| ||||||||||||

You want to be able to transfer your assets to the next generation with as little red tape as possible — and that often means doing what you can to avoid probate. A trust is one way to do this, but it’s not the only way.

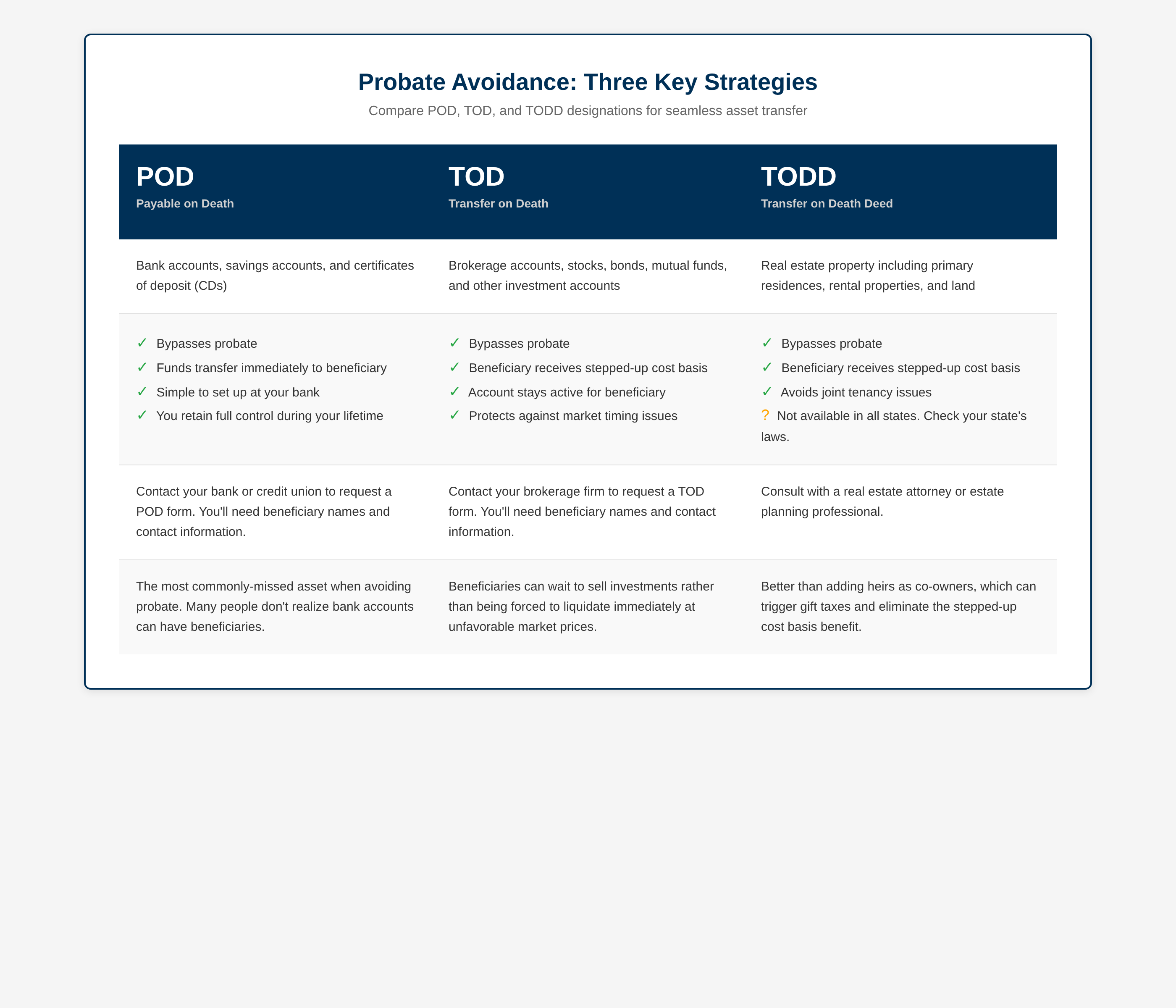

Outside of a trust, avoiding probate comes down to three things:

- Understanding the tax implications of passing on property.

- Filling out the right paperwork to make your assets transfer directly to your inheritors.

- Keeping your beneficiary information up to date.

While these options are available, whether they make sense for you will depend on your specific situation. Many people opt to consult a financial professional before making choices.

Connect with a MassMutual financial professional

What is probate?

Probate is the legal process that oversees the settlement and distribution of assets in an estate. This process, which guides the legal acceptance of a will (if there is one) and appointment of an executor, essentially wraps up a person’s legal and financial affairs after his or her death. Depending on circumstances, it can be a long and costly exercise. (Related: Why people fear probate)

“Probate is typically caused by four triggers: accounts, titles, registrations, and deeds,” according to Skip Johnson of Great Waters Financial. “Depending on the state you’re in, having a trust may help with estate tax exemption, but if avoiding probate is the main goal there are other ways to do it.”

Most of these ways come down to filling out forms that transfer assets directly to your beneficiaries upon your death. Different types of accounts require different paperwork, and while some are given to you, others you have to ask for.

Qualified investments like 401(k) and other retirement savings plans often ask you to list beneficiaries when you sign up. It’s generally a good idea to name someone — and remember that you can change your beneficiary designation over time if you need to.

Johnson noted that because these assets are contracts that pass outside of a will, it’s important to check your beneficiary designations periodically to make sure they’re still in line with your wishes.

This is also true for life insurance policies which, according to Johnson, “should have a person, and not the estate of a person, designated as the beneficiary” in order to avoid probate. Naming your estate the beneficiary of a life insurance policy brings the death benefit proceeds back into the probate process.

But what about all the assets outside a retirement plan balance or life insurance policy?

Things like real estate, brokerage accounts, and even regular checking and savings accounts are part of your estate, too. If directions for transfer are included solely in your will, those assets will be lumped with your estate and unavailable to your beneficiaries until the probate process is complete. Probate can take months or even years depending on your state’s laws and the complexity of your estate.

Real estate and Transfer On Death Deeds

Real estate is one of the most common things people want to pass to the next generation. To keep the transition of property to your heirs seamless and outside of probate, you may want to consider creating a TODD, or Transfer on Death Deed.

You may have thought about changing the property deed now to list your inheritors as co-owners, but this might not be the simple solution it appears.

Rights of survivorship generally apply to spouses, whereby one spouse takes full possession of the home outside of probate upon the other spouse’s death. However, this joint tenancy with right of survivorship has four requirements to apply, one of which is that the co-owners must have acquired the property at the same time — which typically isn’t the case when passing a home on to children.

“Probate is a far lesser concern between married couples,” said Johnson. “We’re talking about the second death in a married couple, when the second joint owner passes away and the estate needs to change hands entirely.”

The biggest consideration when arranging to transfer assets to the next generation may be the tax implications, which can hit both now and later.

To start, adding someone to an existing deed makes them an owner. In the eyes of the IRS, making someone an owner of your property “without expecting to receive something of at least equal value in return” constitutes a gift and may be subject to gift tax.

And while it’s true that having joint owners on the house is likely to reduce or eliminate exposure to probate, when those joint owners are multigenerational it creates potential for tax issues down the road.

This is because of how the cost basis on property works. If your inheritors are listed as owners on the current deed, their names will be associated with the price you paid for the property. So, they won’t just own the property — they’ll “own” all of the gains in its value since you bought it, too. (Related: Real estate and wealth transfer)

For example, let’s say you bought your house 30 years ago for $80,000, and on today’s market it’s worth $300,000. You put your daughter’s name on the deed to make her a co-owner, because you wanted the property’s transition to her to be seamless. Not only have you made a gift to your daughter, but now her name is on a piece of paper that lists the house at the price you bought it for — which means it appears as the price she bought it for, too.

The amount for which a property was purchased is known as the cost basis. When a property is sold for more than its last purchase price, the profit is a capital gain, which is taxable. The IRS allows for an exclusion of $250,000 ($500,000 for a married couple filing jointly) on the sale of the property if the following conditions are met:

- You owned the home and used it as your main home during at least 2 of the last 5 years before the date of sale.

- You did not acquire the home through a like-kind exchange (also known as a 1031 exchange), during the past 5 years.

- You did not claim any exclusion for the sale of a home that occurred during a 2-year period ending on the date of the sale of the home, the gain from which you now want to exclude.

The first condition is probably the most important in this example.

If your hypothetical daughter sells the house at its current market value of $300,000 and has not lived in the home as her main residence for at least two years prior to selling it, she’s looking at having to pay taxes on the full capital gains amount, which is the current sale price minus the seller’s cost basis.

In this case, because she’s listed on paperwork that shows an $80,000 cost basis, that difference amounts to $220,000 that she’ll have to pay taxes on as a result of the sale.

This is where the Transfer on Death Deed can be helpful.

“Filling out a TODD allows beneficiaries to get a stepped-up cost basis on the house,” said Johnson, “which means that when the asset is transferred to them, its past is basically erased. They receive the property at its current market value, which means that they pay taxes only on future gains when and if they decide to sell.”

Be aware, though, that not all states allow for TODDs. And the availability depends on where the property is located. So be sure to check state and local requirements.

Stocks, investments, and bank accounts

If you own stocks, you’ll probably want to pass those on, too, and similar rules apply.

One option for a brokerage account is to fill out a POD or Payable on Death form, which makes the current market value of the asset transfer directly to the named beneficiary upon your death. But if you want the whole active account to pass intact, rather than pay out, you may want to consider a TOD instead.

“A TOD, or Transfer on Death,” according to Johnson, “allows beneficiaries to take ownership of an active account. This can be especially advantageous if a stock is experiencing a temporary blip, because they can wait to sell it rather than taking payout at a low market value.”

The TOD serves the same purpose as a TODD, giving the inheritor(s) a stepped-up cost basis on the property to avoid paying taxes on your previous gains should they decide to sell the investments.

This kind of property transfer isn’t just reserved for high-profile properties like stocks and real estate.

“The most commonly-missed asset we see is bank accounts,” Johnson said. “People often don’t know you can set a beneficiary for a regular bank account by making the account POD, or Payable on Death, which allows the contents of the bank account to skip probate and go immediately to the listed beneficiary.”

The important thing when it comes to non-qualified properties is that you have to ask for the POD, TOD, and TODD paperwork — banks, brokerage firms, and real estate agents generally won’t ask who your beneficiaries are when you open an account or purchase a property.

And in order to keep things moving as seamlessly as possible when trying to avoid probate, remember that it’s best if your beneficiaries match across paperwork. Feuds can arise if your will states one beneficiary but a POD form states another, so make sure you take the time to maintain consistency across your estate documents. (Related: Splitting heirs? Keeping your mourning family from fighting)

“Having the right beneficiary information across documents is important,” said Keven Milgram, director of financial planning at Bienenfeld, Lasek & Starr, LLC , “because the last thing you want your family to have to do while they’re dealing with a loss is guess what you wanted to have happen. Not knowing causes fights. Writing it down and keeping it up to date lets your family know exactly what you want and gives them the time and freedom to do what really matters.”

_______________

Frequently Asked Questions about avoiding probate

Q: Do I need a trust to avoid probate?

A: Not necessarily. You can use direct beneficiary designations like Payable on Death (POD) or Transfer on Death (TOD) for many of your financial accounts.

Q: What is a Transfer on Death Deed (TODD)?

A: A TODD allows you to transfer real estate directly to a beneficiary upon your death, bypassing the probate process. However, these deeds are not legally available in every state.

Q: Does having a will help me avoid probate?

A: No, a will actually provides instructions for the probate court. To keep assets out of probate, they must pass outside the will via trusts or direct beneficiary designations.

Discover more from MassMutual

Who is responsible for debt after death?

This article was originally published in April 2017. It has been updated.