| ||||||||||||

Good news: Americans are getting a larger standard deduction in 2025. This inflation-based adjustment is one of many the IRS considers each year.

It may not feel as though inflation has slowed down when you’re buying groceries or car insurance, but compared with previous years, it has. The consumer price index in October 2024 was up 2.6 percent compared with 12 months earlier. In October 2023, it was up 3.2 percent year over year.

Along with raising the standard deduction, the IRS has increased how much you can save in certain retirement accounts, how much of your income is tax-free, and how much you can earn before moving into the next tax bracket.

It’s worth considering these changes as you draft your financial plan for 2025. (Related: Top tax changes for 2026)

Standard deductions

Your standard deduction in 2025 will be higher than it was in 2024. Your standard deduction is the amount of income the federal government lets you keep 100 percent of. You may owe less tax in 2025 if your income increases by less than 2.7 percent — the amount to which the deduction was increased due to inflation.

- For single people and married couples filing separate returns, it increases by $400, from $14,600 to $15,000.

- For heads of household, it increases by $600, from $21,900 to $22,500.

- For married people filing jointly and surviving spouses, it increases by $800, from $29,200 to $30,000.

If you’re 65 or older, your additional standard deduction increases by $50 from $1,550 to $1,600 per qualifying spouse if you’re married and from $1,950 to $2,000 if you file as single or head of household.

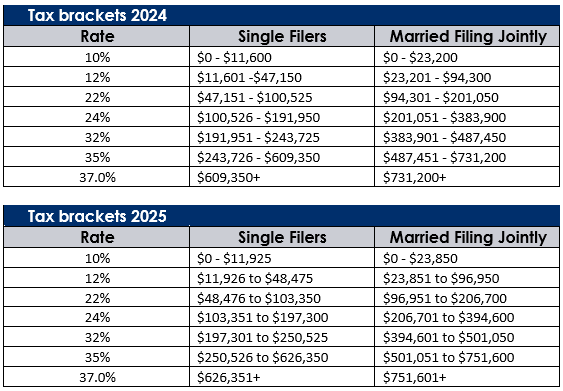

Tax brackets

Marginal tax rates won’t change in 2025. The lowest rate will remain 10 percent, and the highest will still be 37 percent. The amount you can earn within each tax bracket has been increased for inflation, however.

Here’s a simplified example that assumes all your income comes from work. If you filed as single in 2024 and earned $100,525, you were at the top of the 22 percent tax bracket. In 2025, you could earn $103,350 and still pay the same marginal tax rate. In other words, your pay could have increased by $2,825, or about 2.8 percent, without pushing any of your income into the 24 percent tax bracket.

The average salary increase in 2024 was about 3.8 percent according to The Conference Board, a nonpartisan think tank that delivers business insights. For 2025, U.S. companies expect to raise salaries by 3.9 percent.

“It’s a good idea to consider if you should update your W-4 withholding form with your employer,” said Annette Nellen, CPA, professor of tax and accounting at San Jose State University. “If you owed taxes when you filed your 2023 return, you might not be having enough taxes withheld from your paychecks or you might need to make quarterly estimated tax payments.”

IRA contribution limits

The IRA contribution limit remains at $7,000 for 2025 (or 100 percent of your earned income, whichever is less).

While the deadline to contribute for 2025 won’t arrive until April 15, 2026, making regular contributions and automatic investments throughout the year can be more effective than hoping you’ll have a lump sum to contribute at tax time.

● If you want to max out your savings and contribute monthly, you’ll need to set aside $583.33 per month.

● If you want to align your contributions with your biweekly paychecks, that’s $269.23 every two weeks.

The catch-up contribution amount for individuals 50 and older remains at $1,000 for 2025. That’s an additional $83.33 per month ($666.66 total) or $38.46 every two weeks ($307.69 total).

If you have a SIMPLE IRA through work, the annual salary deferral contribution limit will increase by $500, from $16,000 to $16,500. The catch-up contribution limit will stay the same at $3,500. But if you’re 60, 61, 62, or 63, you’ll be able to make an even larger catch-up contribution of $5,250.

Roth IRA eligibility income limits

The IRS limits how much you can contribute to a Roth IRA directly when your modified adjusted gross income reaches certain levels.

● If you file as single or head of household, you can directly contribute a reduced amount (less than the $7,000 maximum) once your income hits $150,000 (up from $146,000). You can’t contribute directly to a Roth IRA at all if your modified adjusted gross income exceeds $165,000 in 2025 (up from $161,000 in 2024).

● If you’re married and file jointly, the phaseout range is $236,000 to $246,000 in 2025 (up from $230,000 to $240,000).

● If you’re married and file separately and you lived with your spouse at any time during the year, the phaseout range doesn’t adjust for inflation and will still be $0 to $10,000 in 2025. If you did not live with your spouse, the single and head of household range applies.

You can still contribute indirectly to a Roth through a backdoor Roth IRA once your income exceeds these limits.

Traditional IRA deductible contribution income limits

You can make after-tax contributions to a traditional IRA regardless of how high your income is. To claim a tax deduction, however, your income needs to fall below certain limits if you or your spouse are able to contribute to a workplace retirement plan.

● If you’re a single filer, the phaseout range in 2025 is $79,000 to $89,000 (up from $77,000 to $87,000 in 2024).

● If you’re married and file jointly, the range is $126,000 to $146,000 (up from $123,000 to $143,000) if you can contribute to a workplace retirement plan.

● If you’re married to someone who can contribute to a workplace retirement plan but you can’t contribute yourself, the phaseout range is $236,000 to $246,000 (up from $230,000 to $240,000).

● If you’re married filing separately and covered by a workplace retirement plan, the phaseout range remains at $0 to $10,000.

401(k), 403(b), most 457 and Thrift Savings Plan contribution limits

If you have access to any of these employer-sponsored retirement accounts, you’ll be able to contribute as much as $23,500 in 2025, an increase of $500 (about 2.2 percent) from 2024.

“Check with your employer to be sure your contribution is increased if you are contributing the maximum amount each year,” Nellen said.

If you get paid every two weeks and want to max out your contributions, you’ll have an additional $19.23 withheld from each paycheck, for a total of $903.85 per pay period.

“In 2024, employers gained the option to make matching contributions to an employee’s 401(k) plan tied to their student loan payments,” Nellen said. “Ask your HR department about this option if your student loan payments are making it hard to put enough in your 401(k) to get your employer’s match.”

This student loan matching provision from the SECURE 2.0 Act is designed to help workers save for retirement while repaying education debt.

Workplace plans also let you make catch-up contributions of up to $7,500 in 2025 if you’re 50 or older, or an extra $288.46 per paycheck. This limit is unchanged from 2024.

What is new for 2025 is that if you’re 60, 61, 62, or 63, you’ll be able to make a catch-up contribution of up to $11,250 under a SECURE 2.0 Act provision that will kick in.

If you can afford to contribute more than that limit for your age bracket, find out whether your employer’s plan would allow you to make mega-backdoor Roth contributions.

Solo 401(k) contribution limits

If you earn a high income as an independent contractor or sole proprietor income, you can take advantage of a solo 401(k) to save far more for retirement than most employees are allowed to. (Related: Freelance taxes)

Like employees, you can contribute up to $23,500 to a solo 401(k) in 2025. And instead of the matching contributions that many employees receive, your company can make a profit-sharing contribution of up to $46,500.

That’s a maximum annual contribution of as much as $70,000 (up from $69,000 in 2024) — plus a $7,500 maximum catch-up contribution if you’re 50 or older $11,250 if you’re 60, 61, 62, or 63. To contribute the maximum, however, your self-employment income would need to be at least $280,000.

Long-term capital gains taxes

Outside of tax-advantaged retirement accounts, long-term capital gains tax applies when you make money selling an investment you’ve held for more than a year. Unlike short-term capital gains, which are taxed at your top marginal rate, long-term gains are taxed at lower rates.

In 2025, the long-term capital gains tax rate is 15 percent tax once your income exceeds $48,350 if you’re single, $64,750 if you’re head of household, and $96,700 if you’re married and file jointly or you’re a surviving spouse. The respective thresholds in 2024 are $47,025, $63,000, and $94,050. Below these limits, you don’t owe the tax.

Should your income get into the mid-six figures (more than $533,400 for single filers, $566,700 for heads of household, and $600,050 for married joint filers), the capital gains tax rate hits 20 percent. (Related: Preparing for an audit)

Potential tax changes under the new presidency

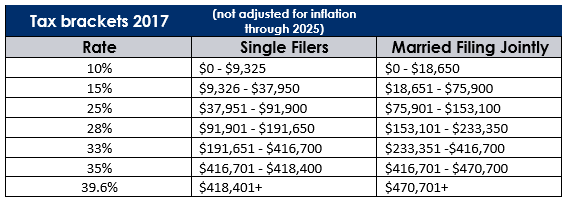

Donald Trump is expected to make tax changes a priority. His efforts may include extending or making permanent the provisions of the 2017 Tax Cuts and Jobs Act set to expire on December 31, 2025. (Learn more: The 2026 tax planning question mark)

Without action on the tax code, brackets will revert back to 2017 levels, adjusted for inflation.

The 2017 law also doubled the standard deduction and the lifetime estate tax exclusion, lowered tax rates, doubled the child tax credit, and created a 20 percent qualified business income deduction for sole proprietorships, partnerships, S corporations, and some trusts and estates.

Conclusion

The tax changes for 2025 are mostly minor and allow you to continue saving for retirement while possibly reducing your tax bill. Wondering whether your overall financial plan is on track? Your MassMutual financial professional can help you review your accounts and create a personalized strategy to meet your goals. (Need a financial professional? Find one here or let us know.)

Discover more from MassMutual…

The 2025 changes coming to Social Security

8 FAQs on traditional vs. Roth IRAs

5 retirement investment strategies

_______________________