| ||||||||||||

Elections ― whether national, state, local, primary, or midterm ― can often lead to change, especially when it comes to finances. Governments large and small, after all, have tax policies and support programs that touch everyone’s life in one way or another. So, a change in the control of the government can change the direction of those policies.

Even if an election leads to very little change in terms of political control, there can still be implications for personal finances, especially if the country is facing a critical financial situation.

Candidates or political parties may campaign on a very precise set of policy measures, but it’s debatable whether those measures will actually come to pass. Passing legislation requires time and debate, even if one party has dominant control. And amid the compromising and horse-trading involved in the legislative process ― as well as deals sometimes upset by midterm elections or appointments ― the final product is often different, sometimes vastly so, from what was originally proposed.

So, can you prepare for any possible financial changes that may come from an election?

Yes. Here are three steps you can take to be prepared for whatever emerges.

Having these three items in hand will give you a head start in staying ahead and planning actual asset moves once any policy changes prompted by an election come to pass in taxes or support programs such as Social Security and Medicare.

Know your tax bracket

Knowing where you fall in the government tax spectrum would seem an easy thing to keep track of. But many don’t. In fact, one survey estimated that more than half of Americans have no idea how tax brackets work.

Why so tricky? The answer requires knowing two things: How much you earn in the eyes of the IRS and what the tax brackets are.

Generally, people can have a basic idea of how much they earn. Most workers get a standard paycheck statement and a yearly summary from their employer, which makes for a good starting point.

But it can get complicated quickly, depending on individual circumstances. Investment gains or losses and one-off windfalls like gambling winnings can make overall taxable earnings fluctuate. And some income from programs like Social Security can be considered taxable earnings, depending on a number of factors.

And then there are deductions and credits. These can be wide-ranging and significant, depending on individual circumstances, and have a meaningful impact on which tax bracket you climb into.

Checking your previous tax return is an expedient way for most people to track their overall income level. However, events in some years, like a pandemic or recession, can have profound economic effects on many people, which can change their income circumstances.

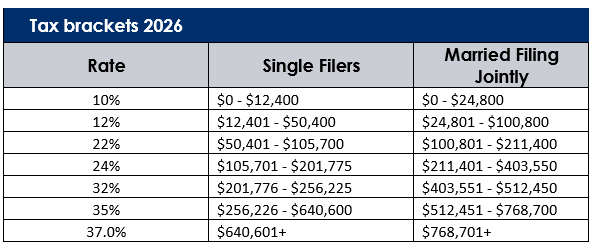

But understanding the bracket system itself can be challenging. The United States tax system is a progressive plan, meaning each level of income is taxed at a different percentage rate.

For instance, for 2025, a single person making $48,475 would have:

- The first $11,925 of their income taxed at 10 percent.

- The rest — $36,550 — would be taxed at 12 percent.

- If that person won a lottery or otherwise received additional income, it would be taxed at 22 percent up to $103,350.

The income levels applied vary depending on your marital status and how you are filing, jointly or separately. And altogether there are seven brackets for 2025, which will be adjusted for inflation in the years ahead.

But elections and changes in government priorities and policies can change where the brackets begin and end as well as the tax rate applied to each section. For instance, in 2017, the top tax rate was reduced from 39.6 percent to 37 percent for incomes over $510,301.

Indeed, the current tax brackets were the result of legislation passed in the summer of 2025. (Related: ‘Big, beautiful’ changes to review with your financial professional)

To understand what such changes, or proposed changes, may mean for your own situation requires knowing where you stand now. So, check your bracket.

Calculate your net worth

Government policy that may result from a national or midterm election and affect your finances goes beyond your yearly income. There are federal taxes and obligations on a variety of other items, like gifts or inheritances. Additionally, there are state and local taxes on assets like property or businesses. How such policies — or a change in those policies — will affect you or your loved ones begins with knowing how much you have in the first place.

- For example, do you own property? How would a change in local property taxes affect its value or your ability to hold it?

- Or, if the federal estate tax exemption (which stands at $13.99 million for 2025 and $15 million for 2026) were increased or reduced, would it affect you or your estate plans?

- Or how would a change in the federal gift annual exclusion (which currently stands at $19,000 a year per donee) affect any plans you have to help family members before you pass away?

All these questions require you to understand your net worth, basically reviewing your assets and your liabilities. Depending on your circumstances — like how much you own or the level of your investment — that can be a simple or complex task. But it’s critical to understand what you might need to address should an election mean changes to how your assets are treated. (Related: How to calculate your net worth)

There are other advantages to doing the net worth exercise as well. It will likely reveal to you how you stand versus any financial goals you have, like a secure retirement or starting a business. It will also signal whether you are carrying too much debt or not getting the desired performance out of investments.

Have a plan … and a professional

With your tax bracket and net worth in hand, you can at least roughly gauge what effect any possible changes in tax or fiscal policy might have on you. And that, in turn, can allow you to formulate a plan, or at least a rough course of action, to take should such changes come about.

For instance:

- A change in tax brackets might prompt you to take action on the deduction or income front to avoid a higher tax rate — like contributing more to a qualified retirement plan. (Related: How to avoid moving into a higher tax bracket)

- Or a change in federal estate tax exemption levels might prompt you to look at life insurance options for helping heirs handle a higher tax bill. (Related: Keeping a farm in the family)

Many people turn to a financial professional to help with such long-range estate and personal finance planning. Or, for specific tax questions, a tax specialist. An upcoming election, primary, midterm, or otherwise, is a good time to do that.

“You need to get with your financial professional to look at your individual situation, because whatever the changes may be from whatever side of the election, those changes will present both opportunities and challenges that only planning can overcome and help seize,” said J. Todd Gentry, a financial professional with Synergy Wealth Solutions in Chesterfield, Missouri.

If you have a financial professional, it would probably pay to make an appointment in advance to discuss any possible plans or changes to plans as a result of an election. Indeed, should a major change take place, time and input from financial professionals will likely be in high demand.

If you don’t have a relationship with a financial professional, it might be a good time to establish one. You can find a MassMutual financial professional near you through this tool or, if you prefer, fill out this contact form and have one get in touch with you.

Most elections mean change, in one way or another. These three steps should help you be prepared for that change.

Since 1851, MassMutual has been focused on helping people secure their financial future and protect the ones they love. That mission is why we have thousands of financial professionals to assist you on your journey through insurance, investing, retirement planning, estate management, and more.

Discover more from MassMutual …

Estate planning for high net worth households

Is setting up a trust right for you?

How to grow wealth: 3 strategies

This article was originally published in August 2020. It has been updated.

_______________________