The dictionary defines “misconception” as a mistaken belief, a wrong idea or a false hope. In many ways, it also defines many people’s attitude towards long-term care (LTC).

One of the biggest misconceptions people have in preparing for retirement is that they will never need care for months or even years as they age. Another misconception is that paying for long term care is affordable.

Those beliefs are among several barriers that prevent many people from planning for the likelihood of needing long term care in retirement. While you may not expect to need LTC, the consequences could be severe if you face an unexpected LTC event. Working with a financial professional who understands both the need to protect against the potential consequences, as well as what options are available to prepare for them can be one of the best decisions you make in planning for retirement.

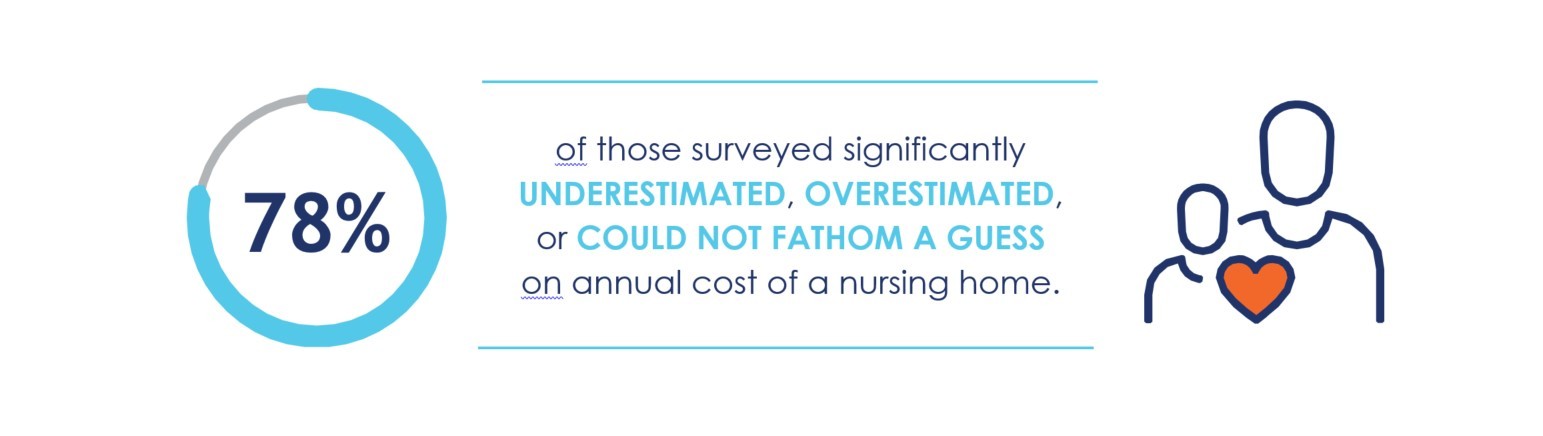

The impact and costs of long term care are often misunderstood. As an example, The MassMutual Long Term Care in America Study reveals that 78 percent of Americans ages of 45 to 70 significantly underestimate, overestimate, or cannot fathom a guess about the annual cost of a nursing home.1

Also, confidence in paying for LTC is a challenge for many Americans, especially when they are faced with the possibility that they may live longer than they expect. When asked to consider living 10 years beyond their self-reported life expectancy, 40 percent of study respondents become less confident about their ability to pay for care.

It’s worth noting that many Americans fail to accurately estimate their own life expectancy. According to the Society of Actuaries only half can estimate their own life expectancy within five years.2

The National Center for Health Statistics (NCHS) reported earlier this year that the average lifespan for Americans is now 78.7 years, (76.2 for men and 81.2 for women).3 But those figures are deceiving. The average lifespan figure takes into account the total population, including those who do not live to the traditional retirement age of 65. Those who reach that milestone typically live much longer lives. For instance, the average life expectancy for a 65-year-old is now 19.5 years or to nearly age 85, according to the NCHS.

Unfortunately, there is a correlation between living longer and a greater need for long term care. Adults ages 85 and older are much more likely to need LTC than those ages 65-74, especially support from a paid professional, according to HHS.4

Overall, 70 percent of Americans ages 65 and older eventually require some form of long-term care, with expenses potentially running into six figures, according to the U.S. Department of Health and Human Services (HHS).5

These facts underscore the need to consult a financial professional and develop a plan for potential extended care needs in the future. A financial professional can explain the options and alternatives available to help pay for care, and how various choices relate to a your specific financial, health and longevity needs.

With good fortune and careful planning, you and your family will be prepared for the possibility of needing long term care.

Discover more from MassMutual …

Is extended care part of your future?

Planning for diminished capacity as you age

Keeping caregiver costs contained

________________________

1 The MassMutual Long Term Care in America Study, conducted by Greenwald & Associates in 2019.

2 Society of Actuaries, “Longevity Perceptions and Drivers: How Americans View Life Expectancy,” https://www.soa.org/globalassets/assets/files/resources/research-report/2020/longevity-perceptions-drivers.pdf

3 Mortality in the United States, 2018, National Center for Health Statistics, Data Brief No. 355, January 2020, https://www.cdc.gov/nchs/products/databriefs/db355.htm

4 What is the Lifetime Risk of Needing and Receiving Long Term Services and Support?

U.S. Department of Health & Human Services, April 4, 2019, https://aspe.hhs.gov/basic-report/what-lifetime-risk-needing-and-receiving-long-term-services-and-supports

5 U.S. Department of Health and Human Services, Aging, Published Sept. 12, 2018.

.jpg)