| ||||||||||||

Both traditional IRAs and Roth IRAs can help you save for retirement. But they have different rules about taxes on contributions and withdrawals, what happens if you need to take money out before retirement, and other things that can affect which account type you might be better off contributing to. We’ve answered some of the top frequently asked questions about the differences between Roth and traditional to help you decide.

Is there a difference in how much I can contribute to a Roth vs. a traditional IRA?

The maximum yearly contribution to traditional and Roth IRAs is $7,000 for 2025, the tax return you file in April 2026. It is $7,500 for 2026 ($8,600 if you're age 50 or older). In the case of a Roth, you may not be eligible to contribute that much, however, depending on your modified adjusted gross income (MAGI) or your filing status.

Recent legislative changes have also eliminated age limits for traditional IRA contributions. Additionally, the age at which required minimum distributions must begin was raised to 73. It will climb to age 75 starting in 2033. (Related: SECURE Act changes to retirement rules)

Can I contribute to a Roth or traditional IRA no matter how much I earn?

No, at least for Roth IRAs.

- For married couples filing jointly, the ability to contribute to a Roth IRA starts to phase out when modified adjusted gross income (MAGI) reaches $236,000 in 2025 and $242,000 in 2026. It is eliminated when MAGI reaches $246,000 in 2025 and $252,000 in 2026.

- For taxpayers who are filing single or head of household, the ability to contribute is eliminated when MAGI reaches $165,000 in 2025 and $168,000 in 2026. It starts to phase out at a MAGI of $150,000 in 2025 and $153,000 in 2026.

- For taxpayers who are married but filing separately, the ability to contribute is eliminated when MAGI reaches $10,000 in 2025 and 2026.

Calculate MAGI by subtracting from adjusted gross income any deductions for traditional IRA contributions, student loan interest, tuition and fees, and certain other, less-common above-the-line deductions (like the foreign earned income exclusion and the foreign housing exclusion that some expatriates take).

If you have a traditional IRA, you can contribute no matter how much you earn, but you may not be able to take a tax deduction for your contribution. If you or your spouse are covered by a workplace retirement plan and your income exceeds $89,000 for single taxpayers or $146,000 for married taxpayers filing jointly, in 2025 you will not be able to claim a deduction. Those limits climb to $91,000 and $149,000 respectively in 2026. You can still make after-tax contributions, however.

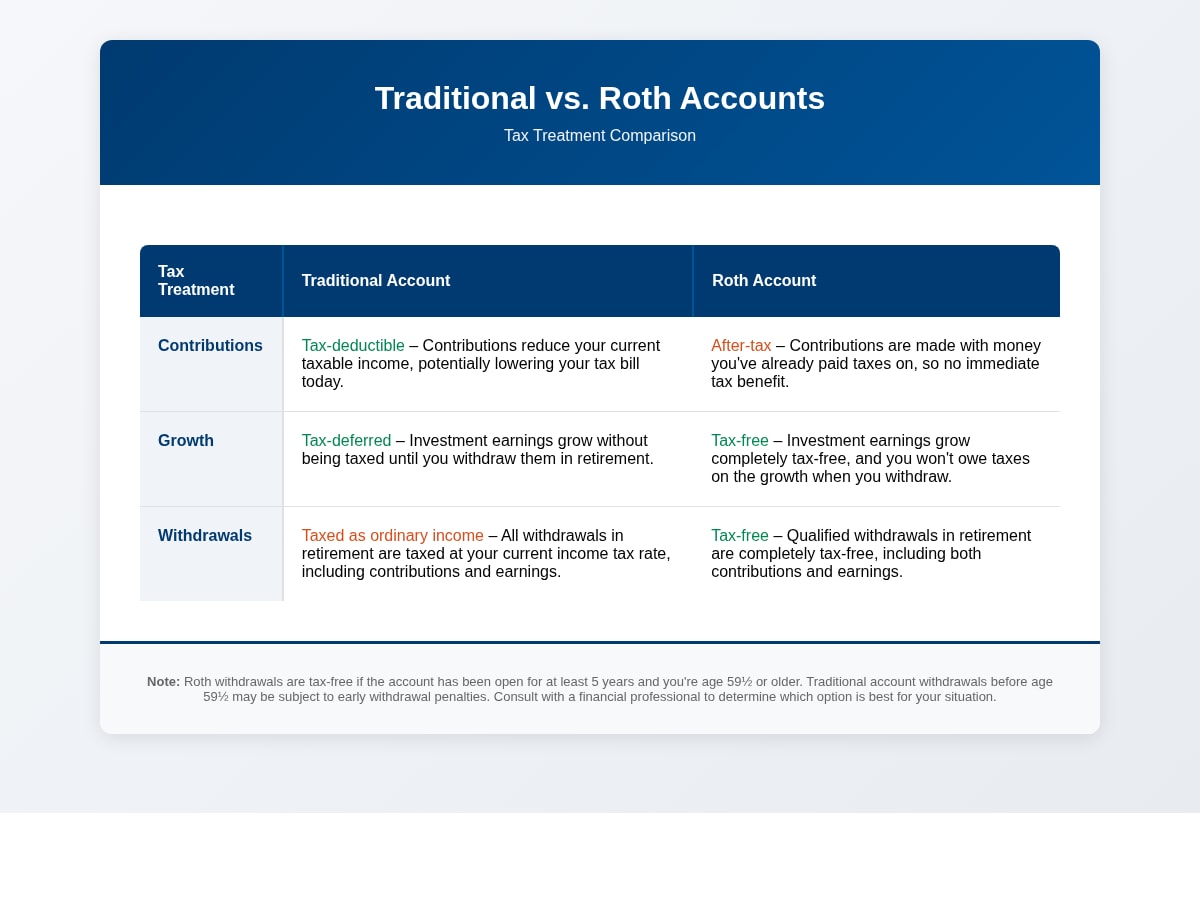

How are my contributions and withdrawals taxed on Roth and traditional IRAs?

With a traditional IRA, you do not pay tax on the money you contribute (in other words, contributions are made with pretax dollars), but you do pay tax on the money you withdraw. With a Roth IRA, you do pay tax on the money before you contribute (after-tax dollars), but you do not pay tax on the money you withdraw. In both types of IRAs, your earnings and gains aren’t taxed while they remain in the account.

You know how you receive a 1099 from your bank each year showing how much interest you earned because you have to provide that information with your tax return and pay tax on your interest? That doesn’t happen with an IRA — which helps your money grow faster.

Here’s a simplified example to illustrate the difference between the two IRA types.

Traditional IRA: You contribute $5,000 of pretax money to a traditional IRA. When you retire your money has grown hypothetically to $10,000. Your marginal tax rate is 22 percent. You withdraw all $10,000 and pay a 22 percent tax on it, or $2,200, leaving you with $7,800. But you saved 22 percent of $5,000, or $1,100, when you made your contribution, because your contribution was not taxable. So, you really ended up with $8,900 or more, depending on how you used the $1,100 in up-front tax savings.

Roth IRA: You contribute $5,000 of after-tax money to a Roth IRA. Since you are in the 22 percent tax bracket, you had to earn about $6,400 to contribute that $5,000 in the first place. When you retire, your money has hypothetically grown to $10,000, but at the sacrifice of the $1,400 in up-front taxes you paid, so it’s like you’re only making out with $8,600. However, you get to withdraw all $10,000 tax free.

Either way, you pay taxes; it’s just a matter of when. And while this example might make it seem like you’ll come out ahead contributing to a traditional IRA, that’s not always the case. It all depends on your marginal tax rate at the time you contribute and at the time you take withdrawals, which, unfortunately, most people do not know with certainty ahead of time. And, of course, rates of return in various types of IRAs will vary as well. (Related: Tax diversification advantages)

In this example, we assumed the same 22 percent tax rate both when you contributed and when you withdrew, but in reality, your tax rates will probably be different. Because you can’t know these things ahead of time, it may be strategic to contribute to both types of accounts.

So, I do not have to choose between a Roth IRA and a traditional IRA — can I have both?

Yes, and in fact, retirement planning experts recommend having a combination of post-tax and pretax accounts to draw upon in retirement. This might mean having both a Roth IRA and a 401(k) or both a Roth IRA and a traditional IRA. Since you do not know what your income or tax bracket will look like during any given year of your retirement, having the option to withdraw money from a Roth tax free in years when your income is higher and to withdraw taxable funds from a traditional IRA in years when your income is lower can keep your tax bill down. (Related: Why a Roth and 401(k) combo is appealing for younger workers)

“Having two buckets of money with different tax consequences gives you more control, and you can decide when it is more advantageous to take one or the other,” said CFP® Patricia Stallworth, an Atlanta-based money coach and the host of the "Minding Your Money 360°" podcast.

Should you always contribute to a Roth IRA and a traditional IRA every year?

Not necessarily. The conventional wisdom says that if you’re in a lower tax bracket when you make contributions than when you take withdrawals, you’ll come out ahead with a Roth. If you’re in a higher tax bracket when you make contributions than when you take withdrawals, you’ll come out ahead with a traditional IRA.

David Walters, a CFP®, CPA, and portfolio and client services manager with Palisades Hudson Financial Group in Portland, Oregon, said in an interview that “another reason you might have both accounts is if you want to make a backdoor Roth IRA contribution in order to avoid the Roth IRA annual income contribution limit. Under this strategy, for taxpayers who are not allowed to make a Roth IRA contribution because they are over the annual income limit, they can make a nondeductible traditional IRA contribution and, shortly thereafter, initiate a tax-free rollover of their traditional IRA to their Roth IRA.” (Related: Backdoor and mega-backdoor Roths explained)

My spouse is taking a few years out of the workforce to raise our young children. Can I contribute to an IRA on my spouse’s behalf?

Yes, but you must file jointly and your MAGI must be less than $236,000 in 2025 and $242,000 in 2026 in order to receive a deduction. Your total contributions cannot exceed your total compensation. So, if you only make $9,000 for the year, you cannot contribute $5,500 to your IRA and $5,500 to your spouse’s IRA, which would total $11,000. You’d have to reduce your contributions to either or both of your IRAs to total $9,000 or less.

Note that someone else could contribute to your IRA on your behalf, as long as their contribution (plus your contribution, if any) does not exceed your annual taxable income.

Also, let’s say your 16-year-old son earned $3,000 from a part-time job and you wanted to give him a huge jump start on saving for retirement. You could open an IRA for him and contribute $3,000. Just be aware that your generosity might have implications for college financial aid.

When do I get to take the money out?

Normally, when you’re 59½, you can withdraw both earnings and contributions from either type of IRA without paying any penalties. Roth IRAs do have a rule preventing the earnings portion of the account from being tapped for five years from when you established the account. Once you reach age 73, if you have a traditional IRA, you’re required to withdraw a certain amount from it each year, called a required minimum distribution (RMD). If you do not withdraw your RMD, you may have to pay a hefty 50 percent excise tax on the amount you were required to withdraw. With a Roth IRA, you are not required to take distributions from it. You can pass the entire account on to your heirs and let them worry about RMDs. (Related: Understanding required minimum distributions)

Career coach Larry Boyer of Success Rockets LLC recommends having a Roth IRA because it allows you to withdraw your contributions at any time. He said in an interview that older workers are increasingly finding themselves unemployed and unemployable because of artificial intelligence and other technological advantages. They’re not able to choose their retirement age, making a Roth IRA a lifeline for anyone forced to retire early. (Related: Handling unplanned retirement)

If you’re at least 55 when this separation from service happens, though, under IRS rule 72(t) you may be allowed to begin taking distributions from your traditional IRA or 401(k) early without penalty.

I may need the money for something else. Should I still contribute to a Roth IRA and a traditional IRA?

Yes, for several reasons. In a best-case scenario, you won’t need the money for something else and you’ll have made extra contributions to your retirement account that can grow for years. The more you contribute and the younger you are when you contribute, the faster your money will grow from investment returns and the less principal you’ll have to contribute over your lifetime to end up with a nice nest egg.

“You should not contribute to an IRA if you don't have some sort of emergency fund in place,” said Mike Zeiter, CPA and personal financial specialist with Foundations Financial Planning LLC, in an interview. His general guideline is to establish an emergency fund, contribute to employer plans to receive any matching contribution available, then make IRA contributions.

There is no sense in putting money in a retirement account if you can't afford to pay the bills in an emergency, Zeiter explained, because you will just end up withdrawing the money and paying a penalty.

There’s one big exception: As Boyer mentioned, as long as it has been at least 5 years from when you first established and contributed to a Roth IRA, a Roth IRA allows you to withdraw your contributions (but not your earnings) without paying taxes or penalties.

With a traditional IRA, you can remove money early in exchange for paying a 10 percent penalty on the amount you withdraw. You’ll also pay income tax on your withdrawals, just like you would in retirement. IRAs do not allow loans, but if you have a 401(k), you could consider borrowing from that account, if the plan permits. With traditional IRAs, one exception to the 10 percent penalty is the ability take up to a $10,000 distribution as a first-time homebuyer. You’ll have to pay income tax on that withdrawal, however, which will reduce the amount you can actually put toward your down payment. (Related: Borrowing from your 401(k): The risks)

Zeiter suggested saving for retirement at the same time as saving for a down payment. “You could put 3 percent of your income into retirement instead of 6 percent, but you shouldn't completely stop saving for retirement while trying to save for a down payment,” he said. “Life changes too much. You may end up putting off buying a house for five years. The one thing about saving for retirement is that you can only contribute a certain amount every year, and the law never lets you go back.”

Discover more from MassMutual…

Retirement savings catch up: 3 moves

Retirement planning: What women do right

Millennials and retirement: The ‘to-do’ list

This article was originally published February 2018. It has been updated.

___________________________