The third quarter began with short-lived relief in equity markets and Treasury yields, but unfortunately concluded with the S&P 500 dropping to new year-to-date lows and Treasury yields surging to their highest levels in more than a decade. Despite many signs that price pressures are slowing, it is not happening fast enough for the Federal Reserve, and we have a long way to go to get to two percent inflation. The clear message from the Fed to the dismay of investors, is that there will be no “pivot” and that interest rates will remain “higher for longer” to squash record inflation. Meanwhile, the European Central Bank has struck a similar tone despite an unprecedented energy crisis and rising probability of a near-term recession. At the same time, COVID interruptions continue to derail China’s economic recovery, and the U.K.’s tax overhaul plan sent its currency and government bonds into a tailspin.

For investors, there has been nowhere to hide. Global equity indices are down anywhere from 15-25 percent across the developed world, and with 2022 only three-quarters over, this is the worst year in history for bond market returns. A year ago, investors could earn a measly 30 basis points on two-year Treasury notes. Now, they can earn over 4 percent! This compares to a dividend yield of less than 2 percent on the S&P 500. The U.S. economy, for now, still looks to be avoiding recession, but the impacts of tighter monetary policy will take several months to years to work their way through the system, setting us up for potentially more uncertainty and volatility in 2023.

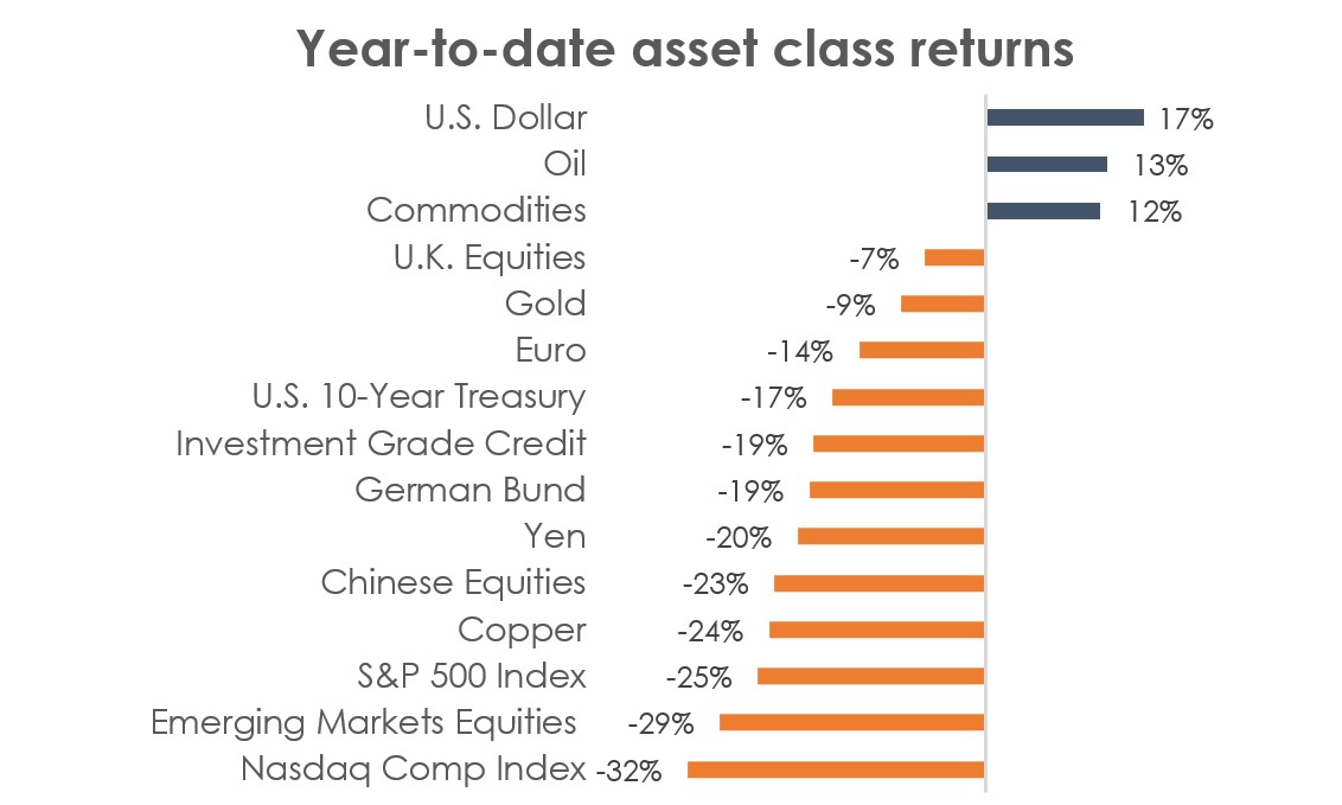

Source: Bloomberg as of Sept. 30, 2022.1

Federal Reserve unequivocally hawkish

U.S. economic resilience has been a double-edged sword. Despite ongoing fears of recession, the U.S. economy and labor market have held up better than expected over the last several months in the face of higher interest rates and persistent inflation. However, this economic strength has made the Fed more emboldened to press on with interest rate hikes. Although the U.S. consumer price index slowed in July and August, inflation is still running at an annualized rate of 8.3 percent.

At the beginning of the third quarter, investors were expecting the terminal Fed Funds rate to peak at 3.50 percent in early 2023. Now, after Chair Powell’s hawkish Jackson Hole speech and revised Fed forecasts provided at the September meeting, interest rate markets expect the Fed Funds rate to reach 4.50 percent by early next year. This compares to the current target Fed Funds rate of 3.25 percent.

Interest rates soar across the globe

The repricing of Fed interest rate hike expectations along with the Fed now beginning to shrink its $8.8 trillion balance sheet by $95 billion per month have contributed to an unrelenting surge in Treasury yields. It is hard to believe that as recently as March, the Fed was still buying Treasurys and expanding its balance sheet when inflation was also around 8 percent. The move from artificially low interest rates to more “normal” levels is a global phenomenon as central banks aggressively tighten to fight inflation. Around two years ago, there was over $18 trillion of negative yielding debt; now that number stands at less than $2 trillion. The European Central Bank and Bank of England are taking similar actions to the Federal Reserve despite their economies facing enormous energy and economic challenges due to Russia’s war in Ukraine. The big outlier is the Bank of Japan, which has maintained accommodative monetary policy, resulting in a very weak currency.

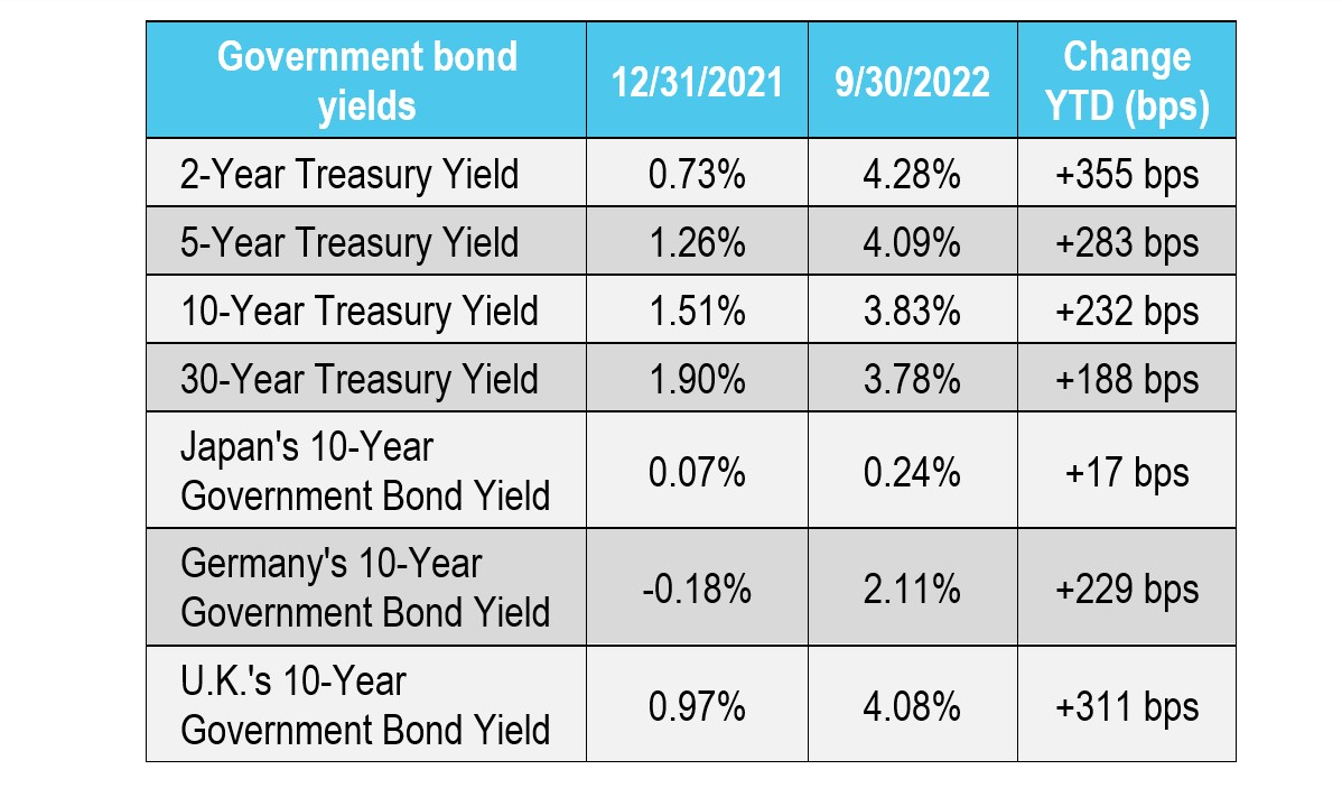

Source: Bloomberg as of Sept. 30, 2022.

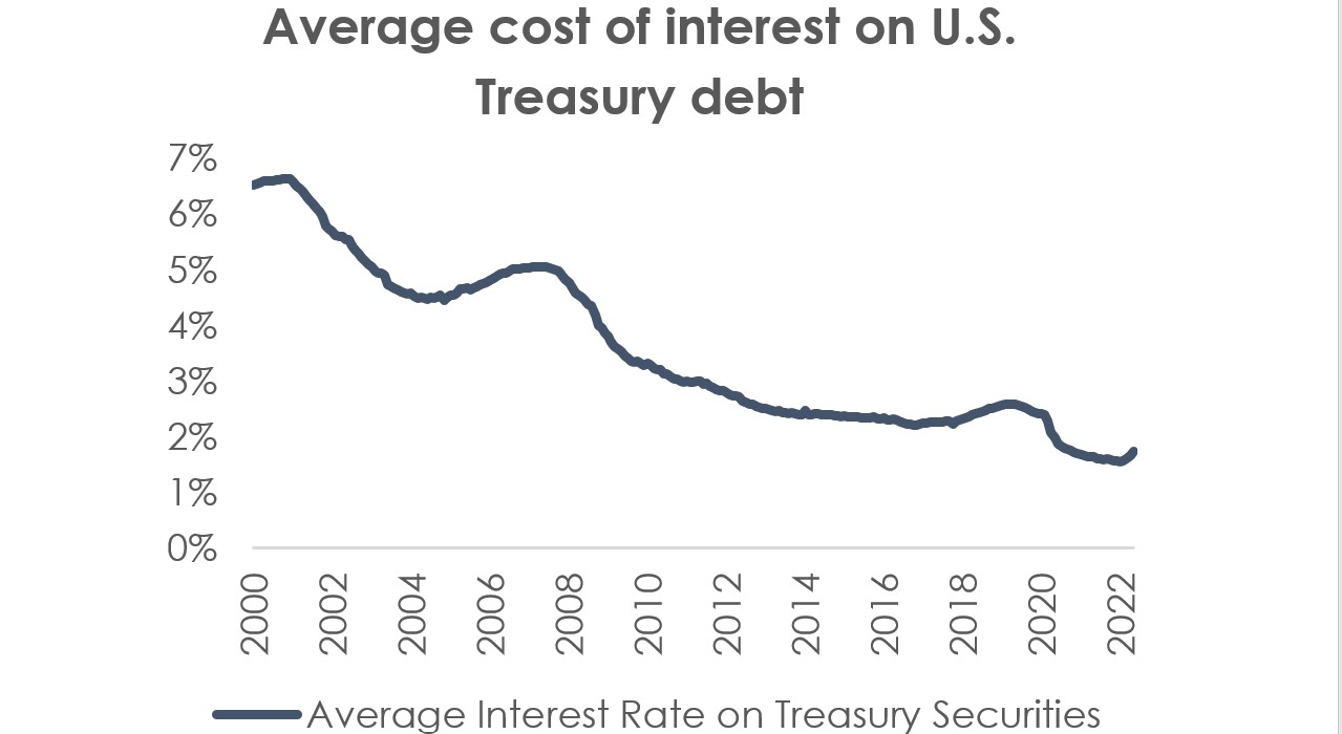

The cost of debt has risen substantially because of rising interest rates for households, corporations, small businesses, and the largest borrower of all, the government. In fact, the U.S. government has enjoyed an average interest rate on its debt of less than 3 percent since the Global Financial Crisis and less than 2 percent in the last two years. These low-cost debt levels are likely to rise with Treasurys now yielding around 4 percent. According to the Committee for a Responsible Federal Budget (CRFB), the Fed’s September rate hike of 75 basis points alone will add $2.1 trillion to government deficits over the next decade. Although it is necessary for the Fed to fight inflation, higher interest rates and the Fed no longer purchasing Treasurys are very challenging for the U.S. government budget.

Source: Bloomberg as of Sept. 30, 2022.

Lastly, as we wrote last quarter, rising interest rates have rendered “TINA” or “there is no alternative (to stocks)” no longer applicable. Fixed income yields have grown more attractive since then as investors can earn more than 3.75 percent on six-month Treasury bills, 4 percent on two-year Treasury notes, over 5 percent on investment grade corporate bonds, and close to 10 percent on certain high yield corporate bonds. The investment landscape has changed dramatically.

Mortgage rates double; housing market falters

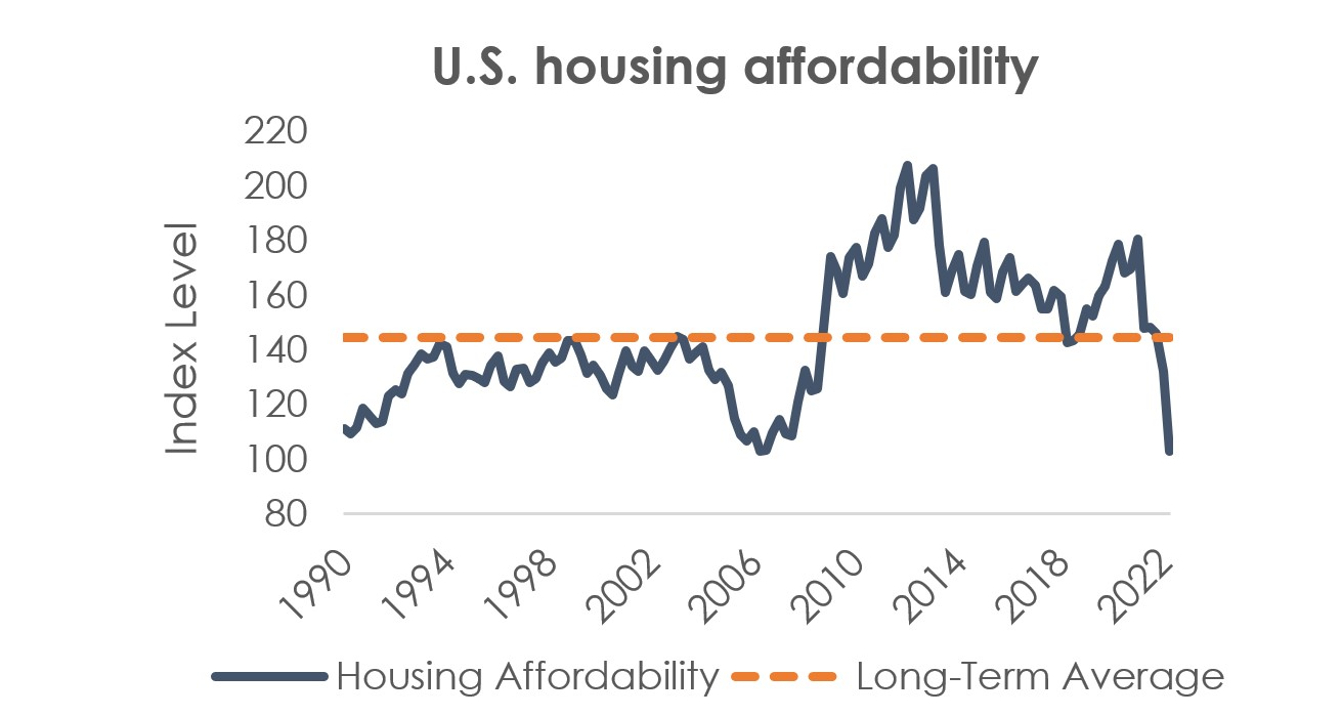

Thirty-year conventional mortgage rates have skyrocketed to their highest levels since 2001 and have surpassed an astounding 7 percent. The much higher cost of a mortgage is impacting U.S. home prices, which cooled in July at the fastest rate in the history of the S&P CoreLogic Case-Shiller Index. Home prices in July were still higher than they were a year ago but fell 0.4 percent from June levels. Housing affordability has rapidly deteriorated and sits at its worst level since 2006.2 The annual mortgage payment as a percentage of income increased to 24.5 percent this July from 17.1 percent a year ago, due to higher home prices and higher mortgage rates.

Source: Bloomberg as of Sept. 30, 2022.

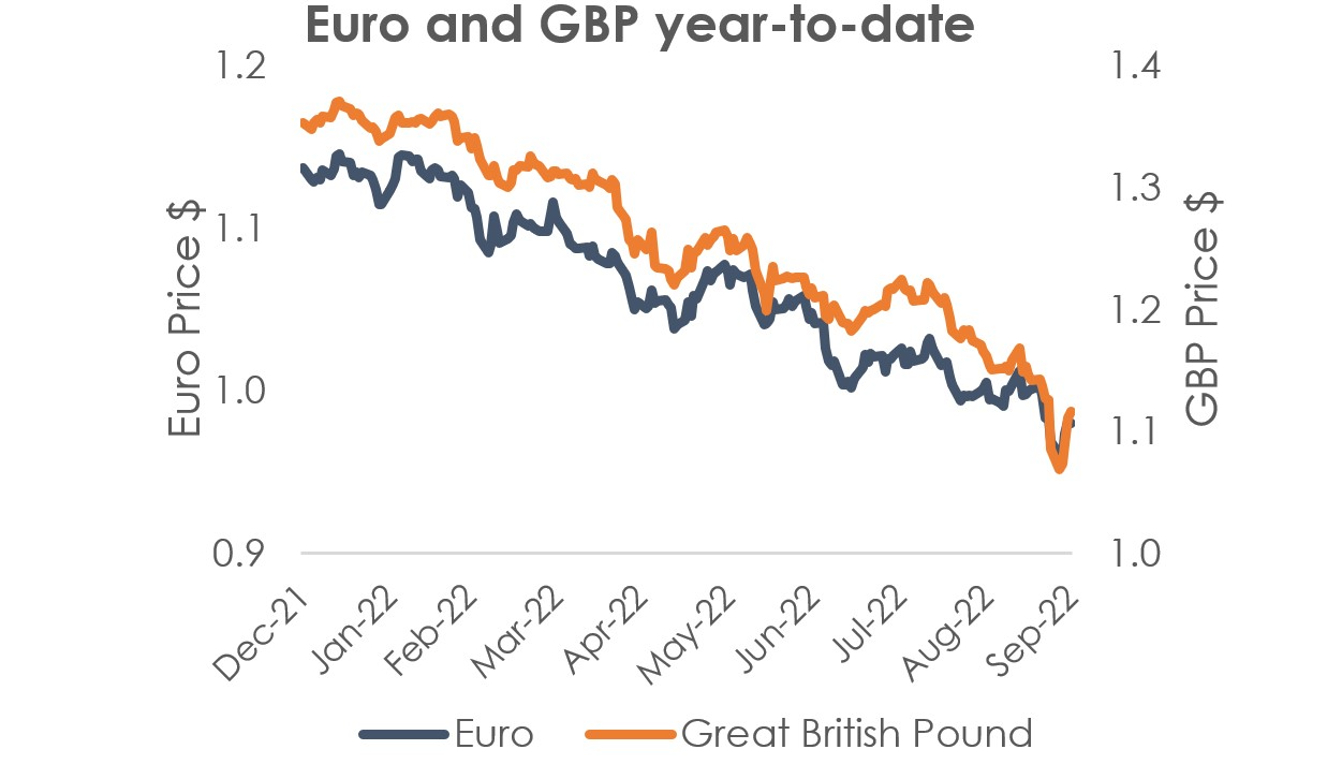

U.S. dollar dominates

Fed tightening and relative U.S. economic strength as foreign countries face their own economic turmoil has resulted in record U.S. dollar strength versus nearly all major currencies. The Dollar Index has risen 17 percent year-to-date as the euro, which is used by nineteen European countries, recently fell to below parity with the dollar for the first time since 2002, and the U.K. pound sterling fell to its weakest levels in history versus the dollar.

Source: Bloomberg as of Sept. 30, 2022.

For the U.S. economy, dollar strength is good news as it means imports are cheaper, and thus is disinflationary. However, for U.S. companies with foreign operations, it means their dollar profits are shrinking. S&P 500 companies get around 30 percent of their sales from outside the U.S. The impacts of a stronger dollar are even worse news for European economies which are forced to import energy and are already battling sky-high inflation. In emerging market countries battling food crises, the stronger dollar is increasing the cost of imported food. Lastly, for economies with dollar-denominated debt, it is making it more expensive for them to service their debt.

Equities sell off on higher interest rates and earnings uncertainty

The persistent rise in interest rates continues to depress equity market valuations as cash flows are discounted at higher rates. Furthermore, there is significant uncertainty over earnings. Although earnings have held up well over the past several quarters, much of the strength has been driven by the energy sector, and expectations for 2023 remain muted. The average of Wall Street top-down forecasts calls for S&P 500 earnings per share growth of just over 2 percent in 2023 with some strategists forecasting earnings to contract in 2023 as higher borrowing costs, a weak economic backdrop, higher input costs, and a stronger dollar weigh on corporate earnings.

Source: Bloomberg as of Sept. 30, 2022.

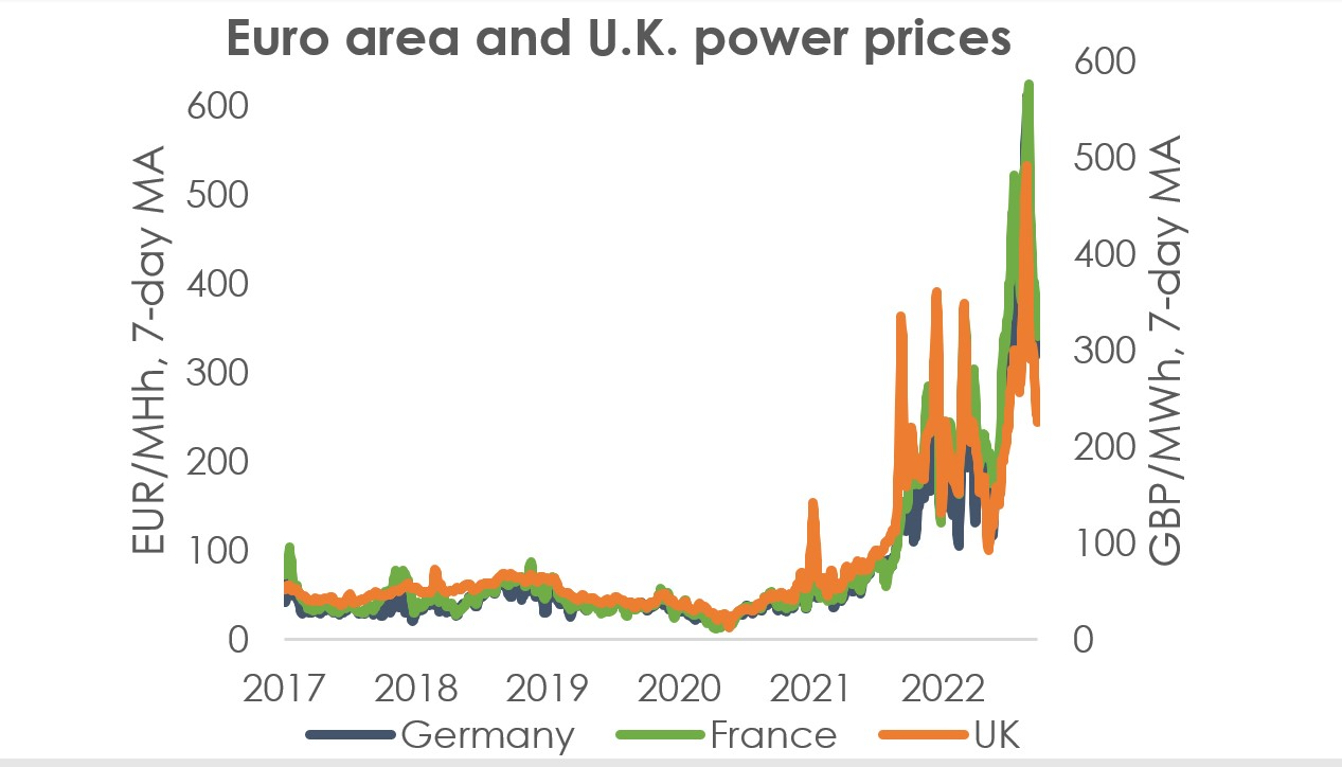

As mentioned above and in our previous letter, the energy sector has been the primary engine of earnings growth. Oil prices have retreated from recent peaks, a welcome sign for household purchasing power and overall inflation, but they remain elevated alongside natural gas prices. The energy situation is exceptionally bleak in Europe where natural gas prices in Europe have reached 6-8 times the levels in the U.S.—the equivalent of the US paying $50 for a barrel of oil and Europe $300-400. As the northern hemisphere heads into colder months, we could see another spike in energy prices, and Europe is likely moving towards energy rationing as supplies tighten.

Outlook

We have likely not seen the complete impact of the historic moves over the past several months in bond and equity markets, currencies, and commodities on the economy and financial market players. Looking ahead, volatility is likely to persist, and the actions and words of the Fed will remain one of the most dominant drivers of financial markets. With the Fed pledging to hike interest rates further and keep them elevated for an extended period of time, the U.S. economy is set to continue to slow, leaving it susceptible to recession in 2023. In order for the Fed to change course, inflation will need to substantially decrease and/or we would have to see significantly more economic deterioration. Markets could snap back abruptly if the Fed indicates it is done raising interest rates or signals a significant policy shift.

Equity, bond, and real estate market valuations have come down, but are not at levels we would characterize as “cheap,” creating a challenging backdrop for investors. Corporate earnings also remain susceptible to further downgrades, which would be a further drag on future equity returns. The COVID downturn was short-lived and unique for many reasons, including the enormous amount of fiscal and monetary policy support that at least partially precipitated recent inflation pressures. The next economic downturn we face is likely to be very different as policymakers are likely to be constrained by inflation risks.

Looking back, we have not been through an extended downturn since the Global Financial Crisis more than a decade ago. We expect the next downturn will be unique in itself as we think about the changes in the economy and markets that have occurred over the past several years. On the positive side, corporate and household balance sheets have elevated levels of cash, helping them to weather a downturn. Nevertheless, there are still likely to be pockets of weakness such as highly levered companies and subprime borrowers who have been most negatively impacted by high inflation. In uncertain and unique times such as these, it is increasingly important to work with a financial professional. We look forward to reporting back to you in early 2023.

Discover more from MassMutual …

Investing basics: What everyone should know

5 ways to prepare for an economic downturn

Income tax diversification defined

___________________

1 U.S. Dollar = DXY Dollar Index; Oil = Brent Crude Oil Spot Price; Commodities = Bloomberg Commodity Index; U.K. Equities = FTSE 100 Index; Gold = Gold Spot Price; Euro = Euro Spot Price; U.S. 10-Year Treasury = S&P U.S. Treasury Bond Total Return Index, Investment Grade Credit = Bloomberg U.S. Corporate Investment Grade Bond Index; German Bund = Euro Bund Futures Price; Yen = JPY/USD Spot Exchange Rate; Chinese Equities = Shanghai Shenzhen CSI 300 Index; Copper = CME Copper Futures Price; S&P 500 Index = S&P 500 Index; Emerging Markets Equities = MSCI Emerging Markets Index; Nasdaq Comp Index = Nasdaq Composite Index

2 A higher level of the affordability index indicates that a family can more easily afford a median-priced home.