| ||||||||||||

If you are considering life insurance, one of the choices you’ll likely encounter these days is indexed universal life insurance (IUL).

This kind of life insurance is similar to variable universal life insurance (VUL), which offers some financial flexibility in addition to protection. However, unlike variable life insurance, IUL policies provide some level of guarantees concerning the investment performance of the contract. But IUL also comes with a lot of additional moving parts and non-guaranteed elements that can be difficult for some to understand.

While those features may be appealing to certain policyowners, such provisions can be confusing and inappropriate for others. Indeed, some opt to consult a financial professional about how such policies compare to other types of insurance protection.

Connect with a MassMutual financial professional

To help in such conversations, it is important to understand IUL features before deciding if it is right for you.

Part of the permanent life insurance family

IUL insurance is a kind of permanent insurance.

Permanent life insurance offers a guaranteed death benefit to your beneficiaries regardless of how long you live, provided the premiums are paid for a specified period. Permanent insurance is distinct from term insurance, which only provides coverage for a specified time period.

Further, permanent life insurance offers:

- Tax-deferred growth of cash value.

- The ability to borrow against the policy’s cash value.

Universal life insurance is a type of permanent insurance that allows for flexible premiums. And some types of universal life insurance, like variable universal life insurance, provide different investment options for cash value accumulation.

These kinds of life insurance options tend to appeal to those who want to allocate their account value into investments that align with their specific growth goals and tolerance for market volatility and investment risk.

IUL insurance particulars

In this vein, IUL insurance allows a policyowner to allocate cash value into an account with a fixed rate of return or accounts tied to various equity indexes, like the S&P 500® or Russell 2000®. So, like VUL, there’s the chance for some market participation while acquiring life insurance protection. And the growth rate credited to the policy is tied, in part, to well-known indexes, which might make some people more comfortable.

It is important to note that the cash value isn’t directly invested in the market index. An insurance company buys options on securities to mimic the index’s price performance. There are charges associated with that practice that can fluctuate with market volatility and interest rate changes. It also means dividends from the stocks aren’t included. Historically, stock dividends have been a substantial portion of a stock index return. So, the growth rate credited to the policy will be less than the growth rate of the index.

Additionally, the insurance carrier uses a formula to determine the growth rate credited to IUL insurance cash value accounts tied to an index. And the math behind that crediting rate calculation can be tricky and subject to change.

Generally, it uses a combination of three factors:

- A floor on losses. This is a minimum interest rate on the indexed account. So, when an index has a negative return, the growth rate credited to the policy will not go below a certain interest rate. However, even with a floor of 0 percent, it is possible for the account value to decline due to the deduction of policy charges.

- A cap on gains. This is a maximum crediting rate, typically in the 8 to 12 percent range. The cap level is generally not guaranteed and can be adjusted within certain limits, as outlined in the IUL contract.

- Participation rate. This is the percentage of an index’s positive price movement used to calculate the crediting rate, subject to the cap. If the S&P 500 returns 10 percent and the participation rate is 90 percent, the interest credited would be based upon 90 percent of that return, or 9 percent. The participation rate may also be subject to change.

The combination of these three factors means that gains in the index are limited in order to maintain a floor against possible losses. And so, the account never really enjoys the full measure of an index’s gains.

Example of IUL caps

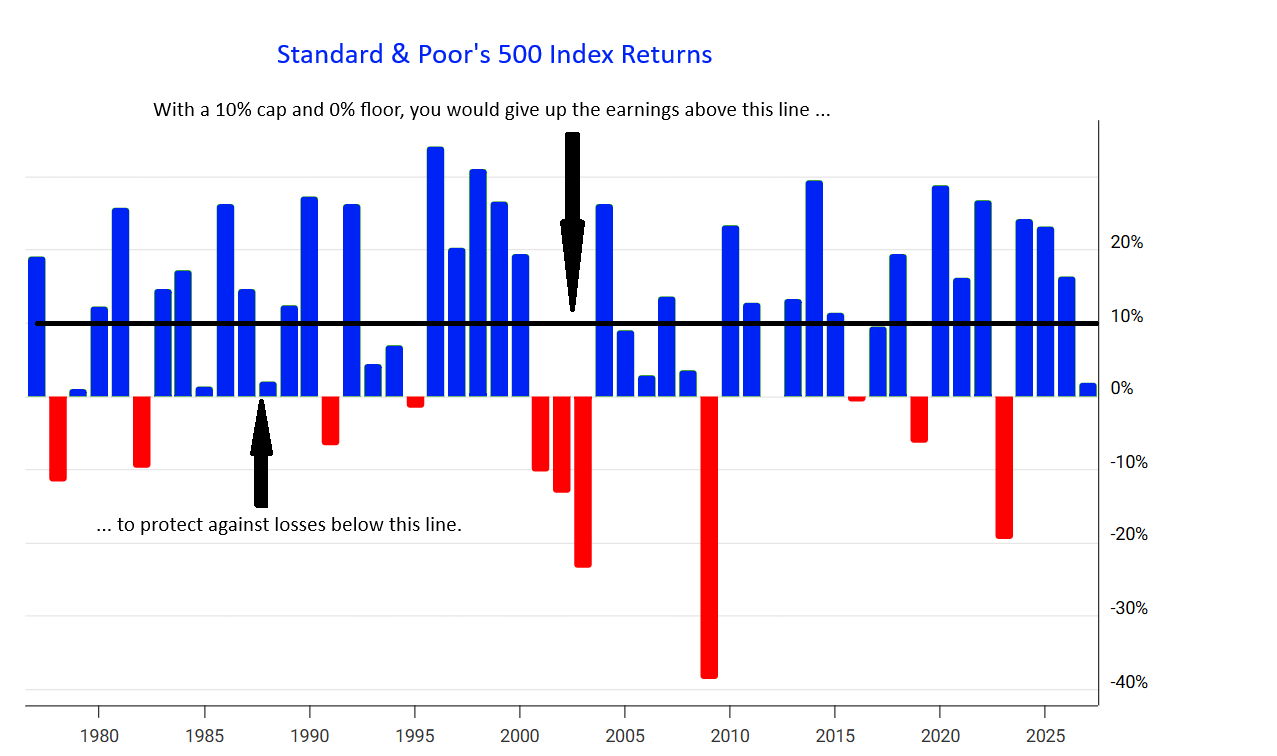

To illustrate how caps and floors affect returns, consider this historical example:

- Assume that the cap for an IUL policy is 10 percent.

- The floor is 0 percent.

- The participation rate is 100 percent.

These are very favorable parameters. The following chart shows the S&P 500 Index returns from 1976 through 2025 (excluding dividends).

As you can see, the upside potential would have been frequently limited, while the downside protection would have been much less frequent. Any performance above the cap line would have been lost, and any losses below the floor line reflect the benefit of downside protection.

Over this 50-year period, there were 29 years in which the returns were greater than the 10 percent cap. The total return given up was over 333 percent. There were only 11 years when the returns were less than the floor of zero percent. The total loss protected was about 140 percent. Also, keep in mind that the index values used here do not include dividends, which have historically been a significant portion of the S&P 500 Index annual returns.

Conclusion

The example above uses very favorable floor, cap, and participation rate factors. Obviously, the upside potential would be even more muted if the floor were lower, the cap lower, and the participation rate less than 100 percent.

Still, some people may find the combination of protection and investment options in an IUL policy appealing. But they should make sure that they fully understand how IUL works, and how it compares to other types of permanent life insurance — like whole life, universal life, and variable universal life — before buying a policy. Many turn to a financial professional to help understand what the options are and how they may apply to their own situation.

Discover more from MassMutual …

What goes into whole life insurance dividends?

Calculator: How much life insurance do I need?

This article was originally published in February 2021. It has been updated.

____________________

.jpg)