| ||||||||||||

You may have learned about Maslow’s hierarchy of needs in your high school or college psychology class. Well, it can work for your financial needs too.

Maslow’s idea is that you have to meet your most basic level of human needs before you can meet your higher-level needs. The hierarchy is often depicted as a pyramid, with physiological needs such as food and shelter forming the base, followed by physical safety, social needs such as friendships and family relationships, esteem needs like respect from coworkers and a sense of achievement, and self-actualization. You can’t worry about your safety unless you’ve got food in your belly, and whether you’re fulfilling your ultimate purpose in life might feel irrelevant if you’re lonely.

By applying a similar approach to your finances, you can prioritize what’s most important among what might seem like an overwhelming number of responsibilities, from paying off debt to saving for retirement. What should a hierarchy of needs for general personal financial security — a financial pyramid — look like?

There’s no official set of guidelines, but here’s a suggestion:

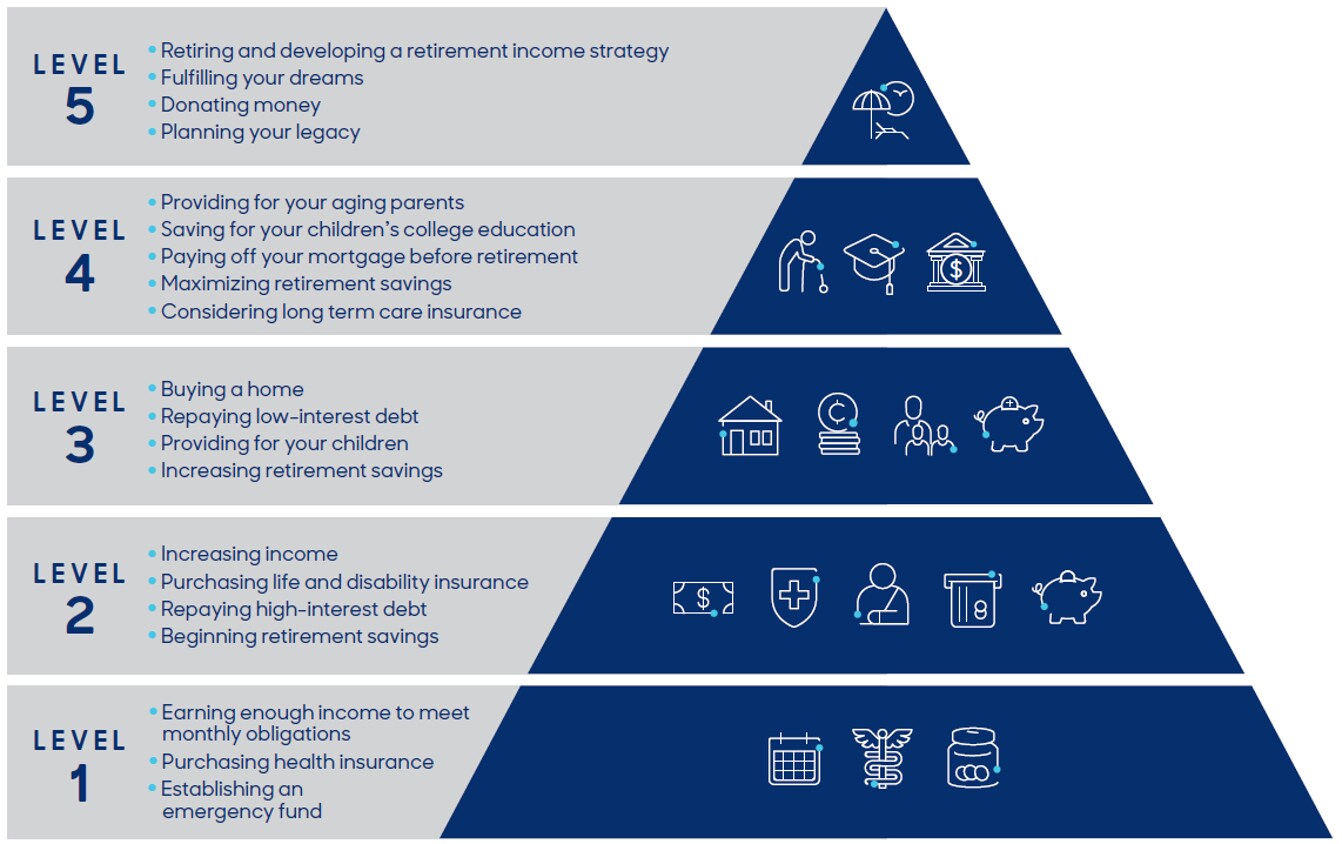

- Level 1 (base): Earning enough income to meet monthly obligations, purchasing health insurance, establishing an emergency fund.

- Level 2: Increasing income, purchasing life and disability insurance, repaying high-interest debt, beginning retirement savings.

- Level 3: Buying a home, repaying low-interest debt, providing for your children, increasing retirement savings.

- Level 4: Providing for your aging parents, saving for your children’s college education, paying off your mortgage before retirement, maximizing retirement savings, considering long term care insurance.

- Level 5 (peak): Retiring and developing a retirement income strategy, fulfilling your dreams, donating money, planning your legacy.

Putting it all together, it would be:

The concept of a financial pyramid not only can help you prioritize financial goals, it also can make sure you aren’t exposed to unnecessary risks. For example, if you haven’t completed the insurance steps at level 2 to make sure that you and anyone who relies on your income are protected if you become disabled or pass away unexpectedly, it’s not a good idea to buy a house (level 3). Taking on a mortgage becomes extremely risky if you don’t have a way to pay it if something bad happens. And lenders won’t even give you a mortgage if you haven’t completed the tasks at level 1 of the financial pyramid: having enough income to meet your monthly obligations and having an emergency fund.

While some steps shouldn’t be pursued out of order, there is some flexibility in the financial pyramid. Building an emergency fund at level 1 might not be an option if money is tight; that step might have to wait until level 2. Many people will want to donate money long before they reach level 5, even if they haven’t fully met their own financial needs, especially if they belong to a religion that encourages tithing. None of us can wait until we retire to use some of our savings to fulfill our dreams; we need small doses of satisfaction throughout our lives to enjoy ourselves and to sustain the motivation to keep working, saving, and investing.

Still, this version of the pyramid, with some tweaks to reflect individual circumstances, may work for most people.

Looking at the steps at each level in more detail….

Level 1 — What are the bare essentials you must cover no matter what? For most people, they’re food, shelter, electricity and natural gas, and transportation to work. Health insurance falls into this category, too. If you can’t afford to buy it, you may qualify for Affordable Care Act subsidies. If you can afford to buy health insurance, then you should make it a priority because it will not only protect your health and your ability to work, it will also protect your income and assets against the possibility of exorbitant medical bills. Creating an emergency fund gives you a cushion so you don’t have to go into debt to meet an unexpected expense.

Level 2 — Once you’ve handled your basic financial needs, you can move up to the pyramid’s second level. You’ll need to increase your income to start meeting these needs. A term life insurance policy is an easy and affordable purchase, especially if you’re a young, healthy nonsmoker who isn’t overweight.

Disability income insurance is more complicated and in some cases pricier, but it’s an essential component of your long-term financial well-being. By providing a monthly benefit if you become too sick or hurt to work, disability insurance helps you avoid depleting assets that are earmarked for other financial goals, such as retirement. (Calculator: How would a disability affect my finances?)

Repaying high-interest debt is also important at this stage, because making expensive, ongoing interest payments detracts from your ability to do better things with that money, like saving for retirement. (Learn more: Handling debt)

But even if you haven’t paid off all your debt yet, it’s a good idea to start saving a small amount for retirement just to get in the habit. In particular, if your employer offers a 401(k) match (say, for example, they match 5 percent of your pretax salary), you should contribute enough to get the full match. For example, on a $50,000 annual income, that’s $2,500 per year, $208 per month or $96 per paycheck, and it means you’ll get another $2,500 in free money.

Level 3 — With your basic insurance needs met, your high-interest debt paid off, and your retirement savings underway, you likely can start focusing on saving for a down payment to buy a home. In today’s market, you’ll need as little as 3 percent of the purchase price, though you’ll pay less monthly and overall if you can save closer to 10 percent or 20 percent. Having paid off your credit cards will make it easier to qualify for a loan.

Many people buy a home in anticipation of starting a family. If that’s part of your plan, then providing for your children becomes a financial priority at this stage of the pyramid, which means starting college savings plans and looking at ways to protect them should something happen to you. (Calculator: How much life insurance do I need?)

And if you have lower-interest debt — say, a car loan at 6 percent interest — you might want to put extra money toward paying that down, while also increasing your retirement contributions. Ideally, you’ll put 15 percent of your income toward retirement.

It’s at this point, when financial priorities begin to build up, that some people opt to talk with a financial professional to help sort through options. (Learn more: When do you need a financial professional?)

Level 4 — At this stage, you might be settled into family life, with a home you’ve lived in for years and a career that’s well established. Ideally, you’ve racked up a few raises and promotions over the years and are comfortably paying your monthly bills and saving for retirement. If so, then you may want to focus on putting your extra savings toward your children’s college fund. You might also have aging parents who need financial assistance — or who need your time, requiring you to work a bit less. (Learn more: Coping in the sandwich generation)

With your own retirement becoming more of a reality than an abstract concept, you may want to focus on maximizing your retirement savings, which includes making catch-up contributions if you’re eligible. Paying off the mortgage so you don’t have a monthly housing payment during retirement should be another priority. In some instances that may mean staying away from expensive home remodeling projects that would require you to take out a home equity loan. It also may mean asking your kids to choose a college you can afford without going into debt. (Calculator: What will my retirement income be?)

At this level you may also want to consider purchasing long term care insurance, which will pay for professional help with activities of daily living such as bathing and dressing if you become unable to care for yourself. The younger you are, the more likely you are to be insurable and the lower your premiums will be.

Level 5 — The peak of the pyramid is where you can, with hope, relax and enjoy your earlier efforts at building financial security. You may be able to retire and start living off the income from your investments. You might have more money available to donate, with your children grown up and your mortgage paid off.

You can fulfill those wish list items that you had neither money nor time for during your working years, like touring Europe or buying a vacation home in the mountains. It’s also time to update your estate plan. Your wishes might have changed since you first drafted a will (maybe when you had your first child) and your financial situation might have improved significantly, necessitating a different strategy for distributing your assets after your death.

Learn more from MassMutual...

Baseball and the longevity threat

Lending money to family...good idea?Lying on insurance? There are consequences...

This article was originally published in November 2016. It has been updated.

__________________________________________