| ||||||||||||

Life insurance offers many benefits. But some policy benefits can be hard to envision, as they are conceptual and ultimately materialize in the future. That’s where a life insurance policy “illustration” comes in.

An illustration is a document that lays out in visual form exactly what a particular kind of life insurance policy provides now and may provide in the future in terms of protection and other benefits. It is a powerful tool for analyzing and comparing the utility of different types of policies for particular individual situations.

“Life insurance is an unfamiliar subject for many buyers,” said Sam Eppy, managing partner at Levanti Wealth in Fort Lauderdale, Florida. “Additionally, many of those people are visual learners. Viewing an illustration remains one of the most valuable ways financial professionals can help educate their clients to guide them through the buying process.”

Why an illustration helps

To understand the usefulness of an illustration, it helps to understand the various benefits different types of life insurance offers.

First and foremost is protection. Life insurance provides a death benefit to help loved ones cope with the financial challenges of your passing. This can be especially important if that happens earlier than expected and your family must cope with the loss of the financial support you provide.

Basic term life insurance offers a death benefit for a specific period of time in exchange for a certain level of premiums. That’s a pretty straightforward arrangement and doesn’t require much to envision.

Permanent life insurance offers more. Permanent policies, such as a whole life insurance policy, build up cash value over time, which can be a sizable and helpful resource in the future. Additionally, whole life policies may be eligible for dividends from the insurance carrier. Dividends, while not guaranteed, when used to purchase paid-up additional insurance, can offer the opportunity for growth in cash value and death benefit. The additional insurance will also be eligible to receive dividends.

Since permanent life insurance policies cover an entire life (not just a specific period like term insurance), that growth can be substantial, but hard to envision.

And that’s where the illustration comes in.

What an illustration illustrates

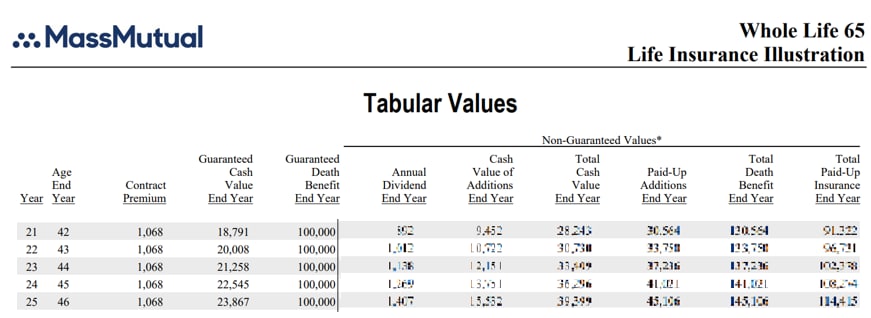

An illustration will lay out how the cash value death benefit are guaranteed to grow over the lifetime of the insured under the conditions set by the policy.

For instance, in a whole life insurance policy, the cash value grows at a rate guaranteed by the insurance company.

The illustration of such a policy will, in table form, show:

- The growth in that guaranteed cash value year by year.

- The guaranteed death benefit.

- The non-guaranteed, potential future values for the policy’s cash value and the death benefit based on the company’s current dividend schedule if it were to continue at the same level for all years in the future.

You can see an example of such estimates below in a hypothetical illustration for a 21-year-old female nonsmoker in excellent health living in Massachusetts. The policy used for the illustration is a whole life policy with a $100,000 death benefit and a premium schedule lasting until the 21-year-old turns 65.

- On the left are guaranteed cash values and the death benefit.

- On the right would be the non-guaranteed values based on potential dividend performance, based on the paid-up additions dividend option, in addition to the guaranteed results.1

Click on the image or here to see the full illustration.

An illustration will also provide information about:

- Different premium payment schedules (See What premium plan will work for you?)

- Premium payment limitations (See Mind your ‘MEC’: When life insurance morphs)

- Riders (See Understanding life insurance policy riders)

Given the breadth and complexity ― and the inclusion of non-guaranteed values ― in a life insurance illustration, it is important to review it with a financial professional, who generated it in the first place. They can explain the meaning of the various values based on the information provided and offer guidance on how it relates to your situation.

What does a financial professional need to generate an illustration? Generally, they need your age, smoking status, health status, and state of residence, and the amount of coverage you are looking to have.

From there, they can generate illustrations for a variety of policies. For example, whole life policies are available that can be paid up in as little as 8 annual premiums or as many premiums as it takes for the insured to reach age 100.

Illustrations can make the benefits of various types of life insurance policies apparent and comparable. You can contact a MassMutual financial professional to start investigating the possibilities.

Connect with a MassMutual financial professional

Discover more from MassMutual …

Is group life insurance enough?

How whole life insurance helps diversify your taxes

Whole life insurance: Criticisms and rebuttals

__________________

.jpg)