| ||||||||||||

A 401(k) is a common type of workplace retirement savings plan that gives employees an opportunity to contribute a portion of their income with pretax dollars into their own retirement investment account.

Indeed, since its creation in 1978, the 401(k) plan has become the most popular type of retirement plan offered by employers. Over 710,000 plans are in existence with more than $7.4 trillion in assets.1 In addition, there are plans — such as 403(b), 457, and 401(a) plans — that offer similar features and benefits for workers in specific labor sectors.

What makes 401(k)s so popular?

- Tax benefits

- Investment flexibility

- Possible employer matching contributions

While a substantial number of workers already take advantage of 401(k) savings plans, efforts are consistently underway to encourage more participation, especially among those just entering the workforce.

“More and more 401(k) programs are becoming a primary way for people to save for their retirement,” said Thomas Charla, a personal finance expert for MassMutual. “But 401(k) plans also come with provisions and rules about when and how money can be distributed from them. So, it is important to understand how they work.”

Connect with a MassMutual financial professional

How do 401(k)s work?

401(k) contributions are automatically deducted from your paycheck and invested in the plan. That means contributions will come out of your paycheck each pay period (unless you choose to stop contributing). 401(k) plans offer a range of investment options, typically stock and bond based mutual funds, to select from. (Related: New 401(k) investment options?)

If you are under age 50, you can put up to $24,500 in your 401(k) in tax year 2026 (the tax returns you file in April 2027). If you are over age 50, you can put in an additional $8,000 each year — called a “catch-up contribution.” For tax year 2026, a new provision enables those age 60 to 63 to make a higher catch-up contributions of up to $11,250. (Related: Tax changes on high-earner 401(k) contributions)

In addition to being an easy and convenient way to save, 401(k)s can offer a number of other benefits that may make them an effective way for you to financially prepare for retirement.

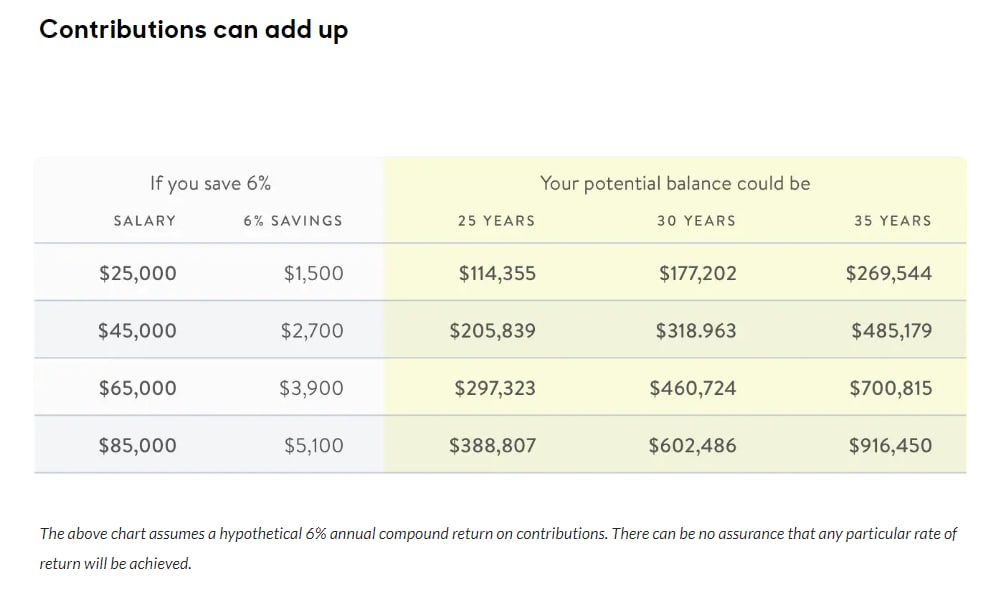

Company Match — Sometimes, companies make matching contributions to help your account grow more quickly. For example, a company may contribute 50 cents for every dollar you contribute up to 6 percent of your pay. In this case, if you contribute 6 percent of pay, then add the company match to your contribution, your contribution amount is effectively increased to 9 percent.

Compounding — Compounding is when the value of an investment increases because the earnings on your contributions are reinvested and, in turn, may produce even more earnings as time passes. Compounded growth occurs because the total growth of an investment along with the original contribution amount earns money — and keeps doing so over time.

Control — Most 401(k)s offer a variety of investment options. You have the opportunity to invest your money in options consistent with your risk tolerance and time horizon. (Related: What is your risk tolerance when it comes to investing?)

Tax Advantages —Contributions are deducted from your paycheck on a pre-tax basis, which means whatever you contribute reduces your current taxable income. When you eventually make withdrawals during retirement, you’ll have to pay taxes on original contributions and the account’s earnings at your ordinary income tax rate.

You can start withdrawing money from a 401(k) plan at 59½ years of age. But most people wait till sometime later. However, you must start withdrawing funds when you reach 73 years of age. (Learn more: Turning 73? Required minimum distributions explained)

Some employers may also allow you to make contributions to a Roth 401(k) as well. Unlike traditional retirement plan deferrals, contributions are made after-tax and withdrawals during retirement are income tax-free. And, unlike Roth IRAs, there are no income restrictions, so anyone can contribute. (Learn more: How a 401(k), Roth combo can help younger savers)

Conclusion

Put all together, a 401(k) plan can offer a good and sound start to build savings for retirement. It can also work in tandem with other savings and investment strategies to accommodate additional financial goals. A financial professional can help you understand how your 401(k) plan and other retirement investments fit in your broader financial plan.

Discover more from MassMutual …

Is maxing out your 401(k) enough for retirement?

5 retirement tax planning strategies

How to read your 401(k) statement — and why it matters

This article was originally published in September 2016. It has been updated.

__________________