Have you ever seen a dog chasing a car and wondered: “What happens if the dog actually catches it?” That’s what I thought of recently as I watched Federal Reserve Chairman Jerome Powell discuss the central bank’s new, and suddenly resolved, determination to slow (catch?) inflation. The question then becomes “what happens if they are able to raise rates enough to stop inflation?” More than they bargained for?

We will begin with what inflation is and how high it has become. We will then turn to why it has occurred and wrap up with thoughts and perspective on possible outcomes. Let me also acknowledge that the topic of inflation and, in particular, Federal Reserve policy, is not one most Americans are thrilled about discussing … but I will note it is probably the most important dynamic in play right now (so I congratulate anyone who can make it to the end of this update!).

With that, let us begin.

Inflation

For a moment, ignore what you have heard about inflation. It is not complex; we in the investment and economics world only choose to make it sound that way. Inflation is nothing more than an increase in the prices of goods and services. If I can buy 10 loaves of bread today with the $10 in my pocket, and tomorrow I can buy only nine loaves of bread with another $10 … then the price of bread has gone up, and the value of my dollars has gone down. That’s it. Prices go up and the value (or purchasing power) of our currency goes down.

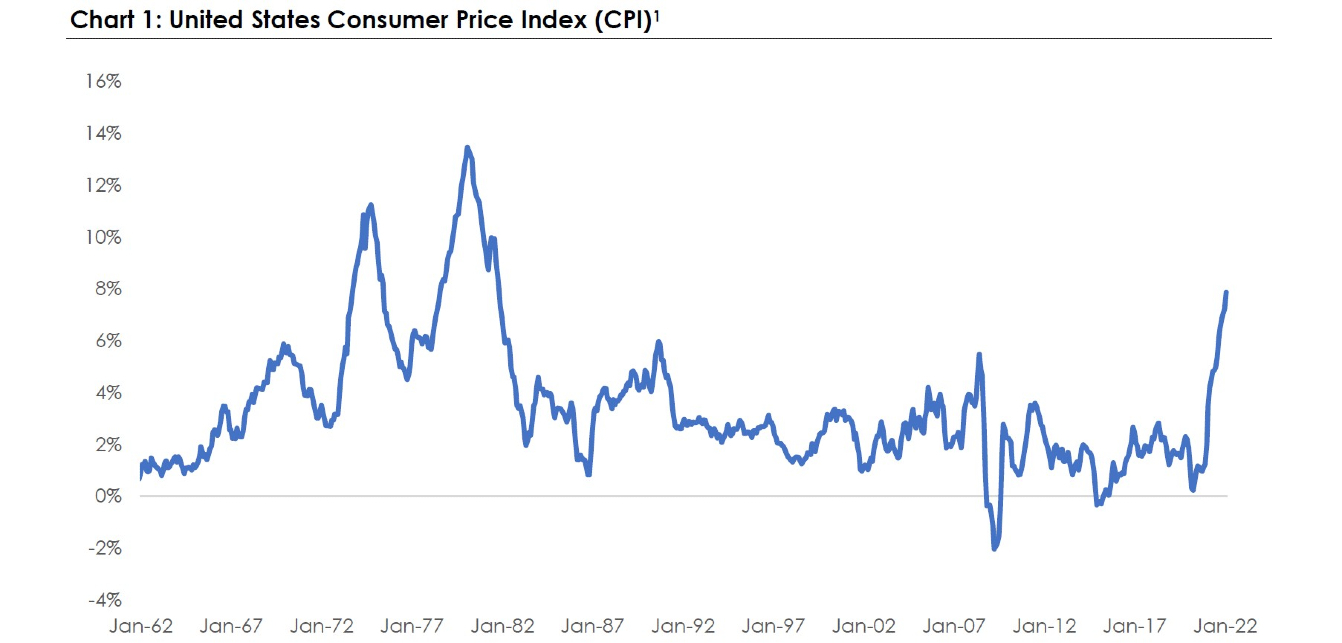

We can measure that dynamic in many different ways (and we do), but the primary measure of inflation in the United States is something called the Consumer Price Index (CPI). Candidly, it’s a bit flawed as an index, but let’s review it as it is the primary index of reference. It’s simply a percentage change of how much prices have changed, where prices are defined as a basket of goods (cars, energy, housing, paper towels, etc.).

As Chart 1 demonstrates, we have not seen inflation this high since the early 1980s. Recently, however, we, as consumers, have felt this on a daily basis as everything from used cars to houses to gas to consumer goods have increased in price, and done so rapidly.

It is worth noting that lower income households feel the effects disproportionately so, as a larger portion of those households’ incomes are going to basics such as food, housing, and utilities, and those households are less likely to be able to absorb the price increases. As such, inflation is not equal opportunity, unfortunately.

Investors, on the other hand, have benefited from this dynamic in that inflation has not been limited simply to the goods we purchase, but also to goods we own (more on this later). Examples include houses and financial assets (stocks, for example). Again, it is worth noting this also disproportionately benefits wealthier households as it is those households that are more likely to hold hard assets such as homes and financial assets such as stocks.

The question, then, is why?

Causes of inflation

Attribution of why prices move is always difficult: there is no way to reconcile all transactions that make up the sum movements of a price, let alone an index. Further, as we have discussed in these updates, markets are dynamic, complex, and always evolving. Yet … as students of history, we can also observe certain fundamental principles that seem to occur over and over. In many ways, this inflation increase follows many patterns of old.

First, the obvious causes.

- Pent up demand: It should come as no surprise to anyone that consumers, particularly those used to spending (as we are in the United States) have not been able to spend throughout the pandemic as they normally would. Vacations were canceled, clothing orders were halted, restaurants were shuttered, and concerts were postponed. Now that we have returned to some semblance of normalcy, consumers are, once again, spending. Flights are packed, hotels are filling up, restaurants are full, and consumers are spending.

- Supply chain disruptions: It should also come as no surprise to anyone that the previously impregnable global supply-chain has had some troubles. Ports around the world have closed because of COVID-19 outbreaks. Manufacturers have shuttered because of disrupted demand, and suppliers of raw materials have ceased operations (or been slowed) because they are having a hard time finding labor and, often, supplies. The Russia invasion of Ukraine only furthered this dynamic and continues to wreak havoc on markets such as energy and wheat.

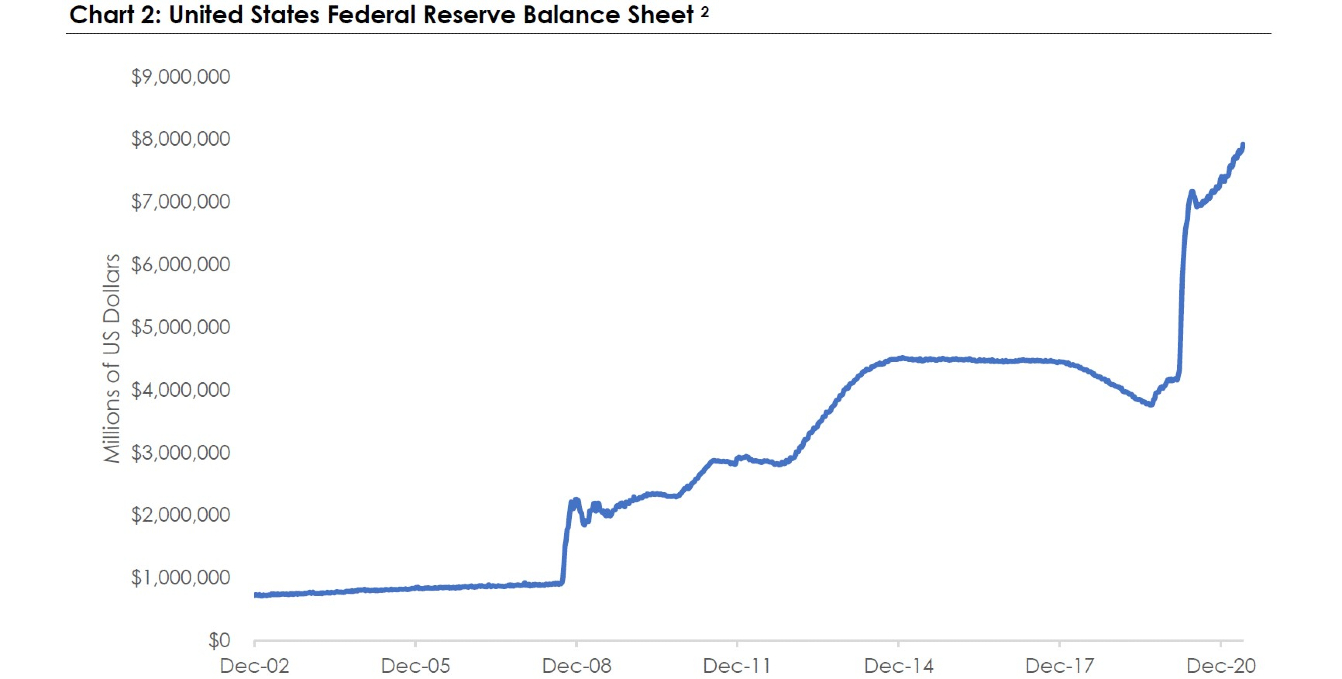

Perhaps what is less obvious is what role the Federal Reserve has played in this dynamic, which is the third major contributor. This brings us to Charts 2 and 3.

With my apologies to the faint of heart, please let me explain. The axis in Chart 2 is in millions of dollars, so 1 million is 1 million millions, or one trillion dollars. Remember, the entire U.S. economy is only $21 trillion (roughly).

What this chart shows is the expansion of the U.S. Federal Reserve balance sheet. While that sounds incredibly complex, it’s actually pretty straightforward.

The Federal Reserve is the Central Bank of the United States. It is the “lender of last resort” or think of it as the bank to all other banks.

As useful and impressive as the Federal Reserve is, their tools are, candidly, fairly crude. This isn’t controversial, by the way. It is generally well understood. They are studying a massively complex economy and trying to accomplish two things well:

- Stable prices.

- Maximum employment.

One of their difficulties, unfortunately, is they don’t have many tools. They can raise and lower the rate at which the banks lend, they can incentivize banks to lend more or less through some more nuanced requirements, and they can talk. (It turns out, by the way, that thus far, the talking, or signaling, is actually quite powerful in adjusting the market’s expectations. More on that in another update.)

They can also expand their balance sheet. Up until 20 years ago, they hadn’t really used this tool much and, in fact, most people didn’t realize they could.

Essentially what happens when they expand their balance sheet is they turn on a computer, they click some buttons, and magically, a bunch of dollars suddenly appear (it is worth noting that they need the U.S. Treasury involved but this a mere detail in what actually occurs).

The Federal Reserve, with some limitations and oversight, then can go buy assets in the marketplace. If they are concerned about lending markets acting reasonably, for example, they can go buy mortgages. If they are concerned with stock prices and the stability of the market, they can go buy stocks (as the Japanese Central Bank did).

So, in 2002, as the chart shows, there was less than $1 trillion of usage, and it’s largely ignored in the marketplace. Then in 2007/2008, the Global Financial Crisis hits, and the Federal Reserve turned on this machine and made some very clever, and incredibly helpful, moves. They stabilized the lending and liquidity markets nearly overnight, and allowed the economy to recover through continuing to signal they were willing to step in and backstop markets. Once the crisis was over, because of commitments they had made, they continued to increase their balance sheet — $3 trillion, $4 trillion. At the time, it was unprecedented and largely lauded as a very creative and stabilizing move.

Then, some of the bonds they had purchased started to mature and the balance sheet began to contract again. At this point, all of those items were expected and the balance sheet was shrinking as it should.

Unfortunately, the unexpected occurred and the world changed. COVID-19 hit in 2020 and suddenly the Federal Reserve balance sheet went from $4 trillion to $8 trillion — and did so very rapidly. Nearly instantly, trillions of dollars were created out of thin air, and those dollars were pushed out into the marketplace. Between those newly minted dollars, and the fiscal stimulus that occurred, somewhere between $12 trillion and $15 trillion was created (depending on who is counting).

At the beginning of this section, I began with clarifying that inflation is the rising of prices, and also, and importantly, the decline of the value of the currency. Well, we have just created massive amounts of currency out of thin air and, by definition, the currency we all hold is now worth less. That is simply supply and demand.

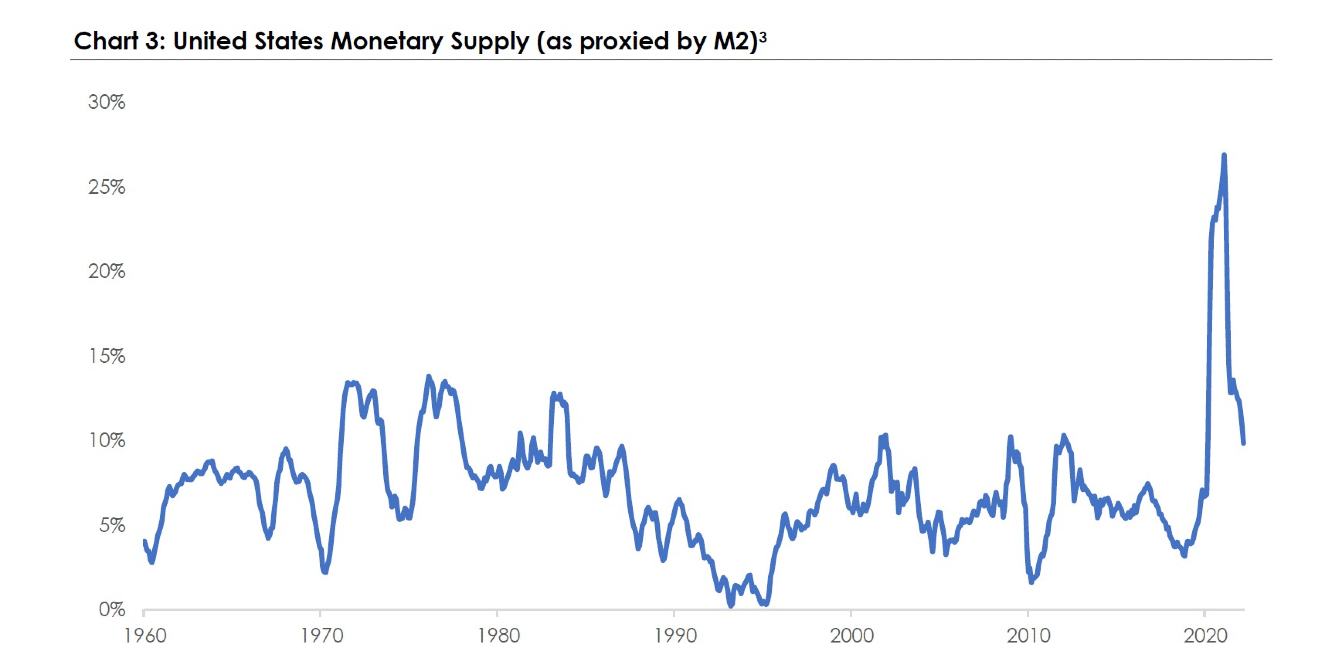

One of the ways we can measure that dynamic is through something called M2. While there are many details, the short version is that, in the United States, M2 is roughly defined as the total of all cash, checking deposits, and easily convertible “near” money. It’s certainly not a perfect measure but something to keep an eye on (note, the Federal Reserve publishes this data) particularly given how significant the percentage increases have been.

Chart 3 shows the percentage change in monetary supply since this all began. If you check the math, our United States money supply (as proxied by M2) is up 36 percent since March 2020. That’s right, the money supply has increased by roughly one-third since COVID-19 began. While that is merely one view, it is an important one, and one that perhaps gives us clues as to how this might progress.

Chart 3 then shows us something really important in three phases. Phase 1 was a steady increase in money supply between 1960 and 2020. Phase 2 was a massive increase in money supply between early 2020 and late 2021, and now Phase 3 is a slowing of that increase in money supply back to more reasonable levels.

Why has this phase 3 occurred? Well, the Federal Reserve, which largely controls this lever, has suddenly realized that prices are rising too rapidly (see their mandate #1 above), and they must rein them in. Therefore, quite simply, they have begun slowing the money supply growth through raising rates, shrinking the balance sheet, and no longer purchasing bonds in the marketplace.

What to expect

If you’ve read my market updates before you will note I am neither knowledgeable nor arrogant enough to predict the future. And this update will follow suit.

With that said, I expect bumpiness.

Markets of many sorts (financial, real estate, cars, etc.) have moved higher because, among other reasons, the markets were awash with new dollars. As dollars are created and enter the market, they tend to push prices higher.

Now that the Federal Reserve is taking inflation seriously, the withdrawal of liquidity has the opposite effect. The withdrawal of liquidity has now pushed the prices of those assets … notably financial assets … down.

This is both expected and relatively healthy … while obviously painful for those owning those assets. Optimistically, this is signaling that the Federal Reserve is finally focusing on the real economy, and not just financial markets … but time will tell if that focus remains.

As such, we, as investors, should recognize that this new dynamic of the withdrawal of liquidity (at least in the short term) will require a reset of sorts. Companies with poorer prospects and weaker balance sheets will suffer, and financial assets will need to reset to adjust to higher costs of capital. This is consistent with business cycles over history, although clearly there are some new dynamics currently as well.

It is worth noting that the risk of something called stagflation, which is higher inflation coupled with slowing growth, has also risen. This is a difficult problem for the Federal Reserve to address, and we are watching this closely.

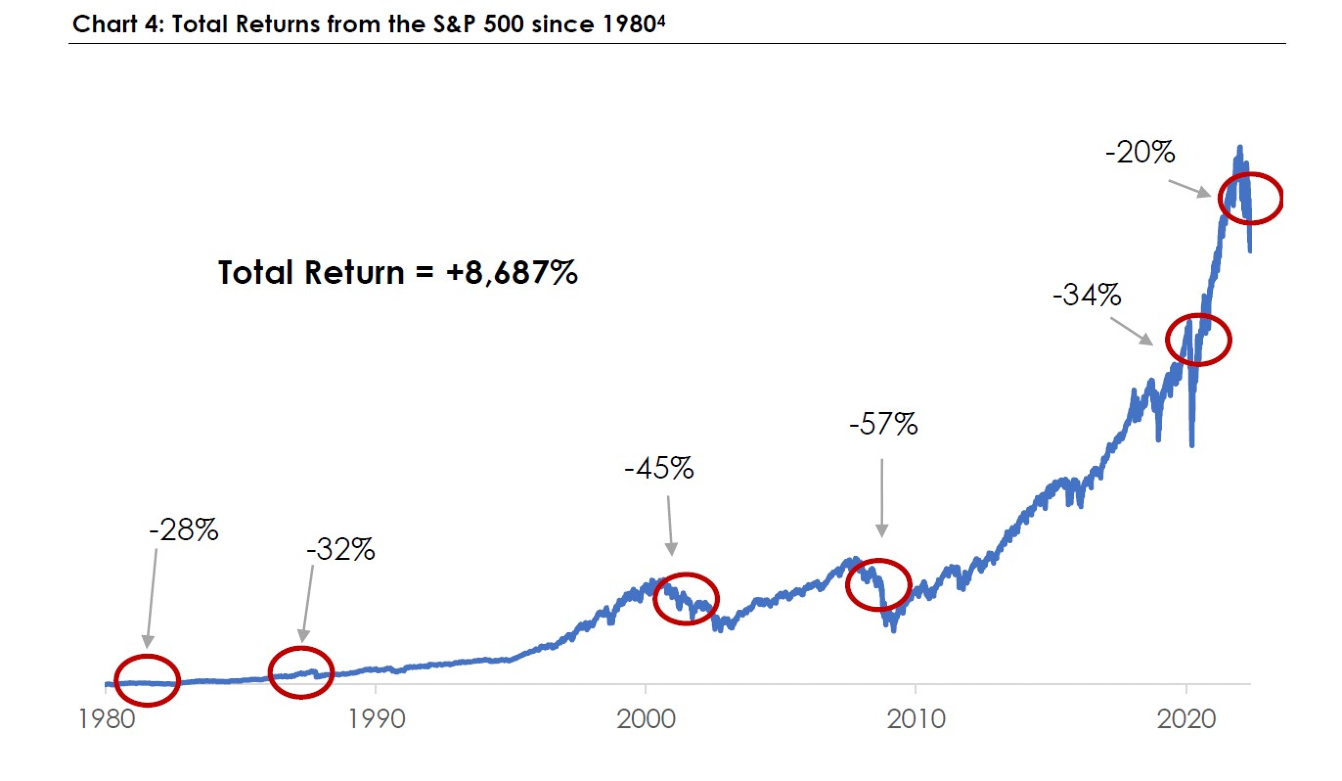

Lastly, and in conclusion, I offer Chart 4.

This chart simply shows the total return of holding the Standard & Poor’s (S&P) 500 since 1980.

Importantly, you may notice this is the sixth sell-off of more than 20 percent since this chart began. Each sell-off has its own stories, concerns, worries, and risks. In each of them, many investors became fearful and sold near the bottom. And yet, the market has generated remarkable returns over this time period. Roughly speaking, $10,000 invested in the S&P 500 in 1980 would be worth around $450,000 today … and that is despite the many sell-offs that occurred throughout this time period.

Will this time be the same? Will this time be different?

I have no idea. I do, however, know that I rely on the timeless and reliable principles of incentives, and the incentives for both companies, and investors, have not changed. Companies are still incentivized to generate higher levels of income and capture more market share and, as investors in those companies, we are still incentivized to provide capital to those companies to fuel that growth.

In closing, we continue to watch closely. Take a moment to breathe and use the difficult markets as an opportunity to focus on what can be controlled, while trying to minimize the impact of those items that cannot.

Discover more from MassMutual …

3 ways to consider market volatility

When markets dive, keep your strategic calm

How higher interest rates may hit consumers

_______________________

1 Source: Federal Reserve Bank of St. Louis, as of May 23, 2022

2 Source: Federal Reserve Bank of St. Louis, as of May 23, 2022

3 Source: Federal Reserve Bank of St. Louis, as of May 23, 2022

4 Source: Bloomberg, as of May 23, 2022