| ||||||||||||

Beyond protection and the ability to build cash value, many whole life insurance policies typically offer a particular feature that many policyowners find attractive: the eligibility to receive dividends.

But this feature, while sounding simple, actually involves some complexity and comes with caveats. So, it’s important to understand the ins and outs of dividends in order to appreciate the overall benefit a whole life insurance policy may mean for you.

First and foremost, dividends aren’t guaranteed. The amount of the overall dividend and the individual dividend payouts are subject to change, depending on the operating experience of the insurance carrier in a given year. Generally, it’s a case of when the insurance company does well in a certain year, its policyowners benefit from that success and get a share of its divisible surplus.

Second, the policy has to be “participating,” that is, a type of life insurance or other financial product (like disability income insurance or annuities) that has been designated by the insurance company as eligible to receive dividends.

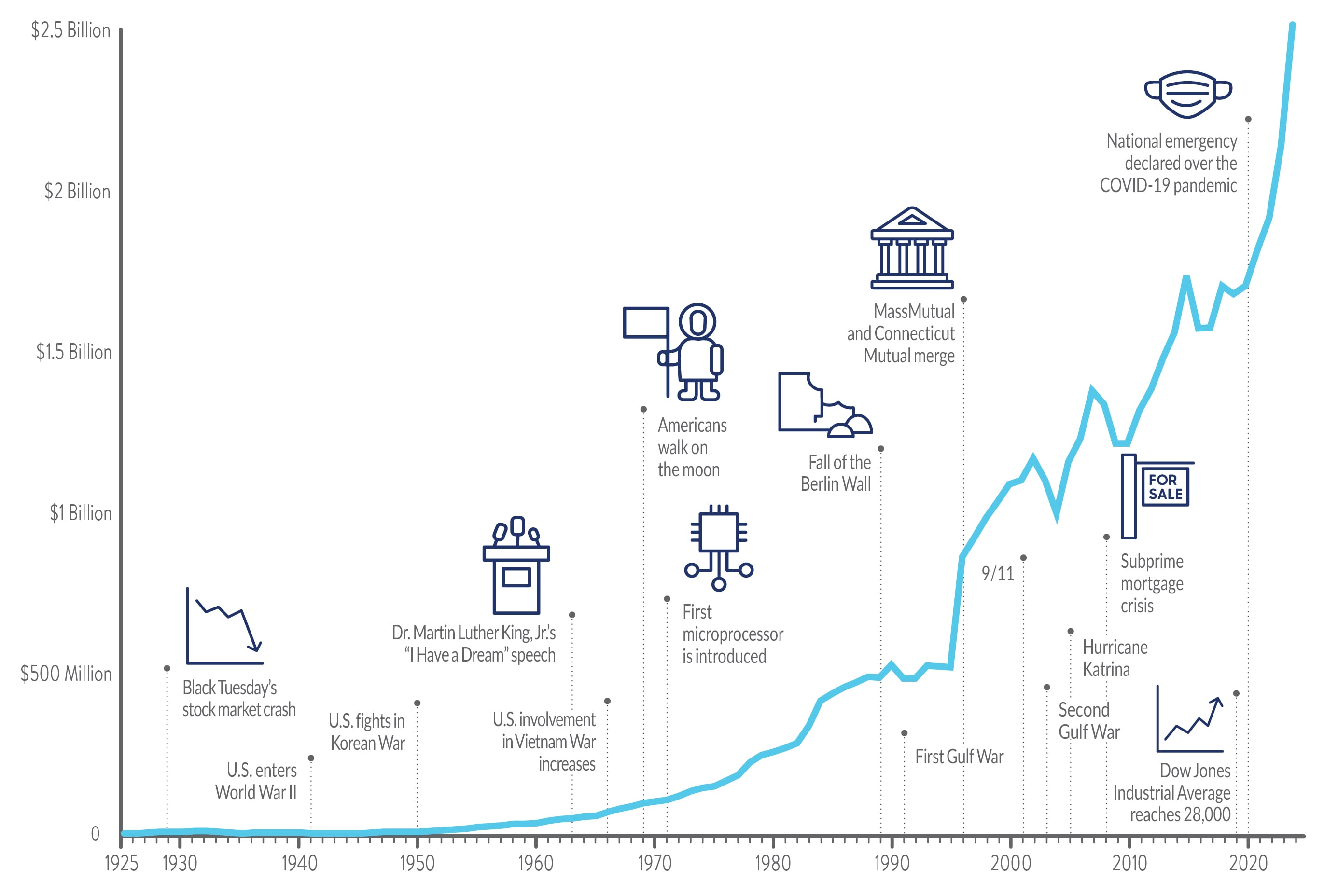

Although dividends are not guaranteed, most mutual insurance carriers strive to pay them consistently to eligible participating whole life policyowners. MassMutual, for instance, has paid dividends every year since 1869. And, as the company has grown, the overall amount of that annual dividend payout has grown as well, as noted in the following chart. (Learn about MassMutual's latest dividend announcement here)

Source: Massachusetts Mutual Life Insurance Company Statutory Annual Statement, Year-End – Summary of Operations – Dividends to Policyowners. These numbers reflect incurred dividends to policyowners. Incurred dividends equal amounts paid to eligible participating policyowners plus any increase in liabilities.

_______________________

So, how are dividends paid out by a mutual insurance company determined each year?

In general, insurance companies take in money through premiums from policyowners. They are required by law to keep a certain amount of that money in reserve to cover their long-term commitments to policyowners. Insurance companies generally invest these reserves in very conservative assets like high-grade bonds and commercial mortgages.

Each year, an insurance carrier calculates the amount of its surplus to set aside to be distributed to eligible participating policyowners as dividends. This is called divisible surplus. This is the amount paid out after the carrier has set aside the funds required to meet all contractual obligations, particularly reserve requirements for its policies, as well as what it expects for operating expenses, contingencies, and general business purposes.

Generally, dividends depend primarily on three components:

- Mortality experience (death claims)

- Expenses

- Investment results

Each eligible participating policyowner receives that policyowner’s equitable share of the divisible surplus that results when the overall actual experience of these components is better than the experience that was originally assumed in setting premiums and guaranteed elements for that policy.

Dividends are declared and paid annually. However, because a company cannot guarantee that divisible surplus will be achieved each year, the payment of dividends cannot be guaranteed. It depends on the company’s performance in these three areas.

Mortality

The mortality component is based on the actual death claims experience compared with what the insurance company estimated when it issued policies and priced premiums.

Performance in this area reflects how well an insurance company calculates and selects risk in its underwriting operations. A company that is careful about who it agrees to issue life insurance for and how to price the premiums for the policy is likely to have a more positive mortality experience over time. So, at the policy level, the mortality component of the dividend in any year is based on the age, gender, and underwriting class of the insured (their health and habits, like smoking), as well as the net amount of life insurance (face amount less the cash value) in that year. (Related: How a personal health record can lower your costs)

Expenses

Additionally, an insurance company, like any other business entity, will incur expenses to operate, from administration costs to investment fees to salaries. As mentioned above, a company will price premiums with those costs in mind and set aside funds to cover them.

The expense component of the dividend reflects the difference between the actual expenses that were incurred in issuing and administering policies over time as compared with the expenses that were assumed in setting the premiums.

A spike in costs or a decline in efficiency, therefore, will also subtract from the overall surplus. That’s why those considering a whole life insurance policy may want to research an insurance carrier’s corporate performance over time, to see how well it has controlled costs over time.

Investment

The third major element in determining dividends is investment performance. It is based on actual investment results for an insurance carrier that are more favorable than what is required to support policy reserves and guaranteed cash values.

When determining the premiums and guaranteed elements of an eligible participating whole life policy, insurers use conservative assumptions (guaranteed interest rates and mortality rates) to ensure that the company collects enough money to pay all benefits in the future, even under adverse financial scenarios. Favorable investment results occur when the company’s actual investment returns exceed the guaranteed interest rates required to meet its contractual obligations to policyowners.

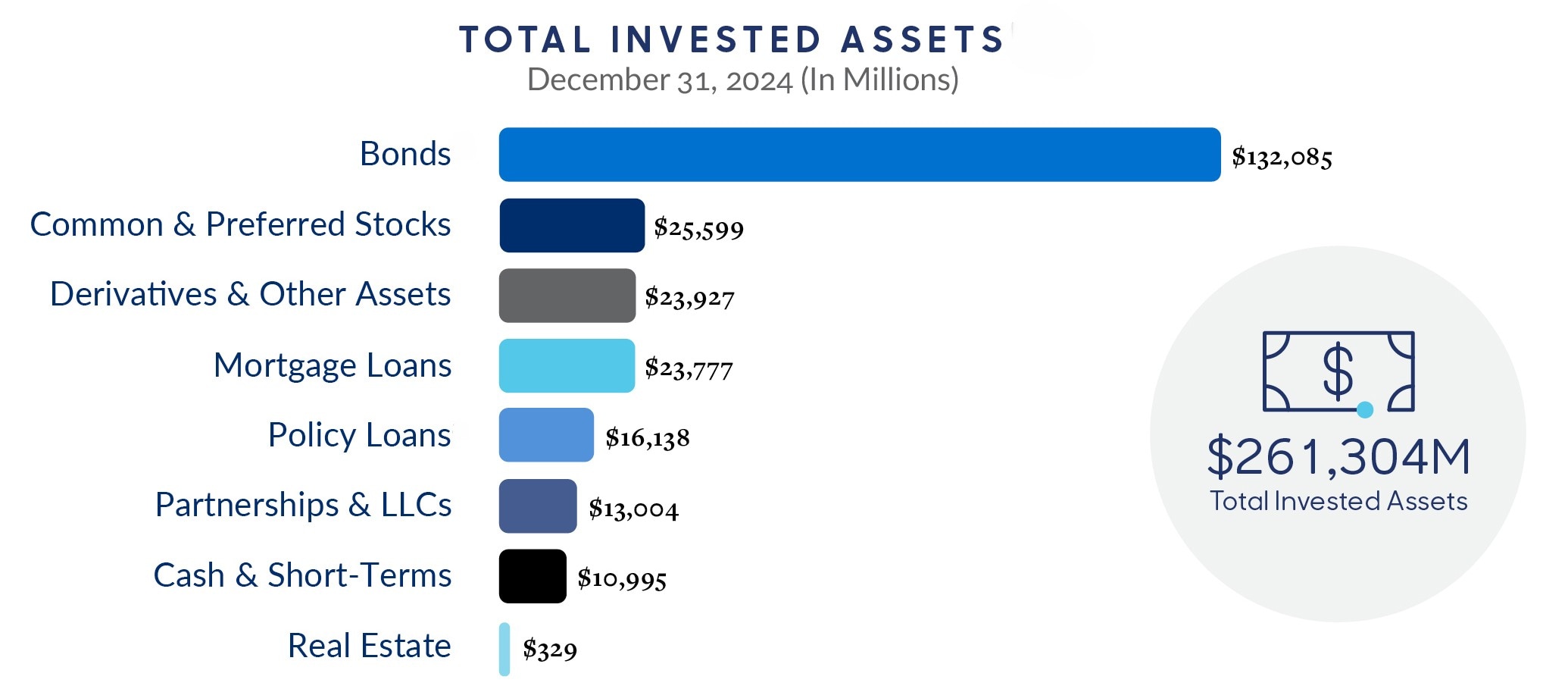

This rests in large part on the carrier’s financial portfolio, which is typically made up of bonds, stocks, and other types of market-based investments.

This is why it’s important for those shopping for whole life insurance to examine an insurance carrier’s holdings and investment philosophy, especially with regard to risk and stability. For instance, MassMutual’s investment goal is to generate competitive long-term results while maintaining the ability to weather downturns in financial markets.

The chart below is a snapshot of MassMutual’s holdings, which consist primarily of high-quality fixed-income securities, but also invest in equities, commercial mortgages, real estate, and other assets.

Invested Assets exclude $24,044 million of funds withheld given that 100 percent of the associated investment risk is reinsured. The funds withheld investment portfolio has counterparty protections in place, including investment guidelines that were established to meet MassMutual’s risk management objectives. Bonds exclude $21,471 million of funds withheld given that 100% of the associated investment risk is reinsured. The funds withheld investment portfolio has counterparty protections in place, including investment guidelines that were established to meet MassMutual’s risk management objectives. Policy loans are loans taken by policyowners against the cash surrender value of their policies and, as such, are secured by the cash surrender value of those policies.

You can find out more about MassMutual’s performance, financial holdings, and investment philosophy here.

Other business earnings

Beyond financial instruments, an insurance carrier can also achieve returns by investing in related business lines, third-party businesses, and other enterprises. Profits from those types of investments and operations can also add to a company’s overall surplus.

For instance, MassMutual offers a variety of insurance products beyond whole life insurance, such as annuities. Revenues from those areas help add to its surplus. And MassMutual has ownership stakes in global asset management companies and wealth management operations, which entitle it to a share of the profits those outfits produce.

These kinds of business lines and investments not only can directly add to a company’s surplus, but they can also diversify sources of income. That can soften the blow of a downturn in other types of investments or businesses.

The overall returns from the investment portfolio and other business earnings help support a company’s dividend interest rate (DIR)*, which is set by a company’s board of directors each year. The investment component of the dividend is the difference between the DIR and the policy’s guaranteed interest rate. So, hypothetically, if the guaranteed interest rate is 3.75 percent and the DIR is 6.60 percent, then the investment component of the dividend will be based on 2.85 percent (6.60 percent – 3.75 percent).

Comparing dividends and other returns

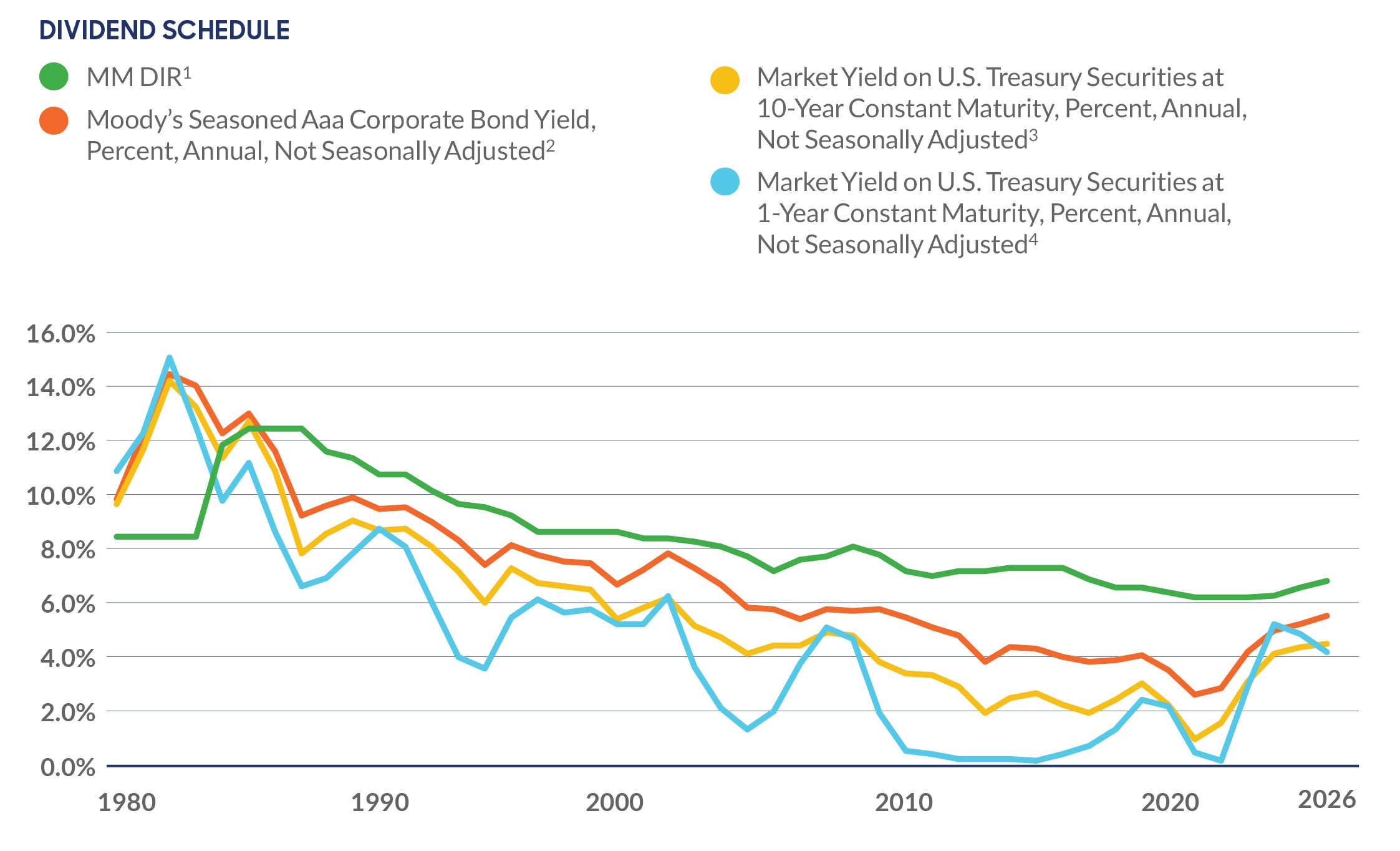

There is a temptation to compare life insurance dividends with returns on other types of financial instruments, like U.S. Treasury or corporate bonds. While such comparisons can be interesting and informative about relative performance, they aren’t entirely “apples to apples.”

For instance, the graph below shows MassMutual’s DIR in comparison with three common fixed-income measures over an extended period of time. Each measure reflects some calculations peculiar to that measure itself. For instance, mortality of policyowners isn’t a factor in determining the rate of U.S. Treasury bonds.

MassMutual’s DIR is determined using a portfolio average method that reflects the portfolio earnings on all assets that support our participating permanent life insurance and participating annuity blocks. Each portfolio is made up of investments purchased over a number of years, so changes in new money interest rates have a gradual impact on the DIR. The stabilizing effect of the portfolio average method over time is among the reasons MassMutual and many other insurers use this approach to determine their dividend interest rates.

1 Refers to the MM-block of business, which comprises policies issued prior to the merger of Massachusetts Mutual Life Insurance Company and the former Connecticut Mutual Life Insurance Company in 1996. Starting with the 2012 dividend schedule, there is a single Dividend Interest Rate for all blocks.

2 Moody’s yield on seasoned Aaa corporate bonds for all industries, quoted for the year preceding the Dividend Interest Rate shown; for 2026, the rate is the average monthly rate from January to September for the preceding year. Moody’s Aaa rates through December 6, 2001, are averages of Aaa utility and Aaa industrial bond rates. As of December 7, 2001, these rates are averages of Aaa industrial bonds only.

3 Market yield on U.S. Treasury securities at 10-year constant maturity, quoted for the year preceding the Dividend Interest Rate shown; for 2026, the rate is the average monthly rate from January to September for the preceding year.

4 Market yield on U.S. Treasury securities at 1-year constant maturity, quoted for the year preceding the Dividend Interest Rate shown; for 2026, the rate is the average monthly rate from January to September for the preceding year.

Who gets a dividend?

As mentioned at the outset, those who purchase eligible participating whole life insurance policies are eligible to receive a dividend. The size of each individual policyowner’s payout depends on how much their policy has contributed to the company’s divisible surplus. So long-standing policies with large death benefits will generally receive larger dividend payouts than smaller policies put in place more recently.

Policyowners typically have several different dividend options to choose from which include receiving dividends in cash, or use them to:

- Reduce the following year’s premium payment.

- Leave on deposit to accumulate with interest.

- Purchase paid-up additional whole life insurance.

Many policyowners go with the last option, which can increase the policy’s death benefit and cash value.

Conclusion

Dividends are an important part of the overall value that participating whole life insurance offers. But it’s important to know how dividends are determined and what may or may not affect their issuance and payment level.

Discover more from MassMutual …

The different types of permanent life insurance

Whole life insurance: Criticisms and rebuttals

What premium plan will work for you?

This article was first published in November 2019. It has been updated.

____________________________________

*The dividend and dividend interest rate (DIR) are determined annually, subject to change and are not guaranteed. Dividends for eligible participating life insurance policies primarily consist of investment, mortality and expense components. The DIR is used to determine the investment component of the dividend. It is not the rate of return on the policy and should not be the sole basis for comparing insurers or policy performance.

Participating whole life insurance policies issued by Massachusetts Mutual Life Insurance Company (MassMutual), 01111-0001.

.jpg)