| ||||||||||||

If you are considering life insurance, one of the choices you’ll likely encounter is universal life insurance (UL).

This kind of life insurance offers some financial flexibility in addition to protection. That may be advantageous for certain policyowners. But it is important to understand its features before deciding if it is right for you.

Part of the permanent life insurance family

To begin with, UL is a type of permanent life insurance. This is life insurance that offers a death benefit throughout a policyowner’s life, provided the premium payments are paid for a specified period. Permanent insurance is distinct from term insurance, which only provides coverage for a specified time period.

Further, some types of permanent life insurance offer:

- Tax-deferred growth of cash value.

- The ability to borrow against the policy’s cash value, including through loans.

Beyond these basics, permanent life insurance can offer a variety of features that may or may not be suitable for certain types of policyowners.

The UL premium difference

Whereas other kinds of life insurance policies require premiums to be paid on a stated schedule, universal life insurance allows for greater premium flexibility within the policy. A policyowner may adjust the amount they pay each year — or even month to month — in premiums, as long as there is enough cash value to cover the cost of insurance, expenses, and administrative charges of the policy. Those charges, along with credited interest rate assumptions help determine what minimum premium is required to keep the policy in force.

Why would flexible premium payments be desirable? Some people pay the maximum premium possible into a policy for the first years of coverage, with the potential to build up the policy’s cash value. That cash value can then be used for some future need, such as college tuition or to pay premiums if their income shrinks in retirement.

For example, someone who may want to guarantee an income source in the future can use higher early funding to create larger value inside the policy, then rely on that value later. (Related: What premium plan will work for you?)

“Universal life can be a good choice for someone fairly conservative looking to protect themselves through retirement,” said J. Todd Gentry, a financial professional with Synergy Wealth Solutions in Chesterfield, Missouri.

Connect with a MassMutual financial professional

Premium flexibility vs. whole life premiums

Compared with whole life insurance, universal life insurance is generally designed to be more flexible in how a policyowner funds a policy and how value can be built up over time.

Whole life typically follows a more standard premium schedule, with level premium payments that support a guaranteed death benefit and a more predictable cash value within the contract. Because the schedule is standard, the policyowner typically pays the same amount for years, and the policy’s cash value develops in a steadier pattern. (Related: Balancing protection and accumulation with whole life insurance)

Many universal life policies, by contrast, separate the premium from the monthly cost of insurance and administrative charges, allowing you to choose to pay more or less (within limits) as long as there is enough value to keep coverage in force.

That flexibility can be a benefit for some people, but it can also increase lapse risk: if funding falls below the minimum needed, the policy can lapse and coverage can end, even after years of premium payments. For those who want control over payments and timing, the flexible design of universal life can be appealing — but it generally requires closer monitoring than whole life to keep the policy on track.

If you choose this flexibility, the policy should be reviewed periodically so funding, credited interest rate changes, and charges do not undermine your long-term goals.

UL guarantees

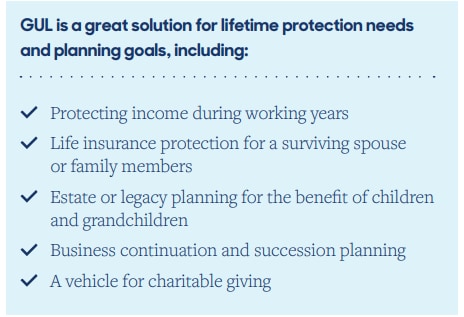

Some universal life policies offer what is called a “secondary” death benefit guarantee or no-lapse guarantee. You can pay a premium for a certain number of years and that will ensure your coverage will remain in place for life, even if the account value runs out. This is commonly described as Guaranteed Universal Life (GUL), where the focus is the death benefit guarantee rather than building cash value. These types of policies are often used to provide for final expenses, to ensure a financial legacy for children or grandchildren, or for the care of a special-needs loved one.

As the policy owner, at time of purchase you have the flexibility to determine how long you need coverage to last, how often and how much you pay in premiums, as well as the death benefit amount.

For example, someone could purchase a universal life insurance policy at age 50 and plan on paying a set premium for 15 years (to age 65) which would guarantee the policyowner a death benefit for life. If, for some reason, the policyowner paid less than the planned premium, the guaranteed period would be reduced.

To restore the guarantee, the policyowner may need to increase premium payments substantially. However, the policy owner would still have the option to pay more in subsequent years so the policy will provide up to a lifetime guarantee.

Another specific type of universal life insurance is indexed universal life insurance, which credits returns on the cash value based on market performance.

Also, like other types of life insurance, UL policies can come with a variety of added features, called riders, specific to the issuing carrier. These can include provisions to accelerate the payment of a portion of the death benefit to help meet health care needs in the event of a terminal illness or the ability to waive premiums in the event of a disability. But riders can increase charges and policy premiums. (Related: Understanding riders)

Why GUL pricing and availability can change

Pricing for GUL can change over time due to a number of factors, including regulatory changes and changes in the financial markets. Once purchased, an insurance company generally can’t change anything that would cause premiums required to fund the no-lapse guarantee to increase.

In practical terms, the rate assumptions used in a GUL illustration may be more conservative, and the minimum premium required to maintain a secondary guarantee may be higher than it was for older policies issued under prior reserving frameworks. (Related: What is an illustration?)

Cash value performance and lapse risk

Cash value growth and policy sustainability can depend on several moving parts inside universal life policies, including credited rate assumptions and policy charges. The credited interest rate affects how quickly value can build, while cost of insurance charges and expenses can rise as age increases.

If the interest rate is lower than expected — or if charges are higher — the cash value may not keep up, and the policy may require additional funding at a higher rate to avoid lapse.

In addition, if the credited interest rate stays low for years, the policy may need a higher funding rate to keep its reserve and value on track.

Loans and withdrawals will reduce death benefit, account value, and increase lapse risk, especially if loan interest accrues and the net value falls. Outstanding policy loan values can increase as loan interest accrues; managing loans carefully can help protect the death benefit and reduce lapse risk.

For many policyowners, the best approach is to review the policy regularly, watch in-force projections, and confirm whether minimum funding targets and the required rate are being met so the secondary guarantee (and any no-lapse guarantee test) remains intact.

Conclusion

The flexible premiums offered by UL policies may be attractive for certain individuals. But they aren’t for everyone. For instance, the premium flexibility can result in a policyowner having to pay more than the planned premium if they have not maintained a certain level of payments in earlier years, especially when credited rate assumptions change.

Potential policyowners should understand additional features offered by other types of life insurance such as variable universal life insurance and whole life insurance before making a decision. In many instances, a financial professional can help you choose among universal life policies and compare policy options to find the best fit.

Learn more from MassMutual …

9 questions to ask when shopping for life insurance

Is group life insurance enough?

This article was originally published August 2018. It has been updated.

__________________________

.jpg)