| ||||||||||||

Having a disability, whether temporary or long term, could mean navigating life differently than people who don’t share your physical, cognitive, emotional, or financial challenges. But it doesn’t mean that all the doors of opportunity slam shut — educational or otherwise — and leave you on the other side, rattling the doorknob.

If you rely on federal disability benefits for income, though, you probably don’t have the cash flow or the savings to pay for higher education outright. So, how will you pay for the degree you want?

Fortunately, there are options — albeit with rules and requirements. Some can get complex. A financial professional with a background in disability benefits and financial aid may be able to help sort out the advantages and disadvantages of the alternatives for specific situations.

Connect with a MassMutual financial professional

But first, it’s important to understand what’s available.

Federal student aid and disability

“People receiving long-term disability income from Social Security can still qualify for federal student loans,” said Kristen Moon, founder and CEO at Moon Prep, an educational consultancy based in the greater Atlanta area that guides parents and students through the U.S. college admissions process.

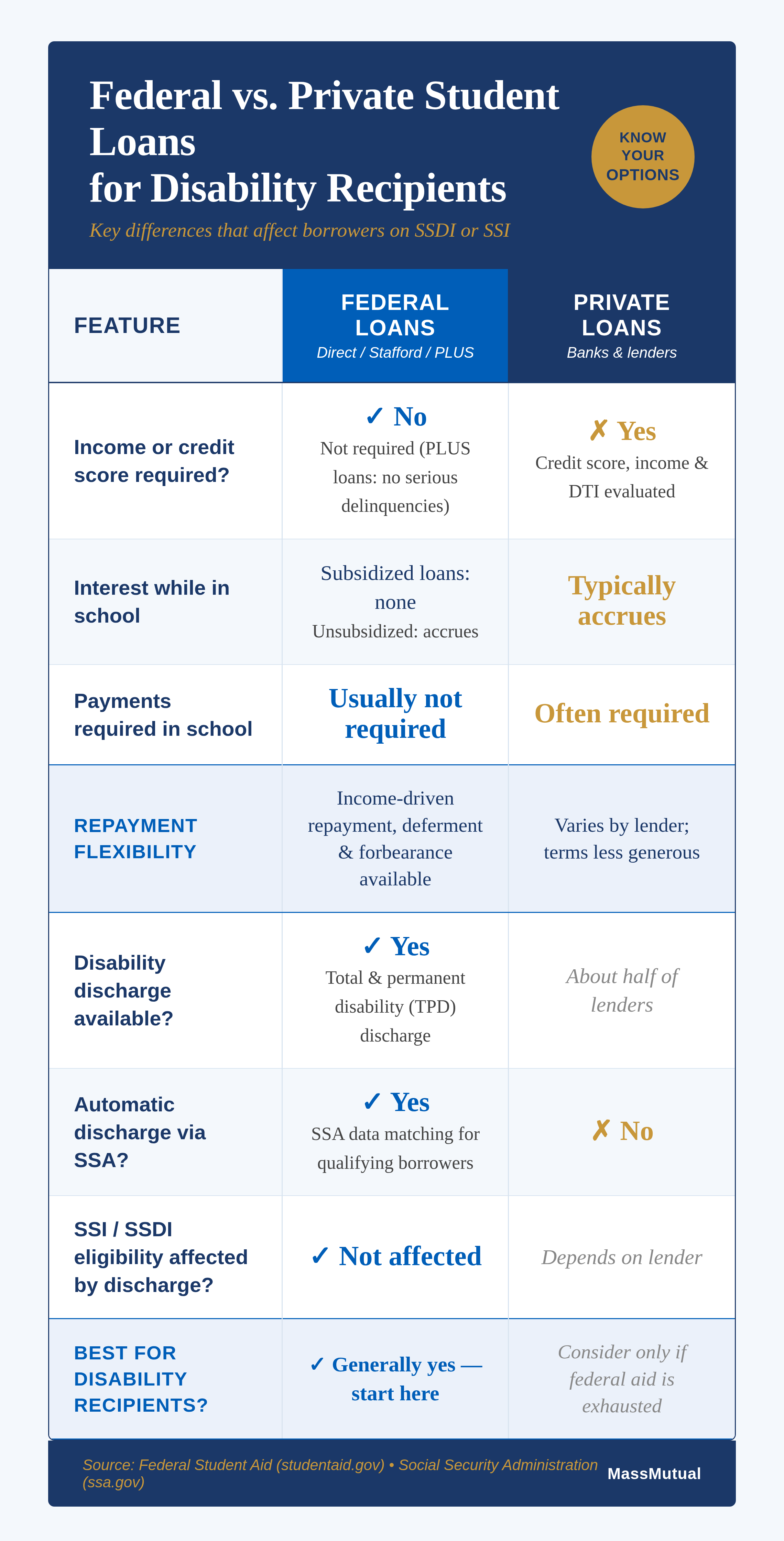

Anyone who wants a federal student loan must submit the Free Application for Federal Student Aid (FAFSA). Federal student loans are the first resource experts recommend any student apply for when scholarships, savings, and income aren’t enough to cover college costs.

You don’t need a certain income or credit score to qualify (though parent and graduate student PLUS loans aren’t an option for those with serious delinquencies). Certain loans don’t accrue interest or require payments while you’re in school, and federal student loans offer relief such as deferment, forbearance, forgiveness, income-driven repayment (subject to current program availability), and total and permanent disability discharge (TPD) to those who qualify.

When you complete the FAFSA, you don’t report certain untaxed income. This includes all Supplemental Security Income (SSI) and untaxed Social Security benefits. Social Security benefits aren’t taxable unless your income exceeds a certain level.

The FAFSA must be filed each academic year and has state and institutional deadlines that may be earlier than the federal deadline.

Taxation of non-federal disability aid

What about private disability benefits? If you receive income from a disability insurance policy, it’s generally taxable if you or your employer paid the premiums with pretax dollars. It’s generally not taxable if you paid all the premiums yourself.

Certain types of assets that individuals living with disabilities might have — such as ABLE accounts, special-needs trusts, home equity, life insurance policies, and retirement accounts — also don’t count for FAFSA purposes. Getting a federal student loan is generally your best bet if you’re on disability.

You’ll need to be aware of an important caveat that could affect you if your disability hinders your ability to get work done.

“Students who want to remain eligible for student loans will still need to progress toward their degree and remain in good academic standing,” Moon said.

This means you’ll need to earn a certain number of credits per year and maintain a certain grade-point average. School policy, not the federal government, sets the specific standards students need to meet. (Related: Is student debt worth it? A cost-benefit analysis of college)

People with intellectual disabilities and federal student aid

Intellectual disabilities are usually diagnosed in childhood, and people with intellectual disabilities often receive disability income from federal SSI and Social Security Disability Insurance (SSDI) programs.

“Students with intellectual disabilities will have additional requirements for eligibility for student aid,” Moon said. “They must be enrolled or accepted for enrollment in a Comprehensive Transition and Postsecondary (CTP) program that also participates in federal student aid programs.”

A CTP program helps students with intellectual disabilities complete a degree, certificate, or non-degree program alongside students without disabilities to prepare for employment. Students need not have earned a high school diploma to participate.

Programs have academic advising, a structured curriculum, and are approved by the U.S. Department of Education. CTP programs are available at select universities in most states; at the time of this article, they are not available in Alaska, Arizona, Hawaii, Maine, Nebraska, New Hampshire, North Dakota, or Vermont.

CTP programs are also structured to open up access to federal student aid for students with an intellectual disability, on the condition that they are also attending one of the approved CTP programs.

If you demonstrate financial need, you may receive a Federal Pell Grant, Federal Supplemental Educational Opportunity Grant, and a federal work-study job. In other words, fewer sources of federal aid are available, but none of them will put you in debt. (See: How to craft a financial strategy for your special-needs family)

Qualifying for private student loans

Private student loans are not nearly as easy to get as federal student loans.

You might not qualify for a private student loan if you don’t want to use your disability income to help qualify — unless you have a creditworthy cosigner, said Mark Kantrowitz, a student loan expert and the author of How to Appeal for More College Financial Aid and Who Graduates from College? Who Doesn’t?

“Lenders consider the borrower’s — and cosigner’s, if any — credit scores, income, debt-to-income ratio, and duration of employment with the current employer, among other factors,” Kantrowitz said. “If the borrower does not satisfy these credit criteria, it may be difficult for them to qualify for a private student loan.”

In addition, private student loans don’t have the advantages of federal student loans when it comes to repayment.

Private student loans may accrue interest and require monthly payments while you’re in school, and you won’t have access to an income-driven repayment plan. If your disability worsens and you struggle to make your payments, a private lender may offer you deferment or forbearance, but the terms may be less generous compared with federal loans.

You may be more likely to accrue late fees, additional interest, and, eventually, collection fees if you have trouble repaying a private loan compared with a federal loan.

Missed payments and defaults on either type of loan will hurt your credit score, making it more difficult to get a credit card or buy a home.

Student loan discharge for disability

“Anytime you borrow money with a student loan, you need to plan for repayment,” said Elaine Rubin, a financial aid expert with Edvisors in Las Vegas. “It will be up to the individual to understand their ability to repay the debt.”

However, disabilities sometimes get worse. You should know what relief might be available in a worst-case scenario for a student loan forgiveness disability situation.

Federal student loans can be discharged if you have a total and permanent disability, meaning your condition has already lasted for 60 continuous months (five years), it’s expected to last that long, or it’s expected to result in your death — and you can’t perform any substantial gainful employment because of your physical or mental impairments. (The federal government sets a monthly earnings threshold for substantial gainful activity, which is updated annually and available at ssa.gov.)

For private student loans, it’s up to the lender. About half offer this type of disability discharge, according to Kantrowitz.

“If a private lender doesn’t offer discharge, then a borrower’s options may be limited — and that can create a financial burden,” Rubin said.

Also, Moon noted that the process for proving a disability can be confusing and lengthy, particularly with private student loans.

The process can be simple with qualifying federal student loans. The government uses data matching to identify student loan borrowers who are also receiving SSDI or SSI benefits and whose next scheduled disability review is in five to seven years. These borrowers are presumed totally and permanently disabled and will have their loans automatically discharged — unless they opt out — without having to submit an application.

Why would anyone opt out? Someone currently in school and receiving student loans or someone hoping to secure federal student loans in the future might opt out to preserve their loan eligibility without having to jump through administrative hoops.

Once you receive a total and permanent disability discharge, you have to take additional steps to become eligible for federal student loans again. You also have to wait three years or your previously discharged loans could be reinstated. The income-based component of this monitoring period — which could reinstate loans if your earnings exceeded a federal threshold — was permanently eliminated by the Department of Education in 2023. However, a three-year window remains during which taking out new federal loans or a TEACH Grant could trigger reinstatement of previously discharged loans.

If you aren’t eligible for automatic discharge through SSA data matching, you can still submit an application with supporting documentation from a an authorized medical professional. Borrowers can submit TPD applications and track their status at StudentAid.gov.

Discharge does not change your eligibility for SSDI or SSI benefits. Veterans rated with a 100 percent permanent and total disability by the Department of Veterans Affairs also qualify for automatic TPD discharge.

Federal law permanently excludes TPD student loan discharges from gross income. This means the discharged amount is not counted as taxable income by the IRS. But some states may still treat the discharged loan balance as taxable income.

Student loans and maintaining eligibility for disability income benefits

Generally speaking, you can accept funds to pay for your education without damaging your SSI eligibility, provided you follow SSI income and resource rules.. You can receive grants, scholarships, fellowships, or gifts from any source, and they won’t affect your eligibility for federal benefits if you spend the money on educational expenses within nine months. There’s no time limit on how long you have to use federal aid such as Direct loans and Pell grants. However, state administered benefits and Medicaid-related programs may have separate rules.

You can even earn income as a student — up to $2,410 a month and $9,730 a year in 2026 — without reducing your federal benefits thanks to the student earned income exclusion for those under age 22. You must be attending college classes for at least eight hours a week to qualify.

Conclusion

Despite your disability, earning a degree can put you on a path toward a job that accommodates and perhaps even celebrates your differences.

Fortunately, you can still qualify for federal student aid, and possibly private student loans, if you rely on disability income from an insurance policy, state benefits, or federal benefits. Further, receiving financial aid and student loans won’t jeopardize your disability income if you understand and follow the rules. An experienced professional can often help sort out options when formulating a plan.

___________

Frequently Asked Questions about student loans and disability

Q. Can I get a student loan if I receive Social Security disability benefits?

A. Yes. People receiving SSDI or SSI can qualify for federal student loans by completing the FAFSA — and SSI and untaxed Social Security income do not need to be reported on the application. SSDI or other Social Security benefits may be treated differently depending on taxability and current FAFSA reporting rules, so applicants should follow the FAFSA instructions for the applicable aid year.

Q. Will taking out student loans affect my SSI or SSDI benefits?

A. Federal grants and loans generally will not affect your SSI eligibility as long as you spend the funds on educational expenses within the required timeframe. Discharge of your student loans also does not change your eligibility for SSDI or SSI benefits.

Q. What is a total and permanent disability discharge?

A. A TPD discharge cancels your remaining federal student loan balance if you have a qualifying disability — one that has lasted or is expected to last at least 60 continuous months, or is expected to result in death, and prevents substantial gainful employment. You can apply at StudentAid.gov or qualify automatically through SSA data matching.

Learn more from MassMutual…

A resource guide for adults with a sudden disability

Is disability income insurance worth it?

Helping young adults recover financially from cancer

This article was originally published in July 2023. It has been updated.

______________________________________

For information about SSI go to http://www.ssa.gov/ssi/. Information is available by telephone, mail, in person at an office. The toll–free number is 1–800–772– 1213.