| ||||||||||||

Right now, if your estate is worth less than roughly $14 million (about $28 million for a married couple), you don’t have to worry about your heirs paying a federal estate tax. But that’s likely to change next year.

And that isn’t very long when it comes to setting up an estate plan.

“In my opinion, everybody should be planning now,” said Matthew DelPriore, director of financial planning at Fortis Lux Financial in New York City. “And it is not just the ultra-wealthy who need to be concerned.”

Of course, knowing exactly what to plan for would make such a task easier. But Congress isn’t likely to make it easy.

What’s going away?

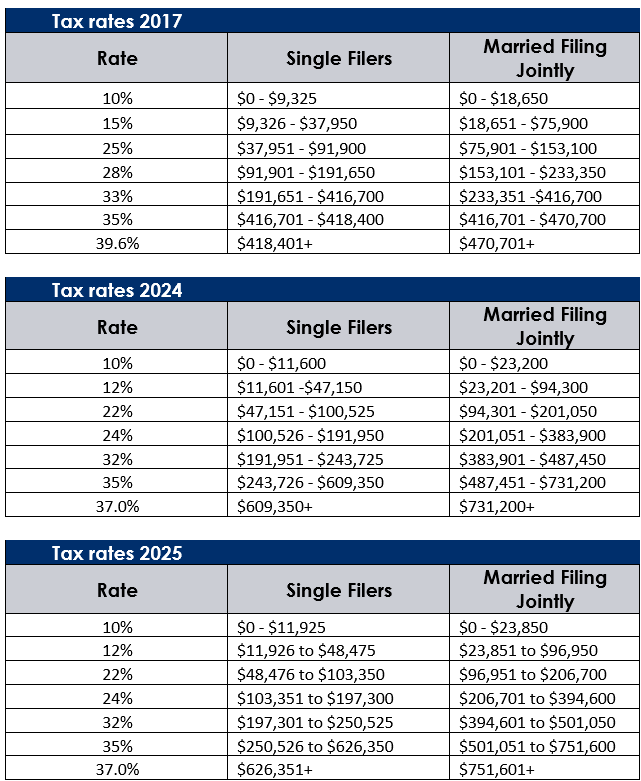

The current estate tax exemption was created under the Tax Cuts and Jobs Act of 2017 (TCJA), which more than doubled the existing exemption at the time. Initially set at $5,490,000 ($5,000,000, indexed for inflation) for an individual and $11,180,000 ($10,000,000, indexed for inflation) for a married couple, the new exemption has been adjusted upward for inflation every year since and currently stands at $13.99 million ($27.98 million for couples) for 2025.

But those higher exemptions are deemed temporary and set to expire at the end of 2025, reverting back to 2017 levels, adjusted for inflation (roughly $6 million to $7 million depending on inflation final levels in 2025 and 2026).

Unless, of course, Congress acts. And it’s likely that it will, especially since the lower income tax brackets set out in the 2017 TCJA will also expire, drawing attention from many constituencies.

The question then becomes, what will Congress do? That, of course, is impossible to predict, especially with budget battles still in the offing. (Related: How to financially prepare for an election)

But a range of possibilities exist, from:

- Allowing expiration of the current exemptions and tax brackets and reverting to 2017 levels.

- Extending the current state of exemptions and brackets.

- Creating a whole new exemption and tax regime.

Given the close balance of political parties in Washington and the wide-ranging promises and priorities outlined by various office holders in the latest election cycle, it's hard to predict where exactly things will end up. (Related: The Social Security funding dilemma)

What to do

Still, in the vein of preparing for the worst while hoping for the best, many financial professionals suggest preparing for the sunset of the larger exemptions and current tax brackets. To do that, they point to three broad areas for possible action:

Of course, what any individual or family should do in these areas will depend on specific circumstances and goals. But understanding the possibilities in these broad areas is a good first step and starting point for a conversation with a financial professional.

“Both annual gifting and estate planning require complex planning to ensure it is done properly,” said Douglas Collins, financial planning director for Fortis Lux Financial, adding that certain households should start taking steps soon. “The potential reduction of the estate tax exemption on January 1, 2026, could have significant implications for those with a net worth above approximately $7 million, or $14 million for couples.” (Related: Calculate your net worth)

Gifting

Gifting strategies involve transferring assets to beneficiaries during your lifetime or at the time of your passing. In 2025, individuals can gift up to $19,000 per donee ($38,000 for a married couple), or utilize their available federal exemption amount without incurring federal gift taxes providing they file a gift tax return.

"Gifting can certainly help as it allows for a reduction of your estate,” said DelPriore. “Don’t forget it’s an annual gift limit of $19,000 per person (in 2025). This allowable amount is a ‘use-it-or-lose-it’ gifting opportunity. If you don’t take advantage of this in a given tax year, it does not carry forward.”

“Depending on your age, leveraging the annual gift exemption can accomplish a lot over the years considering a person could have gifted up to $18,000 in 2024 ($36,000 for a couple) to as many people as they want,” added Collins. “For instance, a couple with three kids and six grandkids could have given away $324,000 in 2024 without dipping into their lifetime exemption amount and these annual limits are indexed for inflation.”

But Collins also noted that people should be careful not to gift money they might actually need or want for themselves.

And financial professionals also point out that some gifts can be made without being subject to tax.

“Look for opportunities to gift to family members or friends who have medical expenses or tuition payments for higher education, as there is no cap on that amount and it is not subject to the $18,000 per year limit per person,” DelPriore added.

Trusts

Trusts are legal vehicles that allow a trustee to hold assets on behalf of a beneficiary or beneficiaries. And certain kinds of trusts can be set up using the gifting allowances outlined above to reduce your taxable estate.

One example is a spousal lifetime access trust (SLAT). This is an irrevocable trust where one spouse makes a gift into a trust that can be used to benefit the lifetime beneficiaries of the trust, often the spouse (or potentially other family members) while removing the assets from their combined estate. The trustee of the trust has discretion to make distributions of income and principal to the beneficiary spouse during the lifetime of the gifting spouse. (Learn more: Different types of trusts)

Another example is an irrevocable life insurance trust (ILIT) that is set up to pay premiums on a policy or policies covering a couple.

“I am a huge advocate for life insurance as part of the estate planning process,” said DelPriore. “Your estate is taxed based on the law at the time of your passing, which we have no control of. Life insurance held in a trust pays out tax-free and extremely quickly. It is a great source to help with estate liquidity to pay taxes or help equalize the wealth amongst your family.” (Related: Life insurance’s income tax advantages)

“In some instances, life insurance in combination with an irrevocable life insurance trust can be the most effective way to reduce and or eliminate estate taxes,” said Jeffrey R. Rotman of Rotman and Associates in Boca Raton, Florida. “Unfortunately, I have seen this strategy overlooked.”

Rotman noted that such a strategy has to be carefully planned.

“There must be no individual ownership of the policy and it must be an irrevocable transfer (to the trust),” Rotman explained. “Annual gifting can be used for premiums and the trust can be drafted to include spousal access. A survivorship life insurance policy is typically used unless there is a significant age difference. Either way, the death proceeds flow into the trust estate tax-free for the heirs in an extremely cost-efficient strategy in estate tax planning.”

Trusts can be arranged in many ways and can specify exactly how and when the assets pass to the beneficiaries. But, as a result, they can be very complex. It is usually advisable to consult a financial professional about what kinds of trusts may be appropriate for a specific situation. It is in the best interests of anyone considering a trust to do so sooner rather than later because of the expiring tax laws.

Tax planning

In addition to the possible sunset of the larger estate tax exemptions, marginal income tax brackets may be set to increase as well in 2026.

“This could be a good opportunity for people to convert traditional IRAs to Roths or make Roth contributions in lieu of pretax contributions given the fact that tax rates are increasing for most filers come 2026,” said DelPriore. “If you have a sizable charitable donation that can wait until 2026, it may be wise to do so given your tax deduction will possibly be more valuable given a higher potential tax bracket.” (Related: Roth IRA conversions explained)

The potential rise in income tax could be particularly adverse for retirees who are required to take required minimum distributions (RMDs) from IRAs or other qualified plans as well as cause taxation on Social Security benefits.

The deduction landscape could also change significantly. The 2017 law eliminated or limited many deductions but doubled the standard deduction. That resulted in many more people taking the standard deduction and avoiding the complicated process of itemizing for deductions. Absent legislative action, it may make more sense for some people to resume itemizing.

Also, the alternative minimum tax (AMT) may hit more people. The AMT is another way to calculate taxes. Taxpayers are required to calculate their taxes under both regular rules and the AMT system, then pay the higher total. Under the 2017 law, the amount of income exempt from the AMT calculation was increased. Those exemptions are also set to expire at the end of 2025.

Consulting a tax expert or financial professional about possible income tax diversification strategies in the face of such potential changes could make sense for some people.

Conclusion

As noted, the sunset of the current estate and income tax regime is far from certain. Still, given the breadth of the potential changes, it may make sense to plan for the possibilities. That is where working with a financial professional can be an advantage.

Since 1851, MassMutual has been focused on helping people secure their future and protect the ones they love. That purpose is why we have thousands of financial professionals to assist you on your journey through insurance, investing, retirement planning, estate management, and more. You can find a MassMutual professional with this tool or you can let us know you’d like to talk to one and we’ll have one of our financial professionals contact you.

Discover more from MassMutual …

How life insurance can help you in retirement

Understanding asset allocation

Asset location strategy: Tame your taxes

This article will originally published in November 2023. It has been updated.

________________________________