| ||||||||||||

College costs are about to double (or worse) for many families that will have more than one child enrolled at the same time.

Starting with the 2024–2025 academic year, the discount currently available under the Free Application for Federal Student Aid (FAFSA) to families with multiple enrolled children disappeared, a byproduct of new legislation that seeks to simplify the form that determines financial aid eligibility.

Parents and students began using the new FAFSA form in October 2023.

“Starting in the fall of 2023, the calculation for determining financial aid changed, so we’re alerting our clients and working with school counselors now to make sure everyone understands the implications,” said John F. Pearson, a financial professional with Barnum Financial Group’s Center for College Planning in Stamford, Connecticut. “One of my clients has triplets — three 12-year-olds. We first brought this to her attention in an email and, after the initial digital tears were shed, we’ve started to talk about increasing her savings and doing whatever she needs to do to prepare.”

FAFSA changes: What’s new

The FAFSA form — which asks for tax return information as well as savings and investment account balances — must be completed by students each year to receive financial aid from the federal government, including grants, work-study jobs, and low-interest federal loans. It is also used by many states and colleges to determine eligibility for other forms of financial aid, including need-based loans and merit-based scholarships.

According to the College Board, roughly 17 million students submit the FAFSA each year and secure about $120 billion in grants (which, unlike loans, need not be repaid) from the Department of Education.1 (Learn more: What high schoolers need to know about student loans)

But the FAFSA form in its former iteration was complex. In a bid to encourage more low-income families to submit the form and secure federal financial aid to support their education, the newly revised FAFSA reduces the number of questions to 36 questions from 108.

It also uses a new formula for determining the “Expected Family Contribution” (EFC) — which has been renamed the “Student Aid Index” (SAI). The new FAFSA still requests information on the number of children in your household, but the SAI will no longer provide a discount for multiple children in college at the same time.

“On a relative basis, this affects all applicants,” said Pearson. “But people with twins or multiples who are in college together all four years are the ones who are going to face the biggest increase as a result of this change.”

The disappearing discount math

Under the prior FAFSA formula, a family’s EFC was divided equally by the number of children they had in college simultaneously.

For example, if your household income was $200,000 and your EFC was determined to be $42,000 per year, you would subtract your EFC from the cost of attendance to determine your family’s financial need. (The actual amount families pay for tuition can be substantially higher or lower than their EFC, depending on the college and their FAFSA inputs.)

So, hypothetically, if the cost of attending a college is $50,000, your first child would have qualified for $8,000 in possible aid.

When your second child started college the following year, your EFC would have been divided by both of your kids — lowering it by 50 percent to $21,000 each. So, using the hypothetical school cost example above, each child would have qualified for $29,000 in possible aid.

And if your third child started college a year later, your EFC that year would have been 33 percent per child, etc. And each child would have qualify for more possible financial aid.

That was a big financial win for families that qualified for need-based aid — especially those with twins or multiples who overlapped in college for all four years. It also created an incentive for families with children who are close in age to be strategic.

For example, to maximize their EFC discount, some families previously opted to send their oldest child to community college for the first year or two to keep their child on course academically, and then have them transfer to a four-year college or university only after their younger sibling started college.

“We also used to suggest to families with kids who were two years apart in school that the oldest child consider a gap year, so they could at least divide their EFC for those three years when their kids would be in college at the same time,” said Brock Jolly, a financial professional with The College Funding Coach in Vienna, Virginia. “These strategies will no longer work.”

Always fill out the FAFSA

Jolly notes that the changing FAFSA formula is unlikely to affect higher-income households that do not qualify for need-based financial aid. And the lowest-income households will continue to qualify for grants, work-study programs, and low-interest loans. It’s middle-income families with college-bound children close in age that will feel the sting of the new FAFSA formula the most.

Regardless of where your family falls on the income spectrum, however, Jolly encourages all students to continue filling out the FAFSA. You never know what you may qualify for until you try. And the FAFSA is still a good chance to secure an academic (merit-based) scholarship distributed by individual schools.

“You’ve got to understand the rules and how to play the game,” said Jolly. “Start by drawing a line in the sand in terms of how much you are willing to pay for college and then determine your eligibility for need-based aid. Regardless of circumstances, I always encourage families to complete the FAFSA. It’s the gateway to merit-based aid.”

Another reason to fill out the FAFSA, especially for high-income families? A competitive edge in the applicant pool.

While many colleges are moving toward a “need-blind” application process, in which they do not consider the applicant’s ability to pay full tuition, some still do consider the family’s potential need for financial assistance when determining which students to accept.

“There are colleges out there that will make admissions decisions based upon your ability to pay full fare,” said Jolly. “So, if school X looks at your FAFSA and sees that your family’s SAI is six figures or more, they may be more likely to accept that student over another candidate who would need financial aid. A full-pay family may have a small leg up.” The college admissions service PrepScholar offers a list of need-blind schools.

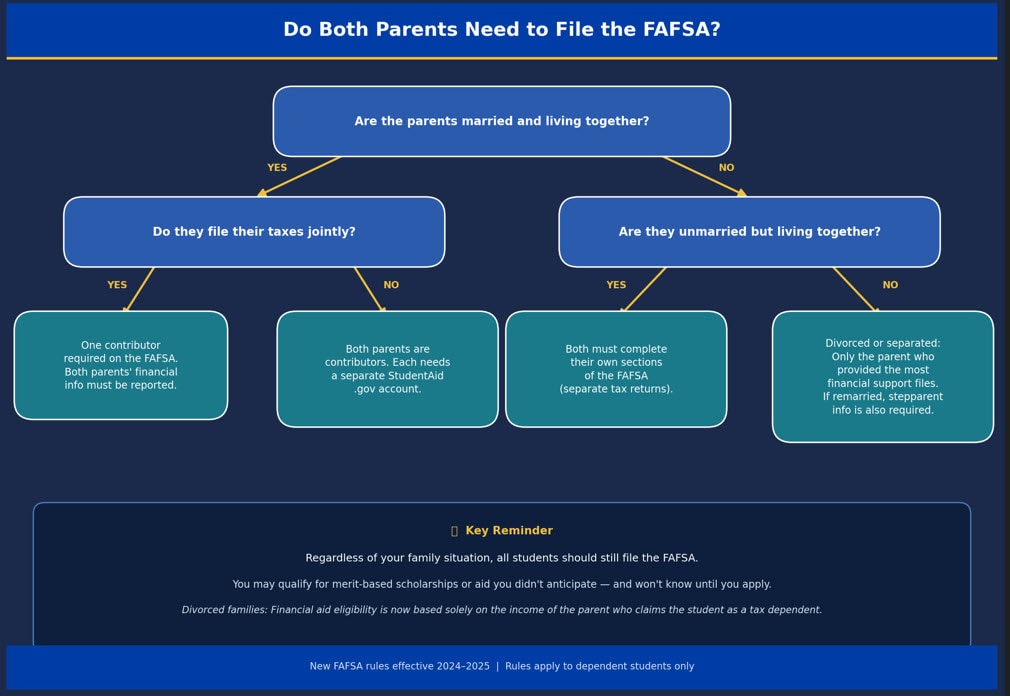

Should both parents fill out the FAFSA?

If your child is considered a dependent student on the FAFSA, you will need to provide parental information as well about your household finances. Whether both parents need to fill out the FAFSA depends on your family's marital and tax-filing status.

- If you are married (and not separated) and file taxes jointly, only one of you will be required to be a contributor on the FAFSA form. But information for both parents must be reported.

- If you are married (and not separated) but file a separate tax return, you are both considered contributors. Each parent must create a separate StudentAid.gov account to log in and provide their own tax and financial information

- If you are unmarried but live together both of you must fill out your respective sections of the FAFSA, as they will have separate tax returns.

- If you are divorced or separated only the parent who provided the most financial support to you in the last 12 months (or the parent with the greater income/assets) needs to fill out the form. If that parent has remarried, your stepparent's information must also be included.

Other changes to the FAFSA

The other big changes to the FAFSA include:

- The income protection allowance (IPA) increased for parents by 20 percent and for dependent students by 35 percent. The IPA shelters a portion of the applicant’s income from the financial aid formula, which reduces their expected contribution. According to college website Savingforcollege, this change increased the parent IPA by $4,000 to $8,000 for most families. It also increases the IPA for dependent students by $2,400, for independent students by between $3,800 to $6,100, and for single-parent students by about $6,500. As a result, the SAI will be reduced by about $5,000 for dependent students and up to $3,000 for independent students.

- Income earned from work can be set to zero if the student or parent applied for unemployment benefits within the last 90 days.

- For divorced parents, financial aid eligibility is now determined exclusively by the income of the parent who claims the student as a dependent on their taxes. Under the prior FAFSA, financial aid was determined by the income of the custodial parent, the one with whom the child spent more than 50 percent of their time. If the noncustodial parent had a higher income, he or she could still claim the child as a dependent on their taxes. That option no longer exists under the new FAFSA formula.

- Untaxed income from family members is no longer reported on the FAFSA. A generous grandparent who put money into a 529 college savings plan for their grandchild, or paid money directly to a university on behalf of their grandchild, previously ran the risk of negatively affecting their grandchild’s eligibility for future financial aid. They can now give without fear as untaxed income from family members will not be factored into the SAI.

- Students are now able to easily determine their eligibility for a Pell Grant based on their income and family size before they even apply for financial aid.

- Students with drug-related convictions are now eligible for federal financial aid.

- Male applicants are no longer required to register for the Selective Service before age 26.

How you can plan

Families that are negatively affected by the new FAFSA formula should start planning now, said Jolly.

There are still plenty of ways to cut the cost of college down to size — and some may reduce your tuition costs by half or more. (Learn more: 6 ways to cut college costs in half)

Cost-saving strategies include attending one or two years at a local community college, where tuition and fees are typically a fraction of what you’d pay at a four-year college, and then transferring to a four-year school to finish your degree.

Students can also level down to a less-prestigious school, or a so-called “safety school,” which is more likely to provide a bigger merit scholarship to top applicants. Some colleges also participate in a reciprocity program, offering in-state tuition to nonresident students within their regional network.

Students may also potentially benefit by applying to private colleges that use the CSS Profile to determine financial aid. The CSS Profile, which also provides a discount to families with multiple enrolled children, requires greater detail on the family’s financial assets and income.

“Everything I have seen says that CSS Profile schools are not changing their formula,” said Jolly, who notes that the discount as it currently stands is slightly less generous than the FAFSA discount today for multiple enrolled students. But when the FAFSA discount disappears, it will be the only port in the storm for families seeking a financial break when their children overlap in college.

For families with two children enrolled in college, the CSS Profile reduces their expected household contribution to 60 percent per student. Three children enrolled simultaneously would each pay 45 percent of the family’s expected contribution, and four children enrolled at the same time would pay 35 percent.

The sticker price for private colleges may look daunting, but keep in mind that many private schools have bigger endowment funds than public schools and are therefore able to provide more generous scholarships.

With big changes coming to the federal application for financial aid (FAFSA), families with children who are close in age should begin planning now for potentially higher costs down the road.

A financial professional who specializes in college planning can help you determine the best way to navigate the system, keep tuition costs under control, and help your child minimize the debt they incur.

____________________________________

Frequently Asked Questions about the FAFSA changes

Q: Does having multiple children in college increase my financial aid?

A: Not anymore. Under the new FAFSA rules, the Student Aid Index (SAI) no longer divides your expected contribution by the number of children you have enrolled in college at the same time. This means having multiple kids in college will not automatically increase your federal financial aid eligibility.

Q: What is the Student Aid Index (SAI)?

A: The Student Aid Index (SAI) is the new formula used to determine your financial aid eligibility, replacing the Expected Family Contribution (EFC). It evaluates your family's financial strength to calculate how much federal student aid you may receive.

Q: Can I still get a sibling discount for college tuition?

A: While the federal FAFSA formula no longer offers a sibling discount, some private colleges that use the CSS Profile may still consider the number of enrolled siblings when awarding their own institutional aid. It's always best to ask the school's financial aid office directly.

Discover more from MassMutual…

On the hunt for the most generous colleges

College shopping: Big fish or big pond?

Need financial advice? Contact us

This article was originally published in July 2021. It has been updated.