| ||||||||||||

Annuities can be a useful tool in wealth management and financial planning, but because there are different types, you need to understand how each works to determine which annuity type may be best suited for you.

There are different types of annuities. Some are generally long-term contracts designed to accept payments, allow for potential tax-deferred growth,1 and eventually provide income back out to the owner. On the surface they may sound like retirement plans, but while annuities share some things in common, they’re not the same.

They can be fixed or variable, immediate or deferred income annuities, depending on which contract option you select to meet your needs.

First and foremost, if you are considering an annuity, make sure to read any prospectus or specific marketing material that relates to that particular annuity carefully. It will provide all the details on how your specific annuity will work, and a financial professional can help you evaluate the options.

Connect with a MassMutual financial professional

Buying an annuity: Basic types

There are several different types of annuity contracts you can buy, but they fall into three major categories:

- Deferred fixed annuities (deferred fixed and deferred fixed index)

- Deferred variable annuities

- Income annuities (immediate and deferred)

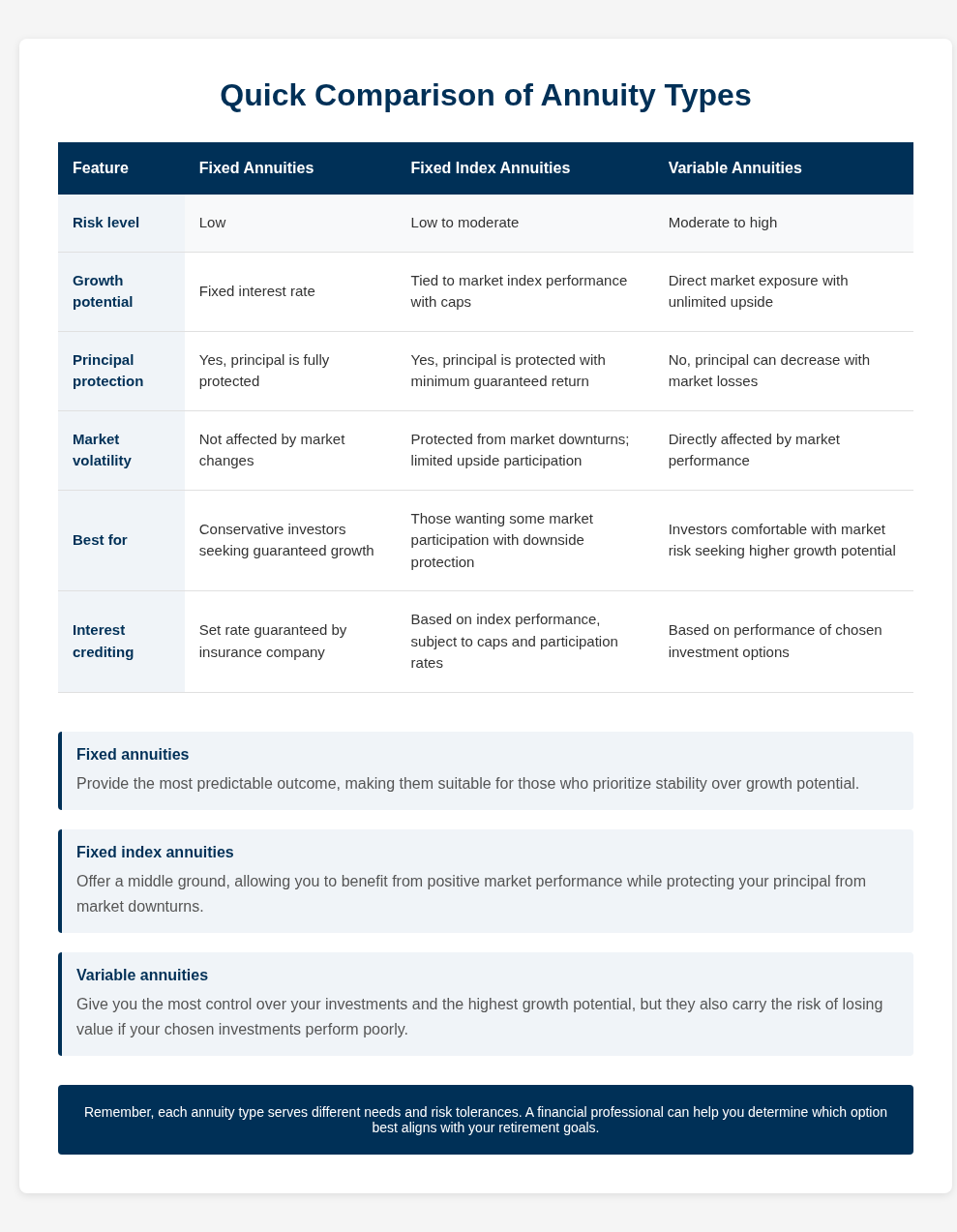

Deferred fixed and fixed index annuities

Deferred fixed annuities earn interest at an insurer-set rate that is set for the guarantee period elected at issue. This annuity type often provides a guaranteed minimum interest rate. They’re designed for a more conservative approach to growing some of your assets while avoiding the effects of market volatility.

While deferred fixed index annuities also fall under the fixed annuity umbrella, they credit interest differently than a traditional deferred fixed annuity. The interest that may be credited is tied, in part, to a specific market index, such as the Standard & Poor’s 500 Index. They typically provide the potential for a higher interest rate than a deferred fixed annuity – but they also present the risk that the contract owner might receive zero interest in a given year. Plus, interest may be credited only once a year with an index annuity, versus daily with a deferred fixed annuity.

Deferred variable annuities

Variable annuities are designed to provide market exposure. Their potential growth — and your potential future income — depends on market behavior, so while you might achieve greater gains than in a fixed annuity, you’re also exposing yourself to more risk, including the risk of losing value.

With variable annuities you are still purchasing an annuity contract from an insurance company. But unlike with fixed and income annuity types, you’re responsible for deciding how the money you apply to the contract is invested – typically from among a variety of underlying funds as well as fixed account investment options provided by the contract.

With many variable annuity contracts you can also make changes to how your contract value is allocated among the available investment options, a flexibility that can be particularly helpful as your risk tolerance changes over time. Of course, just like with any other stock or market-based investment, there is risk of loss of value and past performance is no guarantee of future returns.

A specialized kind of variable annuity is the registered index-linked annuity (RILA). These are a kind of indexed variable annuity that offer some features of both traditional variable annuities and fixed indexed annuities. RILAs offer growth linked to market indices (like the S&P 500) but include buffer and floor strategies to limit downside risk. RILAs are registered securities and carry investment risk, as they typically don't offer full principal protection like fixed index annuities.

Immediate and deferred income annuities

Income annuities, unlike the others, focus is not on accumulation but rather on creating an income stream. They can be immediate, meaning their payout can start within 12 months after purchase, or they can be deferred, delaying payments until a later date.

For example, if you’re near retirement and you have a lump sum of money you want to avoid spending all at once, an income annuity may help you manage your spending by spreading that money out into payments over a certain period or even your lifetime.

Unlike other annuities, with an income annuity you will know the amount of your guaranteed income at the time of purchase. Be aware, though, that income annuities generally do not allow the owner to withdraw contract value — meaning that once you pay into the annuity, you can’t touch that money again until it comes back to you as income.

Income annuities behave differently depending on contract specifics, but they are generally fixed, with a guaranteed income stream. They can provide immediate income or future income, but little to no liquidity — so you have to be OK with losing access to the money you use to buy an income annuity, as withdrawals of contract value are typically not available or limited with this type of annuity. You should ensure that you have other assets set aside to cover unexpected expenses.

There is also a specific form of deferred annuity called a qualified longevity annuity contract. It can be purchased with retirement funds, reducing RMD requirements and associated tax obligations.

How an annuity pays out

Once your money is in an annuity there are two general ways for getting the money back, depending on what is allowed by the type of contract you hold: withdrawal and annuitization.2

Withdrawals, for contracts that allow them, fall into systematic partial withdrawal, non-systematic partial withdrawal, or full withdrawal categories.

- Full withdrawal is just what it sounds like: whatever the value of your annuity is at the time of withdrawal, you receive the contract value minus any applicable charges, such as surrender charges, in a single payment. Keep in mind that when you withdraw that sum you’ll be responsible for paying any taxes due.3

- The systematic partial withdrawals option lets you tell the insurance company how much you want to receive and how often you want to receive it if withdrawals are allowed under the contract. Being able to set a higher or more frequent payment may be appealing, but it’s worth noting that with this payout option, unlike certain annuity payment options, the insurance company won’t guarantee that you won’t outlive the annuity. While you may have greater access to your contract value you will have to manage longevity risk on your own.

- Non-Systematic Partial withdrawals, if allowed by your contract, let you pull out a portion of your annuity’s value to help meet short-term objectives. It’s potentially useful if you need it, but any partial withdrawal (systematic or non-systematic) may reduce your annuity’s benefits, such as your death benefit, which allows you to pass on the contract to your beneficiaries in the event of your death, or optional living benefit rider.

Most deferred annuities have a “free withdrawal provision” that allows contract owners to receive a certain amount each year without incurring fees, though what that amount is will vary depending on contract specifics.

Keep in mind that annuities may assess a surrender charge on withdrawals if you sell or withdraw money during the surrender charge period, and withdrawals made prior to age 59½ may also be subject to a 10 percent federal income tax on the earnings.

The other avenue for getting money out is activating the annuity’s income stream, more formally known as annuitization.

Annuitization is the switch that flips an annuity into “payout mode”, initiating income payments according to the contract. There are several annuity payment options.

- With period certain annuitization, you can choose a defined period of time over which to receive payouts. If you die within that time, your listed beneficiary will receive the rest of the payments until the defined period is complete.

- Life payments are based not on a fixed period of time but on the annuitant’s calculated lifespan. The basic life option pays the contract-owner for the rest of their life, while joint life calculates a lower payout, which is based on you and your spouse being alive, giving the option for payments to go to your spouse for the rest of his or her life should you predecease them. The single life annuity payment option typically provides the largest payment amount, but has the most risk since payments cease upon the annuitant’s death. No payments will be made to a beneficiary.

- Life with Period Certain is kind of a blend of “life” and “period certain” – it pays you guaranteed income for life, like with the “life” option, but also allows you to pick a time period for guaranteed payments. That way, you get the “life” payments that are calculated based on your life expectancy, but if you die prior to the end of the period, payments will continue to your beneficiary until the guarantee period is up.

No matter what type of annuitization option you choose, keep in mind that annuity payments may be subject to tax. The specifics of how annuities are taxed change based on what type of annuity you buy, as well as whether you purchase the contract with pre-tax or after-tax money.

If you used pre-tax money (essentially buying a qualified annuity), then you’ll need to take required minimum deductions by age 73. (Related: Using annuities to satisfy your RMD obligations)

Also, annuities can have the protection of passing on the value to a beneficiary should the unforeseen occur. Many people misunderstand this. People may think that the value of an annuity can vanish or is taken by insurance companies once the owner passes on as a matter of course. But, depending on the type of annuity involved, that may not be the case. (Learn more: Understanding annuity death benefit protection)

Because there are so many variables involved, you should consider working with your financial and tax professionals to determine the options that will work best for you.

Should I buy an annuity?

There are several things to consider if you’re thinking about purchasing an annuity beyond the basics outlined here.

Typically, someone might consider purchasing an annuity after he or she has maxed-out his or her other tax-advantaged retirement plans, such as 401(k) plans or IRAs. Because each annuity contract has different terms, features, and requirements, the type of annuity you buy should be based upon your particular needs, such as the need for income, growth from a conservative investment, potential growth from a variable annuity, or the need to access the value in the annuity. (Related: Does an annuity fit your retirement goals?)

Be aware that there are fees and charges associated with variable annuities, such as mortality and expense risk charges, administrative fees, underlying fund expenses, penalties and more. This and other information is available in the prospectus (or summary prospectus). Read it carefully before investing. There are fees for certain optional features often available with fixed and variable annuities. As stated earlier, there are also typically surrender charge fees associated with withdrawals from fixed and variable annuities.

The other thing to remember with annuities is that although they’re designed to provide guaranteed income, that guarantee is based on the claims-paying ability of the issuing insurance company. So, if you decide to purchase an annuity contract, make sure to work with a financially strong insurer. (You can check MassMutual’s financial standing here.)

Before purchasing, it's important to weigh the pros and cons of annuities to ensure they align with your financial goals. Also, requirements and fees will vary based on annuity type and contract specifics, so make sure to read any annuity contract carefully.

Annuities can be a key component of a diversified retirement income plan, helping to ensure you don't outlive your savings. A financial professional can help you sort through the options and decide how an annuity may be a good move for your money.

________

Frequently Asked Questions about types of annuities

Q: What are the main types of annuities?

A: The three main categories are deferred fixed annuities, deferred variable annuities, and income annuities. Each type serves a different purpose, from conservative growth to market exposure or immediate income.

Q: What is the difference between a fixed and variable annuity?

A: A fixed annuity offers a guaranteed interest rate and protects your principal from market downturns. A variable annuity allows you to invest in the market for higher growth potential, but it comes with the risk of losing value.

Q: When can I withdraw money from my annuity without a penalty?

A: Generally, you can withdraw money without a 10 percent IRS penalty after you reach age 59½. However, you may still face surrender charges from the insurance company if you withdraw funds during the contract's surrender period.

_________________

Learn more from MassMutual …

Who did what with annuities? Take the quiz

Taking cash off the table: Life insurance, annuity alternatives

This article was originally published in May 2016. It has been updated.

__________________________________________

1 Tax deferral is automatically provided by tax-qualified retirement plans, including IRAs. There is no additional tax-deferral benefit provided when an annuity contract is used to fund a tax-qualified retirement plan or an IRA. Investors should only consider buying this contract in conjunction with a tax-qualified retirement plan or an IRA for the annuity’s insurance features such as lifetime income payments.

2 There are some growth-oriented annuities that offer, at an additional cost, an optional rider — typically called a guaranteed lifetime withdrawal benefit (GLWB) — that can provide a level of guaranteed income for life, even if the market drops significantly.

3 If taken before age 59 ½ an additional premature penalty will apply.