Just this week, we have had markets fall, rally, and then fall again, precipitously. Just this year, we have the worst bond market in the last 50 years, the most tragic and involved military engagement (in Europe) since World War II, and the worst inflation in 40 years. And in just over the past two years, we have had the worst pandemic in the past 100 years.

Yes, these are confusing, dangerous, and frequently volatile times. We are inundated with bad news, and we are blasted with doomsday headlines.

And yet … we also have a job to do.

We must see through the chaos, steel our nerves, and at the end of the day, make the best investment decisions we can, given the information at our disposal.

Which leads us to the difficult questions: What should we be doing? Should we be selling? Should we be buying?

While all investment decisions are, of course, personal, and frustratingly, also rarely have certain outcomes … today we are going to use three lenses to view into the abyss and try to answer those questions.

With that, let us begin.

Likelihood of being right

The first lens I would offer is the lens of humility. Timing markets is, inherently, VERY difficult. The best investment managers in the world rarely get it right, and if hordes of well-equipped analysts and strategists fail, how are we, mere mortals to navigate such difficult times?

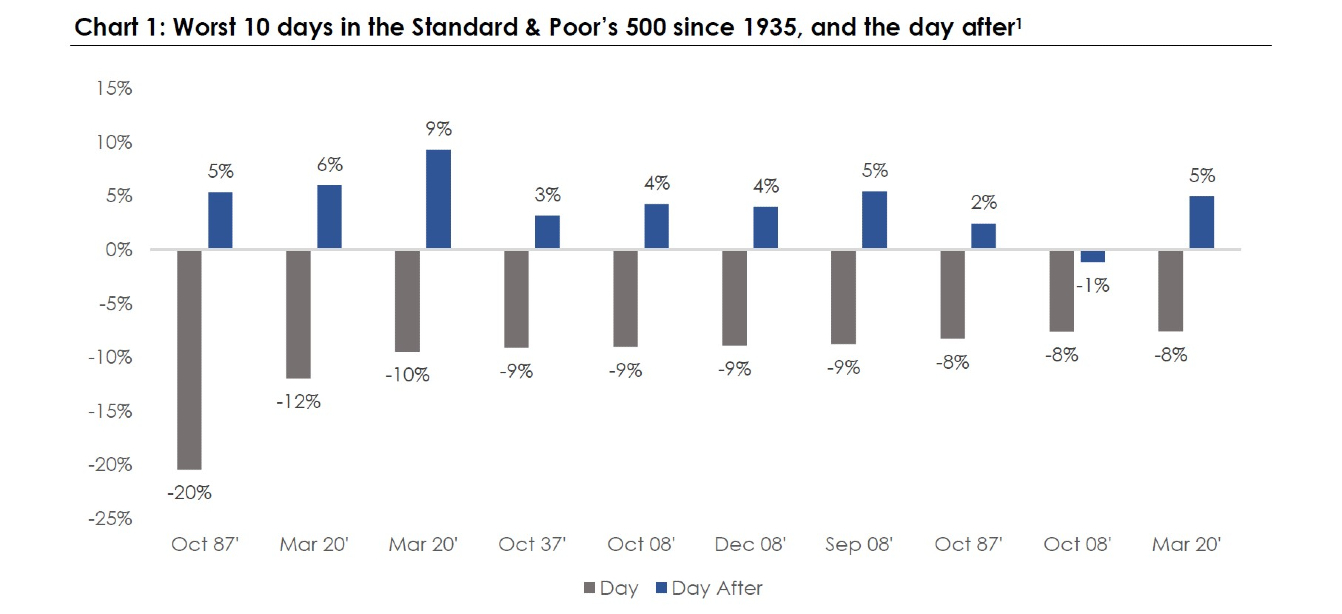

Chart 1 is one of my favorite demonstrations of the difficulty of timing markets.

Chart 1 simply shows the worst 10 days in the S&P 500 since 1935, and then the day after. Two important observations:

- Nine out of those ten selloffs are followed by a positive day

- The magnitude of those positive days is quite high.

The problem is insidious. When markets are down, we are blasted with bad news, we then check our account values, which then leads to an emotional reaction, which then leads to wanting to avoid the pain, which then (sometimes) forces an emotional decision to sell. As Chart 1 demonstrates, this is often the worst possible moment to sell because an investor is not only locking in the loss they just endured, but quite possibly missing out on the bounce back that is about to occur.

Will markets move higher immediately after this recent selloff? I have no idea … candidly, no one does, but I do know that selling after those losses is likely to make my portfolio worse off, not better off.

Markets go down (occasionally)

The second lens I would like to offer is one of perspective. First and foremost, let us establish that there has been no greater creator of human wealth in history than the U.S. equity markets. U.S. equity markets have generally beaten inflation materially, and for those that remained invested, produced sizable gains over the past two hundred years.

Yet, the process of markets going down is both healthy and needed. It allows for the redistribution of assets from those companies that are unsuccessful and unproductive to those that are successful and productive. It forces those companies who have taken too much risk to be held accountable, and it incentivizes companies to take prudent decisions (how much debt, how much speculation, etc.).

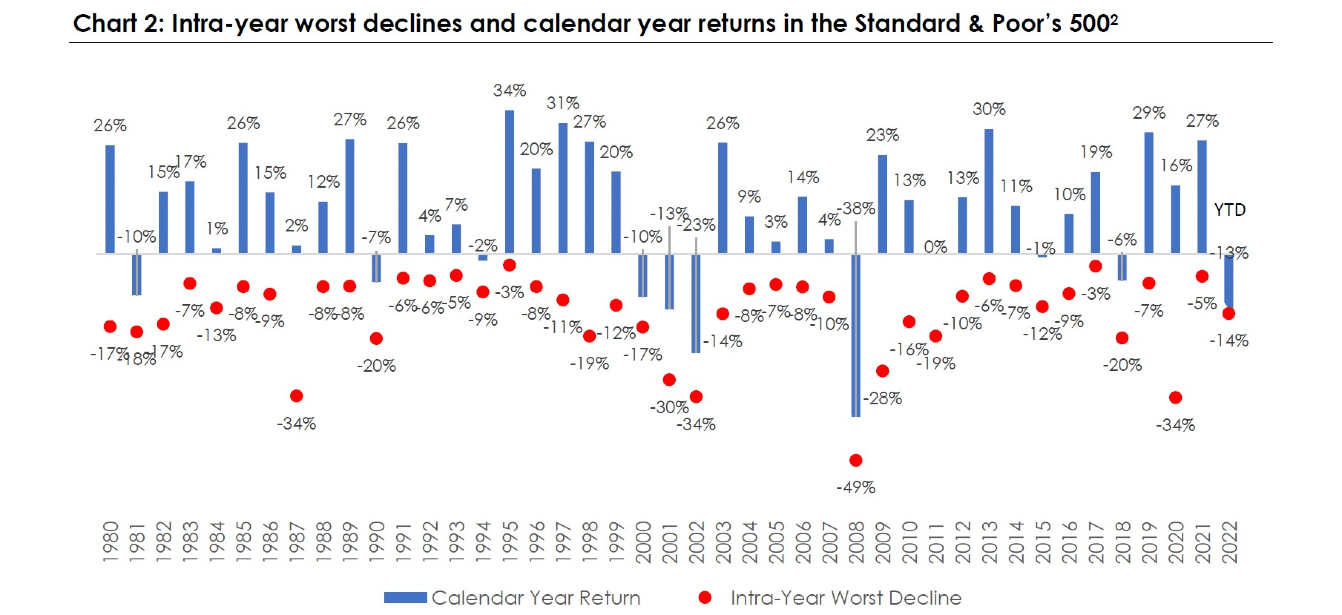

Chart 2 helps to make this point.

This chart shows two very simple numbers going back to 1980. The first (the red dot) is the worst selloff during each calendar year. The second (blue bar) shows how the S&P 500 performed during each calendar year (from Jan. 1 through Dec. 31).

I find this helpful for two primary reasons.

- Every single year has a selloff. Some are more severe than others of course, but every single year markets go down.

- Markets tend to reward investors during most years. Over this time period on average markets returned more than 9 percent per year, materially above inflation.

It’s hard to find rocks to hide under

For this last perspective, I offer the problem of alternatives.

Said another way, even if we could time markets well (we can’t), or could get over the tax implications (we can’t do that either), the question is where would we put those dollars to use? Let’s go through the main categories of possibilities:

- Cash – With inflation at more than 8 percent, cash is currently a wealth eroding asset. Based on current market dynamics, the cash sitting in your pocket today will be able to purchase 8 percent less in a year from now. In short, it’s a very challenged asset right now for reasons other than emotional (always very valid), or short-term spending and tax needs.

- Bonds – As rates rise, nominal bond prices fall. As we have seen, rates are rising and will likely continue to do so. Bonds currently have higher yields than they did several months ago (which makes them much more attractive), but they still contain a good deal of downside risk and are also yielding far less than inflation (more on this in coming updates).

- International stocks – Not an unreasonable path, but we currently don’t see much incentive to over allocate internationally. There are clearly geopolitical dynamics at play that are difficult to navigate and valuations across Europe, Asia, and South America are generally not attractive enough to justify large (or oversized) exposures.

- Commodities – Helpful diversifiers occasionally, but with prices so volatile, and already so inflated, it is very hard to justify making large allocations now. Remember, commodities have no natural positive drift so their primary benefit is diversification, not return generation.

- Real Estate – Again, prices are so inflated it is hard to justify buying in at these levels. They are generally attractive in rising inflation time periods, but price matters and while real estate can be a wonderful part of a portfolio, it is challenging to be over-allocating during an environment when rates are rising.

Therefore, let us summarize what we have explored thus far.

- Markets are very difficult to time well and historically selling when markets fall is likely to miss the times when markets rise.

- Market selloffs have historically occurred every year and will likely continue to occur in the future. Despite that reality, markets over the long-term often reward those that remain invested.

- There are no obvious “deals” to be had.

Therefore, let us instead focus on what we can control. The world is a dynamic, remarkable, and often times confusing place to invest. The asset classes at our fingertips are incredibly useful, but occasionally go down, and therefore, our primary mode of operating should be to stay the course.

Resist the urge to sell during volatile periods. Focus on mitigating taxes, reducing expenses … and if anything, use this period to refocus on the plan put in place to grow your wealth and the wealth of your family.

Discover more from MassMutual …

When markets dive, keep your strategic calm

How higher interest rates may hit consumers

How COVID-19 could shape the way we save, spend, and invest

_________________

1 Source: Bloomberg, as of May 6, 2022.

2 Source: Bloomberg, as of May 6, 2022.