4.8 percent. For context, it has hovered between 1.1 percent and 3.5 percent over the last several years.10

- Personal consumption (a good measure of U.S. spending) was -7.6 percent in March. That reading is generally between 0.1 percent and 0.3 percent each month. This was a dramatic contraction in spending.

In aggregate, Americans are less employed, spending less, and saving more: the basic definition of what a recession (or economic contraction) is. This then brings us to the final topic for this update: Have markets reacted appropriately, and are they priced expensively or cheaply?

The difficulty, of course, is that no one knows. Stock markets reflect both the information known, and the information expected. Said another way, a company is priced based on how it has performed historically … but perhaps more importantly on the expectations for how the company will perform in the future.

Therefore, let’s simply look at the magnitude of the markets’ reaction … and for the first view, let’s expand the scope significantly.

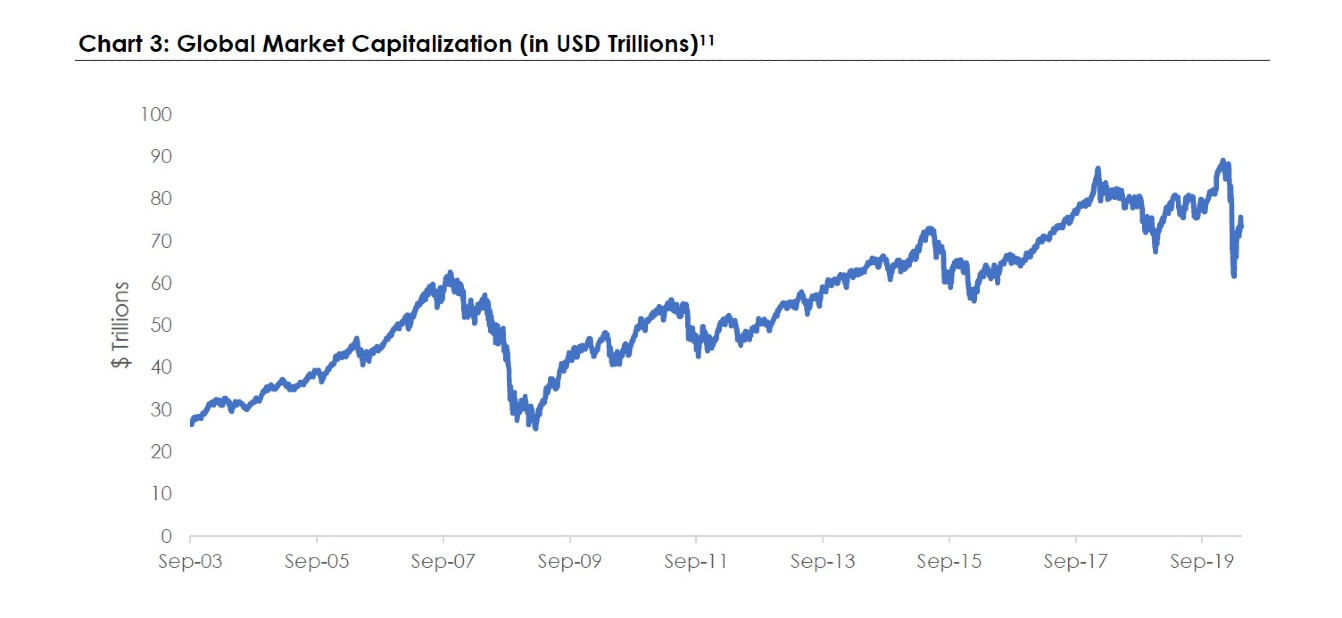

Chart 3 is the compiled picture of all available stock markets in the world: The sum of the value of all known companies that exist on public stock markets across the globe. This, of course, does not represent private companies or non-profits, but it is a good proxy for how markets, in total, have incorporated the outbreak.

Starting at the left axis of the chart, the total value of all companies in September 2003 was roughly $26 trillion. As we went forward, the total value of all public companies in the world peaked on February 16 this year at around $82 trillion.

By the time March 23 came along (just five short weeks later), the total value of all public companies in the world was around $62 trillion. For context, the entire U.S. GDP is around $21 trillion.12 These are remarkable numbers, and it is hard to understand just how significant the rapid loss of $20 trillion truly is.

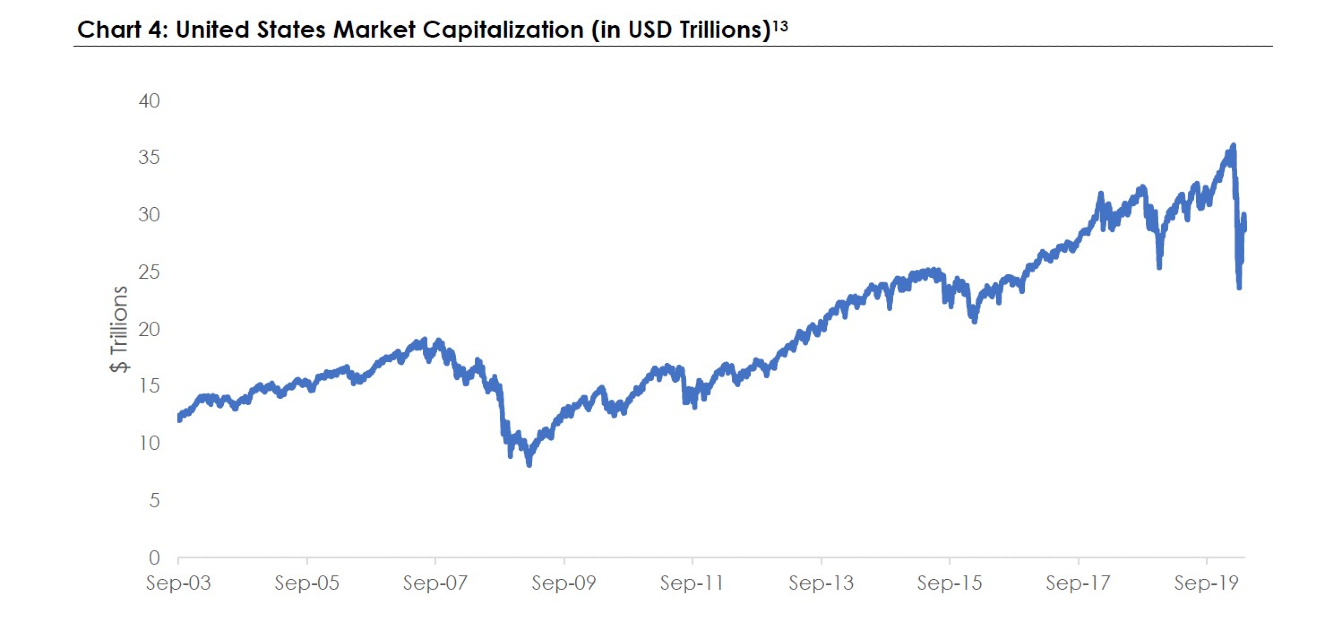

Chart 4 shows the same data but concentrates only on the United States.

Again, starting at the left axis, in September 2003, the entire value of all public companies was around $12 trillion. In February 2020, that number was peaking at around $36 trillion, and by mid-March, the entire value of those same companies was down to around $24 trillion. One third of the entire U.S. public company market capitalization (or roughly $12 trillion) was destroyed over a period of five weeks. Truly remarkable.

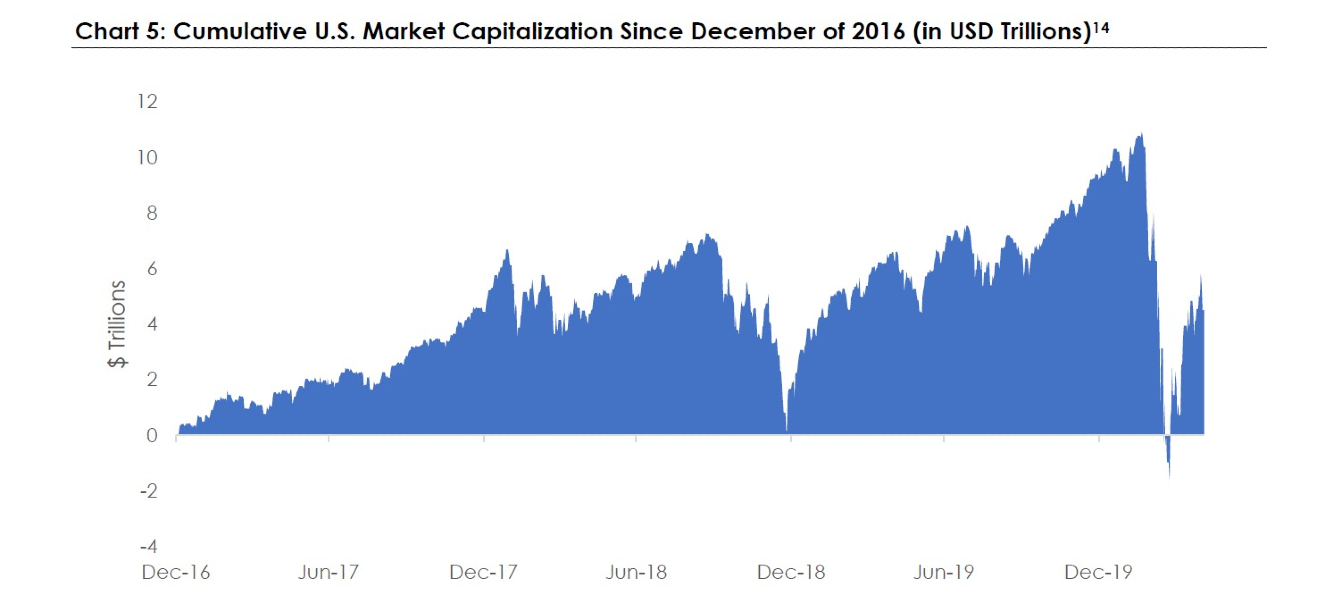

Chart 5 takes the same data, but zooms in a bit, and shows it in cumulative fashion to perhaps view this through a different lens.

This shows the same $12 trillion evaporating over the March time period but, perhaps more interestingly, it shows what happened after that time period.

After the bottom (so far) on March 24, the markets have added back an additional $6 trillion. Why that amount? Who knows? Are markets valued fairly? I have no idea.

Yet, it is worth noting that along with more positive case data, there were two additional items that have provided material stability:

- In addition to the benefits that came with cutting rates to zero, the Federal Reserve has provided an additional $2.3 trillion of stimulus (various asset purchases, liquidity, and the like) that could easily grow much larger.15

- Our federal government has now supplied an additional $3 trillion (roughly) of relief and/or support in various forms.

In essence, the U.S. stock market lost roughly $12 trillion over a short time period. The U.S. government provided roughly $5.3 trillion (and counting) in various forms, and the market responded by moving up roughly $6 trillion. So, while I shudder at the eventual implications of printing money so quickly, I can’t help but recognize the importance the U.S. government has played in stabilizing these markets. Said another way, Senator Dirksen’s adage has never been truer: We are suddenly talking real money.

Therefore, what is the conclusion? Well, again, let’s take stock of what we know:

- The equity market sell-off since mid-February has been unprecedented and was largely uncertainty and fear-driven. The downturn was fast, and the upturn was fast.

- The U.S. Government has provided unprecedented stimulus and support and has indicated there is additional willingness to do more should it be needed.

- The growth of the number of cases around the world is slowing. The desire to get the economy back online has turned into a gradual process of re-opening states, and those remaining states and municipalities are focused on weighing the costs vs. benefits of staying closed.

- Thus far, as a result of incredible stimulus, the underlying pipes beneath our market systems are working quite well. Markets have endured a remarkable level of stress and continue to operate with very few issues.

- The economic impact is still unknown, but early indications are this will be historic. We don’t yet know how deep or how long this will be, and we are watching closely.

As such, the only thing we can really do is to remain focused on the long term and benefit from capitalism and the allocation of capital. Capitalism and, by extension, capital markets, are confusing, volatile, and unpredictable in the short term. Therefore, let’s focus on the long term, and ignore the short term.

Learn more from MassMutual …

6 steps to restoring financial wellness after the COVID-19 crisis

3 tips to avoid locking in losses

What’s behind MassMutual’s financial strength

______________________________

1 https://worldometers.info/coronavirus, as of May 5, 2020

2 Johns Hopkins University, as of May 5, 2020

3 https://www.worldometers.info/coronavirus/; as of May 5, 2020

4 Sources: Bloomberg, World Health Organization

5 https://www.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6

6 https://www.worldometers.info/coronavirus/country/us/

7 Sources: Bloomberg, World Health Organization

8 https://www.dol.gov/ui/data.pdf

9 https://www.pewresearch.org/fact-tank/2019/08/29/facts-about-american-workers/

10 http://datatopics.worldbank.org/world-development-indicators/

11 Sources: Bloomberg; as of May 5, 2020. The World Market Cap indices do not include ETFs and ADRs as they do not directly represent companies. The calculation includes only actively traded primary securities on the country’s exchanges to avoid double counting. Therefore the values will be significantly lower than market capitalization values of a country’s exchanges from other sources.

12 https://www.bea.gov/news/2020/gross-domestic-product-fourth-quarter-and-year-2019-advance-estimate

13 Sources: Bloomberg; as of May 5, 2020 The World Market Cap indices do not include ETFs and ADRs as they do not directly represent companies. The calculation includes only actively traded primary securities on the country’s exchanges to avoid double counting. Therefore the values will be significantly lower than market capitalization values of a country’s exchanges from other sources.

14 Sources: Bloomberg; as of May 5, 2020. The World Market Cap indices do not include ETFs and ADRs as they do not directly represent companies. The calculation includes only actively traded primary securities on the country’s exchanges to avoid double counting. Therefore the values will be significantly lower than market capitalization values of a country’s exchanges from other sources.

15 https://www.federalreserve.gov/newsevents/pressreleases/monetary20200409a.htm